What Is Credit Analysis?

Credit analysis is a process of concluding available data (both quantitative and qualitative) regarding the creditworthiness of an entity and making recommendations regarding the perceived needs and risks. Credit Analysis is also concerned with identifying, evaluating, and mitigating risks associated with an entity failing to meet financial commitments.

As a Credit analyst, two days in life are never the same. Credit Analysis is about making decisions while keeping in mind the past, present, and future. The role offers a plethora of opportunities to learn and understand different types of businesses as one engages with a multitude of clients hailing from different sectors. The career is monetarily rewarding and helps an individual grow, along with providing good opportunities to build one’s career.

Key Takeaways

- Credit analysis is the process of concluding the available data (both quantitative and qualitative), evaluating the creditworthiness of a business, and offering recommendations for the perceived requirements and dangers.

- Character, Capacity, Capital, Collateral, and Conditions are the 5 Cs of credit analysis.

- The job offers many opportunities to learn about and understand different business models because one works with clients from various sectors.

- The occupation promotes personal growth, is financially rewarding, and offers good opportunities for career promotion.

Credit Analysis Explained

The concept of credit analysis involves the evaluation and assessment of credit worthiness of the borrower for the purpose of granting loans by financial institutions. Very often corporates or individuals apply for loan to meet their working capital requirements of to buy assets which require heavy investments. Taking loan is the best possible method to achieve the aim.

Every financial institution engaged in the process of granting loan are required to do a thorough check about the financial health of the corporate or credit rating of the individual which is the credit analysis process. If that meets certain predefined criteria, the lender will clear the process of issuing credit with the confidence that the borrower has the capacity to repay the loan within the time limit.

The commercial credit analysis is typically done by studying financial statements to assess the income and expenditure, the value of assets and future income potential of a company.

For individuals, the past credit history is studied, the value of the assets are calculated and there is also a need to understand the purpose or borrowing. The purpose of borrowing should be such that it should lead to enhancement of assets or reduction of liabilities. If it is taken for a startup business, the lender to assess the future potential of the business to become a success.

Thus, we see that the process determined the risk level of lending and make informed decisions regarding terms and conditions related to the loan. This help lenders reduce risk and borrowers get some favorable borrowing terms.

Video Explanation Of Credit Analysis

How To Do?

In layman’s terms, Credit analysis is more about identifying risks in situations where the bank observes a potential for lending. Both quantitative and qualitative assessment forms a part of the overall appraisal of the clients (company/individual). This generally helps to determine the entity’s debt-servicing capacity or its ability to repay.

Ever wondered why bankers ask so many questions and make you fill out so many forms when you apply for a loan? Don’t some of them feel intrusive and repetitive, and the whole process of submission of various documents seems cumbersome. You try to fathom what they do with all this data and what they are trying to ascertain! It is not only your deadly charm and attractive personality that makes you a good potential borrower; obviously, in case of commercial credit analysis there is more to that story. So here, we will try to get an idea about what a Credit Analyst is looking for.

From time immemorial, there has been an eternal conflict between entrepreneurs/people in business and bankers regarding the quantification of credit. The resentment on the part of the business owner arises when he believes that the banker might not be fully appreciating his business requirements/needs and might be underestimating the real scale of opportunity that is accessible to him, provided he gets a sufficient quantum of loan. However, the credit analyst might have reasons to justify the amount of risk he is ready to bear, including bad experiences with that particular sector or his assessment of the business requirements. Many times there are also internal norms or regulations which force the analyst to follow a more restrictive discourse.

The most important point to realize is that banks are in the business of selling money, and therefore risk regulation and restraint are very fundamental to the whole process. Therefore, the loan products available to prospective customers, the terms and conditions set for availing of the facility, and the steps taken by the bank to protect its assets against default all have a direct forbearance to the proper assessment of the credit facility.

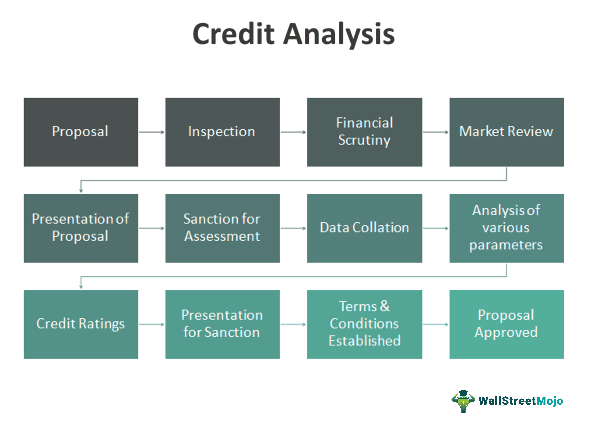

The 5 C’s of Credit Analysis

The below diagram shows the 5 C’s of Credit Analysis Process.

Character

- This is where the general impression of the protective borrower is analyzed. The lender forms a very subjective opinion about the trustworthiness of the entity to repay the loan. Discrete inquiries, background, experience level, market opinion, and various other sources can be a way to collect qualitative information. Then an opinion can be formed, whereby he can decide about the entity’s character.

Capacity

- Capacity refers to the ability of the borrower to service the loan from the profits generated by his investments. The lender will calculate exactly how the repayment is supposed to take place, cash flow from the business, the timing of repayment, probability of successful repayment of the loan, payment history, and such factors, are considered to arrive at the probable capacity of the entity to repay the loan. This is perhaps the most important of the five factors.

Capital

- Capital is the borrower’s skin in the business. This is seen as proof of the borrower’s commitment to the business. This indicates how much the borrower is at risk if the business fails. Lenders expect a decent contribution from the borrower’s assets and a personal financial guarantee to establish that they have committed their funds before asking for any funding. Good capital goes on to strengthen the trust between the lender and the borrower.

Collateral (or Guarantees)

- Collateral security is often used to offset distasteful factors that may have come to the forefront during the assessment process. Collateral is a form of security that the borrower provides to the lender to appropriate the loan in case it is not repaid from the returns established at the time of availing the facility. Guarantees, on the other hand, are documents promising the repayment of the loan from someone else (generally a family member or friend) if the borrower fails to repay the loan. Getting adequate collateral or guarantees may deem fit to partly or wholly cover the loan amount bears huge significance. This is a way to mitigate the default risk. Many times, Collateral security is also used to offset any distasteful factors that may have come to the forefront during the assessment process.

Conditions

- Conditions describe the purpose of the loan and the terms under which the facility is sanctioned. Purposes can be Working capital, purchase of additional equipment, inventory, or long term investment. The lender considers various factors, such as macroeconomic conditions, currency positions, and industry health, before putting forth the conditions for the facility.

Example

So, let’s have a look at what does a loan proposal looks like:

The exact nature of proposals may vary depending on subsequent clients, but the elements are generally the same.

So, let’s illustrate the whole exercise with the help of the example of Mr. Sanjay Sallaya, a liquor Barron and a hugely respected industrialist who also owns a few sports franchises and has bungalows in the most expensive locals. He now wants to start his airline and has therefore approached you for a loan to finance the same.

**To put things into perspective, let’s consider the example of Sanjay Sallaya, who is credited with being one of the biggest defaulters in recent history, along with being one of the biggest businessmen in the world. He owns multiple companies, some sports franchises, and a few bungalows in all major cities.

- Who is the client? Ex. Sanjay Sallaya, a reputed industrialist, owns the majority share in XYZ ltd. and others.

- They were starting a new airline division, which would cater to the high-end segment of society. Quantum of credit they need and when? Ex. Credit demand is $25 mil, needed over the next six months.

- The specific purpose the credit will be employed for? Ex. Acquiring new aircraft and capital for daily operations like fuel costs, staff payments, airport parking charges, etc.

- Ways and means to service the debt obligations (which include application and processing fees, interest, principal, and other statutory charges) Ex. Revenue is generated from flight operations, freight delivery, and freight delivery.

- What protection (collateral) can the client provide in the event of default? Ex. Multiple bungalows in prime locations are offered as collateral, along with the personal guarantee of Sanjay Sallaya, one of the most reputed businessmen in the world.

- What are the key areas of the business, and how are they operated and monitored? Ex. Detailed reports would be provided on all key metrics related to the business.

Answers to these questions help the credit analyst to understand the broad risks associated with the proposed loan and the type of credit analysis skills. These questions provide basic information about the client and help the analyst get deeper into the business and understand its intrinsic risks.

The loan is for a meager $1 million. So, as credit analysts, we have to assess whether or not to go forward with the proposal. To begin, we will obtain all the required documents to understand the business model, working plan, and other details of his new proposed business. Necessary inspections and enquires are undertaken to validate the integrity of his documents. A TEV, i.e., Techno-Economic Viability, can also be undertaken to get an opinion from the aviation industry experts about the plan’s viability.

When we are finally satisfied with the overall efficacy of the plan, we can discuss the securities that will collaterally cover our loan (partly/fully). If it meets all other aspects, such a proposal can be presented for sanction comfortably and generally enjoys good terms from the bank’s side as the risk associated with such personalities is always assessed to be less. Mr. Sanjay Sallaya, a well-established industrialist, holds a good reputation in the business world and, therefore, will make good recommendations.

Therefore, to conclude, Mr. Sanjay Sallaya will get a loan of $1 million approved and will go on to start his airline business. However, what the future holds can never be predicted when a loan is sanctioned.

also, check out the difference between Equity Research vs. Credit Research

Credit Analysis Fundamentals

Other than the above questions, the analyst also needs to obtain quantitative data specific to the client:

- Borrower’s history – A brief background of the company, its capital structure, its founders, stages of development, plans for growth, list of customers, suppliers, service providers, management structure, products, and all such information are exhaustively collected to form a fair and just opinion about the company.

- Market Data – The specific industry trends, size of the market, market share, assessment of competition, competitive advantages, marketing, public relations, and relevant future trends are studied to create a holistic expectation of future movements and needs.

- Financial Information – Financial statements (Best case/ expected case/ worst case), Tax returns, company valuations and appraisal of assets, current balance sheet, credit references, and all similar documents which can provide an insight into the financial health of the company are scrutinized in great detail.

- Schedules and exhibits – Certain key documents, such as agreements with vendors and customers, insurance policies, lease agreements, and pictures of the products or sites, should be appended to the loan proposal as proof of the specifics as judged by the indicators mentioned above.

**It must be understood that the credit analyst, once convinced, will act as the client’s advocate in presenting the application to the bank’s loan committee and also guiding it through the bank’s internal procedures. The details obtained are also used to finalize the loan documentation, terms, rates, and any special covenants which need to be stipulated, keeping in mind the business framework of the client as well the macroeconomic factors.

After collating all the information, now the analyst has to make the real “Judgement” regarding the different aspects of the proposal, which will be presented to the sanctioning committee:

- Loan – After understanding the client’s need, one of the many types of loans, can be tailored to suit the client’s needs. The amount of money, the maturity of the loan, and the expected use of proceeds can be fixed, depending upon the industry’s nature and the creditworthiness of the company.

- Company – The market share of the company, products and services offered, major suppliers, clients, and competitors, should be analyzed to ascertain its dependence on such factors.

- Credit History – The past is an important parameter to predict the future. Therefore, keeping in line with this conventional wisdom, the client’s past credit accounts should be analyzed to check for any irregularities or defaults. This also allows the analyst to judge the client we are dealing with by checking the number of times late payments were made or what penalties were imposed due to non-compliance with stipulated norms.

- Analysis of market – Analysis of the concerned market is of utmost importance as this helps us identify and evaluate the company’s dependency on external factors. Market structure, size, and demand of the concerned client’s product are important factors that analysts are concerned with.

Ratios

A company’s financials contain the exact picture of what the business is going through, and this quantitative assessment bears the utmost significance. Analysts consider various ratios and financial instruments to arrive at the true picture of the company.

- Liquidity ratios – These ratios deal with the ability of the company to repay its creditors, expenses, etc. These ratios are used to determine the company’s cash generation capacity. A profitable company does not imply that it will meet all its financial commitments.

- Solvability ratios – These ratios deal with the balance sheet items and are used to judge the future path that the company may follow.

- Solvency ratios – Solvency ratios are used to judge the risk involved in the business. These ratios take into the picture the increasing amount of debts, which may adversely affect the company’s long-term solvency of the company.

- Profitability ratios – Profitability ratios show the ability of a company to earn a satisfactory profit over time.

- Efficiency ratios – These ratios provide insight into the management’s ability to earn a return on the capital involved and the control they have on the expenses.

- Cash flow and projected cash flow analysis – A cash flow statement is one of the most important instruments available to a Credit Analyst, as this helps him to gauge the exact nature of revenue and profit flow. This helps him get a true picture of the movement of money in and out of business.

- Collateral analysis – Any security provided should be marketable, stable, and transferable. These factors are highly important as a failure on any of these fronts will lead to the complete failure of this obligation.

- SWOT analysis – SWOT Analysis is again a subjective analysis done to align expectations and current reality with market conditions.

If you wish to learn more about financial analysis, then click here for this amazing Financial Statement analysis guide.

Credit Rating

A credit rating is a quantitative method using statistical models to assess creditworthiness based on the borrower’s information. Most banking institutions have their rating mechanism. This is done to judge under which risk category the borrower falls. This also helps determine the term and conditions, and various models use multiple quantitative and qualitative fields to judge the borrower. Many banks also use external rating agencies such as Moody’s, Fitch, S&P, etc. to rate borrowers, which then forms an important basis for consideration of the loan.

Objectives

Let us look at some of the objectives of the concept.

- Determine the credit worthiness – The creditworthiness or the borrowing power of the corporate of individual is assessed using this process, which helps in determining whether they have the power to pay back the loan. Various types of credit analysis skills and indicators like the liquidity position, the asset values, the past credit history, the current liabilities, and also the objective of taking the loan is evaluated to arrive at the decision.

- Interest rate -The rate of interest at which the borrower will have to pay back the loan is determined using this credit analysis of banks and other financial institutions. If the credit rating is good, the borrower may get a loan at lower interest rates. In this case, the borrower is satisfied that they need to pay less interest, and the lender has the assurance that the borrower can repay the loan.

- Assessment of risk – It helps the borrower assess the risk level that they are accepting in return of giving loan to the borrower. This gives them an idea about any possibility of default or delay in payment of installments in the future.

- Monitoring – This also helps in monitoring of credit position of the borrower through continuous assessment of the financial situation so as to remain updated regardimg any change in the financial position of the borrower which may prove to be a threat to the lender.

- Decision – This process helps in the lender decide whether the loan can be extended to the borrower an dwhat kind of term and conditions should be put in the contract.

Thus, the above are some important objectives that the analysis of credit condition help to meet so that there is a continuous flow of money in the economy and it is channelized in the right direction without wastage.

Credit Analysis Vs Equity Analysis

Both the above are two different forms of financial analysis that are widely conducted among financial institutions for the purpose of evaluation of investment opportunities. But there are some differences between them as follows:

- The credit analysis of banks and other financial institutions focus on borrowing and lending while the latter focusses on investment decision in the equity market.

- The main objective of the former is to assess the credit worthiness of the borrower while extending credit facility while the main objective of the latter is to decide the feasibility of investing in the equity or stocks of an organization.

- In the former the credit rating and financial health of the borrower is assessed, while in the latter the future potential and growth opportunity of the business along with its market capitalization is assessed.

- Even though both evaluates risk, the former assesses the risk of giving loan or debt while the latter assesses the risk of investing in equity.

- The return from the former is interest while the return form the latter is dividend and business ownership.

- For the former, the user is usually the banks and financial institution while the latter’s users are usually analysis and investors.

Thus the above are some important differences between the two concepts.

Frequently Asked Questions (FAQs)

Why credit analysis is essential?

Credit analysis is essential for determining creditworthiness, controlling risk, and making wise loan decisions. It necessitates comprehending the borrower’s capacity to repay loans and their financial background and profile.

What are the documents required to perform credit analysis?

Verifying papers, including identification, a passport, and a company license, among others, is the first step in the traditional credit rating process. The next step is to analyze previous financial data, including balance sheets, financial statements, cash flow, etc.

What is spreading in credit analysis?

The procedure by which a bank enters data from a borrower’s financial statements into the bank’s financial analysis tool is known as financial spreading.

What factors are considered in credit analysis?

Credit analysts consider various factors, including the borrower’s financial statements, credit history, income, expenses, assets, liabilities, industry trends, economic conditions, and the purpose of the credit.

Recommended Articles

Guide to what is credit analysis. We explain the ratios along with examples, fundamentals, how to do, objectives and 5 C’s.