What Is An Interest Rate Cap?

An interest rate cap allows borrowers to set an upper limit on variable interest. If market conditions worsen and the variable interest rate rises beyond the predetermined upper limit, borrowers need not pay extra. The interest cap protects borrowers from an unrealistic rise in loan interest.

Interest Rate Calculator Excel Template

Download Excel Template

To enable interest caps, borrowers must pay an interest cap premium upfront. The interest rate at which the cap provider starts paying the borrower for exceeding the predetermined limit is known as the strike rate. If the strike rate is lower, the income cap premium (initial payment) is higher.

Key Takeaways

- An interest rate cap is an upper limit on variable interest loans. It protects borrowers from abrupt and unexpected changes in loan interests. Not all variable interest loans come with a cap. Instead, it is a specific option.

- It is a form of loan restructuring. Lenders restructure the loan interest or offer financial products with different interest rates if the loan interest exceeds the set limit. Nonetheless, borrowers never pay beyond the limit.

- Interest caps have a nonlinear pricing model and hence are expensive. The longer the capped term, the costlier the premium.

How Does An Interest Rate Cap Work?

An interest rate cap allows borrowers to set an upper limit on variable interest. Thus, if market conditions worsen and the variable interest rate rises beyond the predetermined upper limit, borrowers need not pay extra.

Let us first define the variable interest rate to understand this upper limit better. The variable interest rate is applied to a mortgage or loan. The variable interest rate fluctuates depending on market conditions. The interest levied on variable loans depends on the reference or benchmark rate—an index.

The interest rate varies; neither the lender nor the borrower has any control over it. Therefore, it is also called a floating interest rate or an adjustable interest rate. In contrast, fixed interest rates remain constant throughout the debt obligation.

There is a caveat: to enable this upper limit option in a variable interest loan; borrowers must pay an extra premium upfront. Cap providers charge this fee to restructure the loan. Nonetheless, borrowers reap interest cap benefits throughout the tenure of the loan. This initial payment is called interest cap pricing.

An interest cap agreement mentions three cap pricing determinants:

- Notional Amount

- Strike rate

- Term

The term ‘notional amount’ refers to the size of the cap; typically, notional is the hedging amount of the loan. On the other hand, a strike rate is the interest rate at which the lender starts paying the borrower (for exceeding the predetermined limit). ISo, naturally like, the rate is lower, and the income cap premium (initial payment) is higher.

The upper limit on interest rates is applicable for a pre-determined duration. This duration is referred to as the ‘term.’ Again, the longer the term, the higher the cap price.

The US government mandates a 6% interest cap amendment for military personnel. To avail of this caveat, the individual must have purchased the loan before joining the military. Similarly, some US credit card companies offer annual fee waivers to active-duty military officers (on their travel cards).

Examples

Let us look at some interest rate cap examples to understand the practical application.

Example #1

The interest cap premium formula is as follows:

Interest Premium = (Index Level – Strike Price) x (Days in Period / 360) x (Notional Amount)

Now let us assume that Freddy takes a home loan and negotiates a cap with a 6% strike rate. The loan’s interest is based on LIBOR. This loan carries a notional amount of $9000,000, and the income cap term is 120 days.

On the reset date (day 120), the 4-month LIBOR rate was 9%. Thus, the cap provider paid the following amount to Freddy:

- Interest Cap Premium = (Index Level – Strike Price) x (Days in Period / 360) x (Notional Amount)

- Interest Cap Premium = (9% – 6%) x (120/360) x 9,000,000

- Interest Cap Premium = $90,000

Alternatively, If the 4-month LIBOR rate were 8% at the reset date (day 120), the cap provider would pay the following amount:

- Interest Cap Premium = (Index Level – Strike Price) x (Days in Period / 360) x (Notional Amount)

- Interest Cap Premium = (8% – 6%) x (120/360) x 9,000,000

- Interest Cap Premium = $60,000

If, at the reset date (day 120), the 4-month LIBOR rate would have been at 5%, then the cap provider would not pay any amount to Freddy.

Example #2

In October 2022, non-bank financial institutions (NBFI) of Bangladesh requested the Federation of Bangladesh Chambers of Commerce and Industry (FBCCI) to facilitate relaxation on interest caps.

Bangladesh financial institutions made this formal request based on the financial crisis. Financial institutions also received backing from the Bangladesh Leasing and Finance Companies Association (FCA). The FCA is a regulatory authority for non-banks.

In 2022, the Central Bank of Bangladesh set an interest cap of 7%. But most Bangladesh banks offered the same on deposits, and NBFIs deposit mobilization almost became impossible.

Due to floods and the Covid-19 pandemic, the central bank offered relaxation to bank borrowers. But this relaxation was not offered to non-banks. In addition, non-bank institutions suffered from multiple scams.

Advantages And Disadvantages

The advantages and disadvantages of interest rate cap are as follows:

- An interest cap protects borrowers from sudden or unrealistic interest rate increases.

- If an excessive interest predicament occurs, the loan borrower receives payment from the cap provider. Nonetheless, the interest paid by the loan borrower will always stay within the cap limit.

- If the market rate decreases, borrowers pay lower interest on their loans.

The disadvantages of interest cap are as follows:

- In most cases, people opt for a fixed-interest loan to avoid uncertainty. However, the interest cap structure finds fewer takers due to the complexity.

- Borrowers must be prepared to afford the loan repayment even in worst-case scenarios.

- The initial premium itself is an expensive affair. The longer the capped term, the costlier the premium.

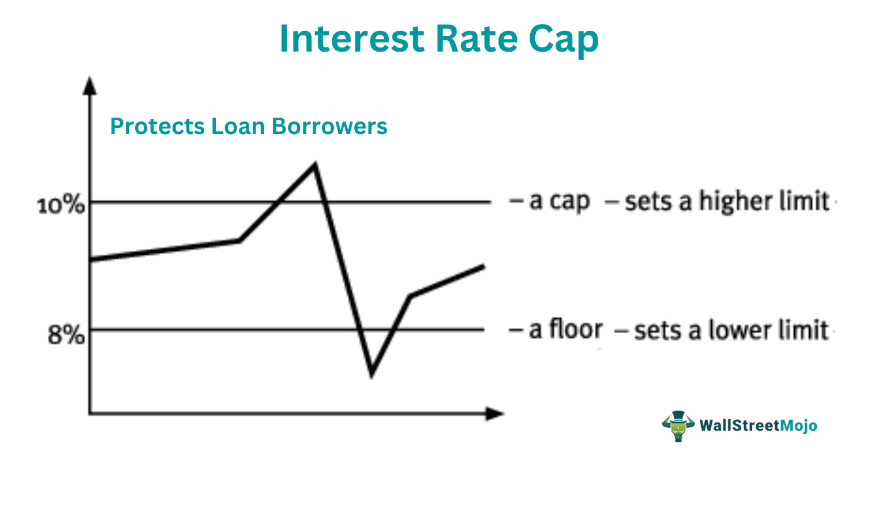

Interest Rate Cap And Floor

Now let us compare the interest rate cap and floor.

- The upper limit on loan interest is called the ‘cap.’ In contrast, the lower limit on loan interest is called the interest rate floor.

- The upper limit protects borrowers. The lower limit protects lenders.

- The upper limit comes into action only when the floating interest rate hits the ceiling (exceeds the strike rate). In contrast, the lower limit is triggered when loan interests fall below the floor rate.

Interest Rate Cap vs Swap

- Interest caps do not allow any midway interest exchanges. However, with interest rate swaps, borrowers can opt for a fixed interest rate after some time.

- If the interest rate exceeds the mutually agreed limit (strike rate), interest cap borrowers receive a premium. That is not the case with interest rate swaps.

- Interest caps are designed to protect borrowers from abrupt interest rate changes. In contrast, interest rate swaps are used to speculate, secure, and hedge credit losses.

Frequently Asked Questions (FAQs)

What is required to purchase an interest rate cap option?

To buy an interest cap option, the following documents are required:

– Legal counsel.

– Regulatory compliance.

– Incumbency certificate.

– Trade confirmation.

How to use an interest rate cap?

When an individual applies for a variable-interest mortgage or loan, they have the option of including an interest cap. The interest cap sets an upper limit on loan interest. If the fluctuating interest rate exceeds the mutually agreed limit, a cap provider pays a premium to the borrower. Thus, borrowers do not have to pay beyond the interest cap.

What does an interest rate cap on a loan mean?

When a borrower applies for a variable-interest loan, the income cap sets an upper limit on loan interest. Borrowers can check for these details in the lending contract.

Recommended Articles

This article has been a guide to what is Interest Rate Cap. Here, we explain it with examples, its advantages, disadvantages, and a comparison with floor and swap. You can learn more about it from the following articles –