Table Of Contents

What Is A Classified Balance Sheet?

A classified Balance Sheet is the type of Balance sheet in which all the balance sheet accounts are presented after breaking them into the different small categories, which makes it easier for the user of the Balance sheet to have a clear understanding by organizing accounts into a more readable format.

A classified balance sheet is a financial document that subcategories the assets, liabilities, and shareholder equity and presents meaningful classification within these broad categories. Simply put, it presents the firm's financial status to the user in a more readable format. It is one step ahead of the balance sheet, which is nothing but a way of representing the valuation of the assets and liabilities.

Table of contents

- What Is A Classified Balance Sheet?

- A classified balance sheet refers to a balance sheet in which every balance sheet account is shown after classifying them into various small sections. It makes it easy for the balance sheet to understand by arranging arrangements in a more readable format.

- It is a financial instrument that sorts the assets, liabilities, and shareholder equity and displays significant divisions.

- It also makes it uncomplicated for regulators to know any matter in the initial stages instead in the final stages when unrepairable harm has already occurred.

Classified Balance Sheet Explained

A classified balance sheet lists the standard contents of a normal balance sheet, which include the assets, liabilities and the value of the equity but there are further classifications or categories of each. It is a more detailed approach, whereby the business will organize the data in such a manner so that more specific and detailed information is available to whoever tries to analyse or read it.

Such details in the classified balance sheet format help in getting a good breakup of the assets, liabilities and equity related information and understand the cash flow situation well.

- When a firm publishes a classified balance sheet, it presents the valuation of its assets and how these current valuations have been calculated. Accounting is more science than math; there can be multiple ways of reporting an asset.

- Some assets are valued at historical or book value, like land and machinery, and some have a more complex way of calculating, like goodwill and brand name.

- The classified balance sheet makes sure that all these calculations are properly communicated to the reader. Although there are no set rules for these classifications as an implicit industry practice, most businesses prefer reporting assets and liabilities based on a time horizon.

However, even though such classification are very useful and provide more meaning to the document, the format may vary according to the company rules or the industry. The rules, regulations and requirements of financial reporting also have a lot of influence on these statements.

How To Prepare?

Understanding the method of preparation of this kind of balance sheet is important. It involves complex process since there is a lot of break up an details. However, let us learn the steps to prepare sample classified balance sheet.

- List of assets and liabilities- This is a very important first step where the company has to prepare a detailed list of all the assets and liabilities, which will include the long-term, short term investments, cash and cash equivalent, account receivable, invesntory, goodwill, plant and machinery, tangible and intangible assets, short or long term debts, accrued expense, deferred revenue, pension obligation, etc. . This details has to be thorough and accurate so that it gives the correct and transparent information and asset and liability status.

- Shareholder’s equity – The calculation of shareholder’s equity is equally important, which will show the breakup of share capital and capital structure like the common stock, the treasury stock, etc, retained earnings details, the amount of net income and any additional paid-in capital.

- Balance sheet format – The next step is to prepare the balance sheet as per the format and listing all the details as highlighted above.

- Cross-checking – This helps to ensure that all data and financial information is properly and clearly displayed as per requirement, and it gives a confirmation of the true and fair view of financial position of business. This step helps in checking for accuracy and completeness of calculation. The company management should take special care to do this.

Therefore, the above steps are essential to prepare a classified balance sheet complete the process so that it can be used by the management and other stakeholders for analysis and investment decisions.

Examples

Let us understand the concept of sample classified balance sheet with the help of some suitable examples.

Example#1

The following table shows the Classified Balance Sheet example format for a garment firm.

As shown above, in the Classified Balance Sheet example, there are proper classifications that help the reader identify the assets or liabilities and their type. It improves readability and leaves little for interpretation, emphasizing transparency and the clarity of the management strategy.

Example#2

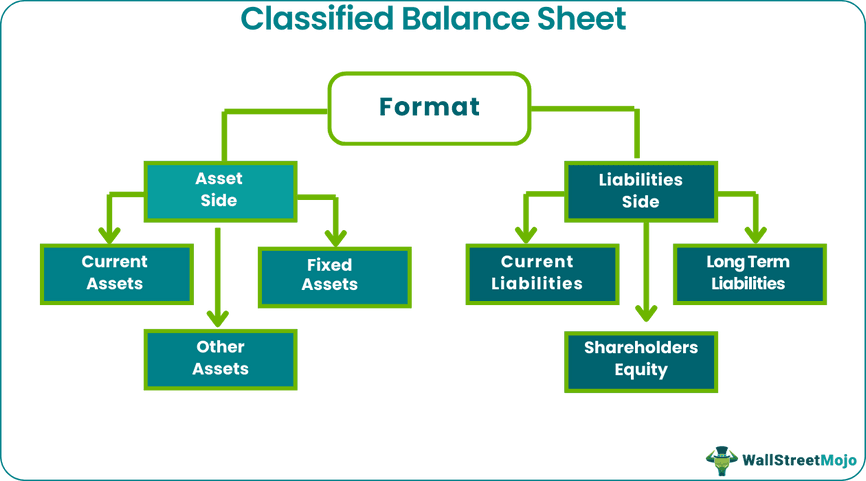

The format of the classified balance sheet 's asset side can be divided into three main categories.

#1 - Current Assets

source: Starbucks SEC Filings

These are the assets that are supposed to be consumed or sold to utilized cash within the operating cycle of the business or with the current fiscal year. They are mainly required to fund the daily operations or the firm's core business. An important characteristic is that they can be easily liquidated to generate cash, which helps a business meet any short-term liquidity crunches. Although they vary from industry to industry, some common examples can be cash, cash equivalents, Inventory, accounts receivable, etc.

#2 - Fixed Assets

Fixed Assets are those long-term assets that are utilized in the current fiscal year and many years after that. They are mainly one-time strategic investments that are needed for the long-term sustenance of the business. For an IT service industry, fixed assets will be desktops, laptops, land, etc., but it can be machinery and equipment for a manufacturing firm. An essential characteristic of fixed assets is that they are reported at their book value and normally depreciate with time.

#3 - Other Assets

The third category is the list of intangible assets that the firm has acquired over some time. These Include goodwill, brand name, patents, copyrights, trademark, etc. They have a multi-period life. An essential characteristic of intangible assets that differentiates them from fixed assets is that they normally do not depreciate with time. Their value increases as the firm grows and spends more time in the industry.

Example#3

The format of the classified balance sheet 's liabilities side can be divided into three main categories.

#1 - Current Liabilities

Current liabilities like current assets are assumed to have a life of the current fiscal year or the current operating cycle. They are mainly short debt expected to be paid back using current assets or by forming a new current liability. The critical point is they have to be settled fast and are not kept for later payments. Examples of current liabilities include accounts payable, accrued liabilities, current portion of long term debt (CPLTD), deferred revenue, etc.

#2 - Long Term Liabilities

Long term liability is obligations that are supposed to be paid back in the future, possibly beyond the operating cycle or the current fiscal year. They are like long term debt where payments can take 5, 10, or maybe 20 years. Examples of long term liability can be corporate bonds, mortgages, pension liabilities, deferred income taxes, etc.

#3 - Shareholders Equity

The shareholder equity section mainly provides information about how the firm has been financed and how much profit it retains to reinvest further in the business. Items included in Shareholders' equity are common stock, additional paid-in capital, retained earnings and accumulated other comprehensive gains/losses, etc.

Balance Sheet Video Explanation

Purpose

A classified balance sheet format provides a crisp and crystal clear view to the reader. Although balance sheets are prepared they are read by normal investors who might not have an accounting background. The different subcategories help an investor understand the importance of a particular entry in the balance sheet and why it has been placed there. It also helps investors in their financial analysis and makes suitable decisions for their investments.

For example, an investor interested in the day-to-day operations and profitability of the firm would like to calculate the current ratio. He would have to deep dive into every section in a normal balance sheet and read notes specifically for each asset and liability. However, in a classified balance sheet format, such a calculation would be straightforward as the management has specifically mentioned its currents assets and liabilities. It will be easy to figure out and calculate even for a retail investor.

A well-represented and well-classified information instills confidence and trust in the creditors and investors. It conveys a strong message to the investors that their money is safe as management is serious about the business's profitability and running it ethically and within the rules of the land. It also tells a lot about management, who wants to be open about their assets and valuations and how these valuations have been calculated. Publishing a classified balance sheet also makes it easy for regulators to point out an issue in the initial stages rather than in the final stages when irrevocable damage has already been done.

Classified Balance Sheet Vs Balance Sheet

The classified balance sheet format and the regular balance sheet are two methods of presenting financial data to management, shareholders, analysis and other investors. But there are some differences between the two formats. Let us study the same.

- There is a significant difference in the level of details provided in the two formats. In case of the order of classified balance sheet, the breakdown of assets, liabilities and equity position is more. There are more subheads and more data revealed. The latter is more compact, and the subheads are totalled up to reveal a comprehensive figure. Even though the figures are accurate, it is not possible to get mouch details.

- The order of classified balance sheet helps in getting a clearer view and assess the financial position of the business with clarity. But this is sometimes tougher and complex in case of the latter because of less amount of information available.

- The liquidity position, which is extremely crucial for any business is best revealed using the former. This greatly helps investors to assess the sustainability and future potential of the company.

- The former is a view that can be used for better analysis and decision making, while the latter is a snaphot of the financial health of the company at a certain point of time.

The above are some basic differences between the two categories of balance sheet.

Frequently Asked Questions (FAQs)

A classified balance sheet is identical to a traditional balance sheet. It shows similar asset, liability, and equity values. However, unlike a typical balance sheet, the classified sheet bifurcates the assets, liabilities, and equity into other different sections for each type.

A common stock dividend distributable is shown in the shareholders' equity area of the balance sheet, and a cash dividend distributable is shown in the liabilities section. Hence, on the classified balance sheet, dividends would be reflected as a reduction in the stockholder's equity section, specifically in retained earnings account.

A classified balance sheet displays details about a business's assets, liabilities, and shareholders' equity divided into account subdivisions.

Recommended Articles

This article has been a guide to what is a Classified Balance Sheet. We explain it with examples, differences with balance sheet, how to prepare & purpose. You may learn more about our articles below on accounting –