Part of our Balance Sheet guide

What is Balance Sheet Reconciliation?

Balance Sheet Reconciliation is the reconciliation of the closing balances of all the company accounts that form part of the company’s balance sheet to ensure that the entries passed to derive the closing balances are recorded and classified properly so that balances in the balance sheet are appropriate. A balance sheet reconciliation policy helps in gaining important insights into the financials of a company.

The balance sheet reconciliation process forms part of the balance sheet items for a respective financial year and whether it is recorded and properly classified, making up for the balances appropriately in the balance sheet. It is a final and crucial activity that the company performs to ensure the accuracy of its financial statements before the closing of its books at the end of the financial cycle.

Balance Sheet Reconciliation Explained

Balance sheet reconciliation is a process where a business or an individual closes all balances of individual accounts as part of their balance sheet. This process ensures that all accounts are documented properly before filing every financial year.

Generally, a statement from each account and the bank statement are compared with each other, and entries with inconsistencies are compared and adjusted according to the norms. In the modern day, balance sheet reconciliation software has been very useful in making the process extremely efficient.

It is vital for a company to close all their unbalanced entries before arriving at their net profit or loss of that assessment year before filing their returns. Different organizations would have different strategies to document, maintain, and review their books of accounts based on the nature of their business, management style, and industry norms.

However, it is important to note that maintaining the same protocol for maintaining accounts must be followed within the same accounting or assessment period as different methods would create confusion and spill out inconclusive data for the accountant or auditor to review and file.

Purpose

Balance sheet reconciliation policy is a vital financial control process that ensures the accuracy, integrity, and compliance of an organization’s financial data. Let us understand the very purpose it is practiced so widely across businesses.

- Accuracy Verification: Balance sheet reconciliation ensures that all financial transactions and account balances are accurately recorded, helping to identify errors or discrepancies.

- Fraud Detection: It serves as a critical tool in detecting and preventing financial fraud by highlighting any unauthorized or suspicious transactions.

- Compliance Assurance: Reconciliation helps ensure compliance with accounting standards and regulatory requirements, providing an audit trail for external auditors.

- Decision-Making Support: By providing an accurate and up-to-date financial snapshot, reconciliation assists management in making informed decisions about the company’s financial health and strategy.

- Risk Mitigation: It reduces the risk of financial misstatements and mismanagement by identifying and rectifying errors promptly.

- Investor Confidence: Accurate financial reporting through reconciliation enhances investor trust and confidence in the company’s financial statements.

- Efficiency Improvement: It streamlines financial processes and record-keeping, making them more efficient and cost-effective.

Types

Let us understand the types followed by companies in their balance sheet reconciliation softwares through the discussion below.

There are two formats in which a balance sheet can be prepared. One is the horizontal format, called the T-format, and the other format is the Vertical Format. Presently the vertical format is widely in use. The contents in both formats are, however, the same. It is only the way it gets presented that is different.

The balance sheet components of the balance sheet comprise data, which would either increase or decrease revenue. Hence many of these would have already been computed. In contrast, the preparation of income and expense / Profit and Loss statements, and a few that would be carried forward from the previous year’s balances shall merely have the final balances available in these accounts.

Ideally, a balance sheet would have the following components:- “Assets, Liabilities, and Owner’s Equity.”

- Assets are items that would likely increase or generate revenue for the company: cash, receivables, inventory, prepaid expenses, and fixed assets, etc.

- Liabilities are items that would likely decrease the revenue for the company. Examples: Debts, accounts payable, payroll and taxes payable, notes payable, deferred revenue, and customer deposits, etc.

- There is no such formula to calculate the balance sheet as it is a statement to match the total liabilities with total assets. However, this can be represented in the following form:- Assets + Owners Equity = Liabilities.

Process

Balance sheet reconciliation policy is a crucial part of financial control and reporting, helping organizations maintain the integrity of their financial data. Let us understand the process through the step-by-step guide below.

- Data Gathering: Gather all relevant financial data, including bank statements, general ledger entries, accounts receivable/payable records, and any other pertinent documents.

- Identify Discrepancies: Compare the data from various sources to the corresponding entries in the general ledger. Identify discrepancies, such as missing transactions, errors, or inconsistencies.

- Investigate Discrepancies: Investigate the root causes of discrepancies. This may involve communicating with other departments, reviewing invoices, or clarifying entries with colleagues.

- Adjust Entries: Make any necessary adjustments to the general ledger to rectify errors or omissions. This might include journal entries, correcting misclassified transactions, or updating balances.

- Document Reconciliation: Document the reconciliation process thoroughly. Maintain records of the steps taken, the individuals involved, and any adjustments made during the process.

- Review and Approval: Have the reconciliation reviewed and approved by a supervisor or manager to ensure its accuracy and compliance with company policies. Once discrepancies are resolved and approvals obtained, finalize the reconciliation and obtain sign-off as an acknowledgment of its completion.

- Reporting: Prepare a reconciliation report summarizing the findings and any adjustments made. This report is often part of the company’s financial documentation and may be subject to external audit.

Balance Sheet vs. Consolidated Balance Sheet Video Explanation

Template

A balance sheet reconciliation software template has been provided below for a better understanding of the concept and its intricacies.

| Company Name | |||||

| Balance Sheet as at MM/DD/YYYY | |||||

| Fixed assets | |||||

| Intangible assets | xxx | The total value of development costs incurred by the business plus the cost of the license it holds for selling its goods. | |||

| Tangible assets | xxx | It is the cost of the business premises, furniture | |||

| and equipment, less depreciation charged since first using the assets | |||||

| Investments | xxx | It is the value of shares owned in DEF Utilities PLC. | |||

| xxx | |||||

| Current assets | |||||

| Stock | xxx | It is the total value of goods bought from suppliers that have not yet been sold plus raw materials held for production plus the value of work in progress | |||

| Debtors | |||||

| Trade debtors | xxx | It is the total of the amounts customers owe, less bad debts and uncollectible amounts. | |||

| Prepayments and accrued income | xxx | The maintenance fee is payable annually in advance to the computer software company. | |||

| xxx | |||||

| Cash at bank and in hand | xxx | It is the total of cash kept on site and the balance on the business’ current account with the bank. | |||

| xxx | |||||

| Creditors: amounts falling due within One Year | Also known as current liabilities – liabilities are shown as negatives because they are amounts owed by the business. | ||||

| Bank loans and overdrafts | xxx | It is the portion of the business’ bank loan that will be repaid in the next twelve months. | |||

| Trade creditors | xxx | It is the total of the amounts owed by the business to its suppliers for goods it bought to sell to its customers. | |||

| Other creditors including tax and social security | xxx | The value of tax and national insurance contributions deducted from employee salaries has not yet been paid over to the Inland Revenue. | |||

| Accruals and deferred income | xxx | It includes interest due to the bank loan since the last repayment. | |||

| xxx | |||||

| Net current assets | xxx | Also known as working capital – this shows the business’ ability to meet current obligations. | |||

| Total assets less current liabilities | xxx | ||||

| Creditors: amounts falling due after more than one year | |||||

| Bank loan | xxx | It is the portion of the business’ bank loan, which is due to be repaid in over one year. | |||

| Net assets | xxx | ||||

| Capital and reserves | |||||

| Called up share capital | xxx | These are the funds invested by the owners in the business, e.g., to finance its assets. | |||

| Profit and loss account | xxx | These are the profits made since the start of the business, fewer expenses, and amounts paid to the owners as dividends. | |||

| Shareholders’ funds | xxx |

Examples

Let us understand the balance sheet reconciliation policy in depth with the help of a couple of examples.

Example #1

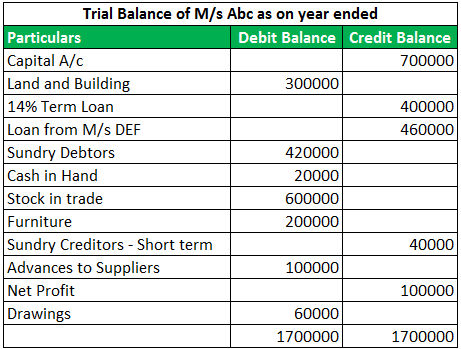

Following is the trial balance of M/S ABC at the end of the year. Prepare a balance sheet for the same.

Solution:

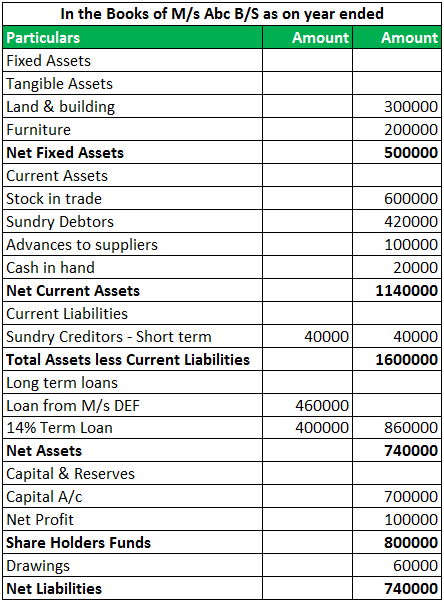

Below is the reconciliation of the Balance Sheet.

We note here that the total net assets are equal to total net liabilities (740,000)

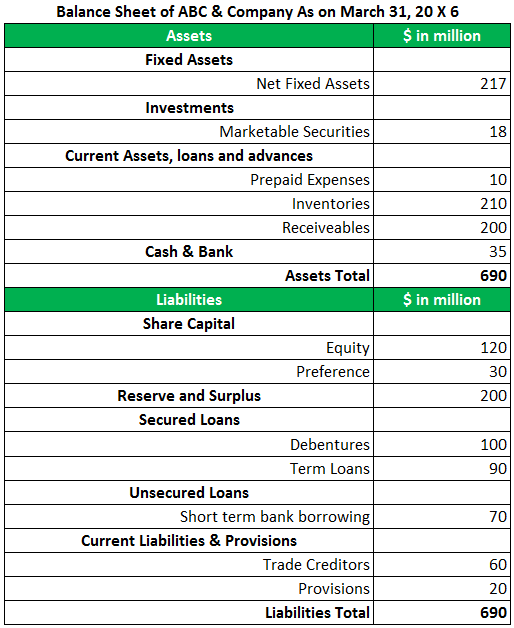

Example #2

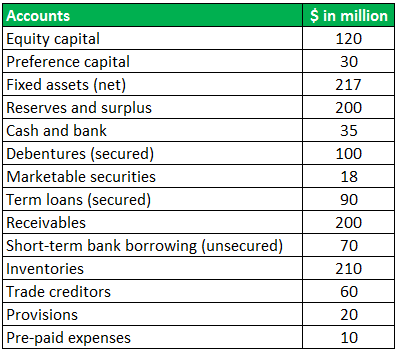

At the end of March, 20X6 the balances in the various accounts of ABC & Company are as follows:

Prepare the balance sheet of ABC & Company as per the format.

Solution:

Below is the balance sheet reconciliation.

Again, we see that the total assets are equal to total liabilities.

Importance

Let us understand the importance of balance sheet reconciliation policy through the points below.

- Balance sheet reconciliation is essential for verifying the accuracy of financial data and ensuring that a company’s assets, liabilities, and equity are correctly stated.

- It helps identify errors, omissions, and discrepancies in financial records, preventing inaccuracies in financial statements.

- It ensures compliance with accounting standards and regulatory requirements. Proper reconciliation provides a clear audit trail, demonstrating accountability to external auditors, investors, and regulatory bodies.

- Regular reconciliation helps detect and prevent financial fraud or misappropriation of assets. It can uncover unauthorized transactions or irregularities that may indicate fraudulent activities.

- Accurate financial data resulting from reconciliation supports informed decision-making by management and stakeholders. It provides a reliable basis for evaluating the company’s financial health and performance.

- Reconciliation helps mitigate financial risks by promptly identifying and rectifying errors and discrepancies. It reduces the likelihood of financial misstatements and the associated legal and reputational risks.

- Investors and creditors place trust in a company that maintains accurate financial records through reconciliation. This confidence can lead to better access to capital and lower borrowing costs.

Advantages

The adoption of balance sheet reconciliation software has helped countless companies settle their accounts or close them in time before filing for that assessment period. Let us understand the other advantages of this necessary function of accounting through the discussion below.

- Eliminates accounting errors

- To better understand and evaluate the financial strength of the company

Disadvantages

Despite the advantages mentioned above, there are a few factors that act as a hassle for accountants and auditors while reviewing the books of accounts. Let us understand the disadvantages of the balance sheet reconciliation policy through the points below.

- Manual reconciliation of balance sheets or accounts is prone to errors.

- Hence, it involves a risk of data manipulation, missing the recording of data, etc.

- It is a time-consuming process. Therefore, the cost of maintenance of accounts also increases.

- Requires reviews at multiple levels to ensure all errors are eliminated.

- With bank entries, it sometimes happens that the entry in the bank’s statement has a different date than that of the company’s books. This can cause confusion if there are entries with the same amount on different dates.

- Cheques issued but not cleared yet can make it look like the transaction has not been initiated at all.

Recommended Articles

It has been a guide to what is Balance Sheet Reconciliation. Here we explain its example, types, advantages, and disadvantages, and provided a template. You can learn more about accounting from the following articles –