What is a Statement of Financial Position?

Statement of Financial Position, also known as the Balance sheet, gives the understanding to its users about the business’s financial status at a particular point in time by showing the details of the company’s assets along with its liabilities and owner’s capital.

It is one of the most important financial statements which reports the firm’s financial position at a point in time. In other words, it summarizes a business’s financial position and acts as a snapshot of events at one point in time. It comprises three important elements (explained in detail later), namely:

- Assets are the resources owned and controlled by the business. Assets are further classified into Current Assets and Non-Current Assets.

- Liabilities are the amount of business owing to its Lenders and Other Creditors. Liabilities are further classified into Current Liabilities and Long Term Liabilities.

- Shareholder’s Equity which is the residual interest in the Net Assets of a business that remains after deducting its liabilities.

The Fundamental Accounting Equation (also known as the Balance Sheet Equation) through which transactions are measured equates:

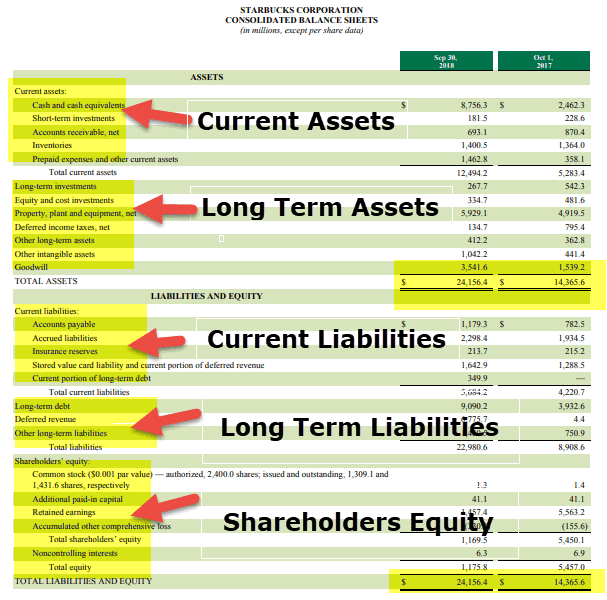

Financial Position Statement Example

Let’s take a look at an example of Starbucks as on September 30, 2018

source: Starbucks SEC Filings

Effectively the above example consists of two lists:

- A list of everything owned by the business collectively called Assets

- A list of the various sources of finance used to fund these acquisitions can be either in the form of Liabilities or Shareholders’ Equity.

Thus, it is a statement showing the nature and amount of a business’s assets and liabilities and Share Capital on the other side. In other words, the Balance Sheet shows the financial position on a particular date, which is usually at the end of a year.

The Statement of Financial Position shows how the money has been made available to the company’s business and how the money is employed in the business.

The format of the Financial Position Statement

Let’s understand the Statement of Financial Position format in more detail.

#1 – Current Asset

Current Assets are those cash and items which will be converted into cash in the normal course of business within one year and includes Inventory, Trade Receivables, Bill receivable, etc. The Total Current Assets are referred to as the Gross Working Capital, also known as the qualitative or circulating capital.

#2 – Current Liabilities

Current includes all liabilities which are due within one year and includes Trade Payables, Creditors, short term borrowings such as Bills Payable, Deferred Tax Liabilities, Current Portion of Long term Borrowings, which are payable within the year, etc.

#3 – Long Term Asset

Noncurrent Assets, also known as Fixed Assets, are those assets that are bought to use in the business and usually have long lives. They may include tangible assets such as Land, Property, Machines, vehicles, etc. Tangible Noncurrent Assets are generally valued at Cost less Accumulated Depreciation. However, it is pertinent to note that not all Tangible Assets depreciate, such as Land.

- Intangible Noncurrent Assets are noncurrent assets that cannot be touched. The most common type of Intangible Assets is Goodwill, Patents, and Trademarks. Goodwill is subject to an Annual Impairment Test.

- Noncurrent Assets include investment in other companies in Shares, Debentures, loans, etc. The business intends to hold the same for a reasonable period, say more than a year.

#4 – Long Term Liabilities

Non-Current Liabilities include Long term borrowings that are not due within one year. It includes finance leases, medium-term bank loans, Bonds and Debentures, and contingent liabilities such as Guarantees, etc.

#5 – Shareholders Equity

Shareholders Equity is the amount contributed by the shareholders/owners of the business in shares. Alternatively, Shareholder’s Equity is the Net value of the business, which is derived by subtracting Assets from Liabilities.

Briefly Equity comprises of:

- Common Stock

- Retained Earnings which includes the number of profits retained by the business;

Limitations

We saw how a Statement of Financial Position depicts the position of the business on a particular date. However, despite so many benefits that it offers to various stakeholders of the business, it suffers from certain limitations, which are as enumerated below:

- This statement is prepared based on going concern assumption and, as such, represents neither the realizable Value nor replacement value of Assets.

- Valuation of Assets is substantially impacted by the judgment of Management and various accounting policies adopted by them.

- It considers only financial factors and fails to quantify non-financial factors that have considerable bearing on the operating results and financial condition of an Enterprise.

- It shows the historical cost and does not disclose the current worth of the business.

Recommended Articles

This article has guided what the Statement of Financial Position is. Here we discuss the format of the Financial Position Statement along with practical examples and limitations. You may also have a look at the related articles: