Part of our Banking Ratios & Metrics guide

What Is A Banks Balance Sheet?

→ Explore all 93 Balance Sheet articles

A banks balance sheet refers to the financial statement prepared by the banks based on which the current status and performance of the entity in the banking industry can be assessed and analyzed. The main elements if this balance sheer are assets, liabilities, and the bank capital.

The bank’s balance sheet is different from the company’s balance sheet. It is prepared only by the banks according to the mandate of the Bank’s Regulatory Authorities to reflect the tradeoff between the bank’s profit and the risk of its financial health.

- A bank’s balance sheet provides a snapshot of its financial position at a specific time. It consists of assets, representing what the bank owns, and liabilities, describing what it owes to its depositors and other creditors.

- Banks typically have a significant portion of their assets in the form of loans. These loans include mortgages, commercial loans, consumer loans, and other types of credit extended to borrowers. The quality and performance of the loan portfolio directly impact the bank’s profitability and risk profile.

- The balance sheet also reflects the bank’s capital position, which indicates its ability to absorb losses and support its operations. Capital adequacy is crucial for banks to maintain financial stability and meet regulatory requirements. It is measured through capital ratios such as the Tier 1 and total capital ratios.

Banks Balance Sheet Explained

Banks Balance Sheet reflects the capacity of the banking institutions to lend money to customers. The assets in the financial statement for banks are the lending resources available with the banks, while the liabilities in these balance sheets indicate the deposits that customers make along with other financial instruments that it possesses.

Assets here are the resources that make the banks capable of financing lending requirements of customers. Hence, this section includes loans, securities, and reserves that they have. Liabilities is the fund coming to the bank from customers, which has to be handed over to the latter whenever they need to. Hence, they become liabilities instead of assets for banks.

The third element in the bank balance sheet is the capital, which is also referred to as net worth, equity capital, or bank equity. The bank capital comprises funds raised by selling equity or finances that come from the profits, which are the retained earnings of the entity. In the case of the banks, the profits are generated from the assets driven by the liabilities they accumulate.

The balance Sheet for banks is different from the balance sheets prepared by other sectors and companies. Several characteristics of the bank’s financial statement highlight how banks’ balance sheets and income statements are created. For example, sales are not measured by ratios like sales turnover and receivables turnover. Once investors are comfortable with the terminology and can grasp the statements, it becomes elementary for them to analyze the trends and understand the statements.

How To Read?

The balance sheet of a bank is easy to read when one is aware of the components and what those components signify. This balance sheet is prepared based on the expression below:

Assets = Liabilities + Capital

However, these elements are available in the form of several other components, understanding which makes reading the balance sheet easier. The main components of the above bank’s balance sheet are:

The main components of the above bank’s balance sheet are

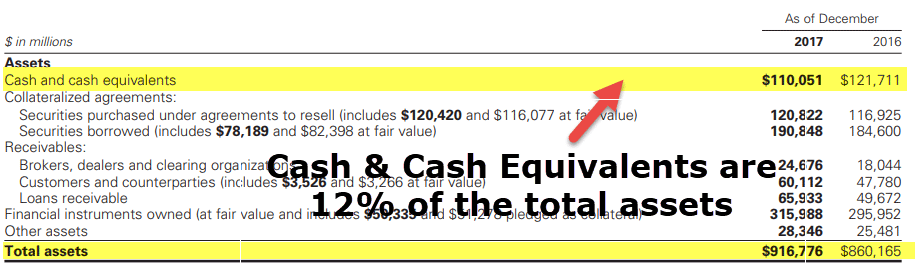

#1 – Cash

- Holding a large amount of cash is considered a loss in opportunity cost for other sectors. But in the case of a Bank’s Balance Sheet, cash is a source of income and is held on deposit. Sometimes banks also hold cash for other banks, and one of the significant services banks provide is to provide cash on demand.

- Due to its business and regulatory norms, banks must have a minimum amount of liquid cash. Most often, banks keep excess reserves for higher safety. Goldman Sachs has a considerable amount of cash balance.

- In 2017 it had ~12% of its balance in cash and equivalents. This is an essential focus for the investors since the chances of receiving a higher amount of dividend or share buyback increases.

#2 – Securities

- These instruments are typically short-term, and banks generate a yield from these kinds of investments. Banks own US Treasuries and municipal bonds.

- These securities are liquid and can be easily sold in the secondary market and hence are termed secondary reserves. Goldman has increased its investment in securities in 2017.

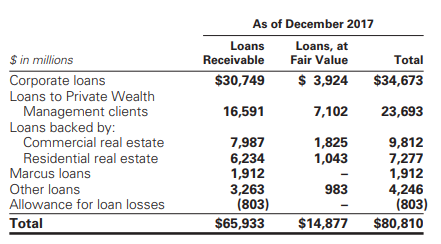

#3 – Loans

Lending money and earning interest is the primary business of the bank. Therefore, it can be termed the bread and butter of the bank.

- From an investor’s perspective, the increase in loans is essential for the bank’s growth. Along with the increase in loans, bank deposits should also be observed. An increase in loans is alone not sufficient. The quality of creditors should be noted. Poor quality of creditors may lead to a rise in default rates and, in turn, a loss for the banks.

- On a broad level, banks provide Personal and mortgage loans. Personal loans are given without any security, and hence interest for these loans remains high. In the case of mortgage loans, the loan is given against a mortgage, and the interest is lower. But if the loan taker defaults on its loan, the bank claims the mortgage as per the agreement.

- Banks also provide loans for business, and real estate loans, which include but are not limited to residential loans, home equity loans and commercial mortgages, consumer loans, and interbank loans.

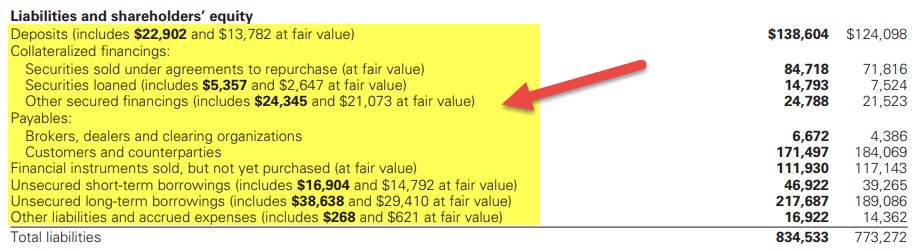

#4 – Deposits

- Deposits fall under the liability portion of the banks’ balance sheet and are mainly the most substantial liability for the bank. It includes money market, savings, and current accounts and has both non-interest and interest bearing accounts.

- Deposits are considered liabilities, but they are also crucial in determining a bank’s lending ability. If the bank does not have sufficient deposits, it will not be able to lend, and the loan growth will also be hampered. Banks may have to take on debt to meet the loan growth, which would cost them more than the rate they might receive on loans.

- Also, this is not a sustainable way for banks to grow their loans. After a certain point, the debt amount will reach an extent where the bank will not get any credit, and if the bank fails to pay on its payments, it will lead to a crash.

- Banks use these liabilities to generate more income, which earns them additional income. By using these deposits to finance loans for individuals etc. Banks will be able to leverage this additional capital to make the extra income that they might have otherwise earned through the capital.

- Banks also have an allowance in the balance sheet for covering losses, and the changes in this amount are based on economic conditions.

Examples

Let us consider the following examples to understand the conceptual and complex instances, respectively to know how the records are maintained.

Example #1

Let us check the banks balance sheet format in which Bank A presents its financial details:

| Assets | Liabilities |

|---|---|

| Reserves – $10,000 Securities – $60,000 Loans – $150,000 Other assets – $17000 | Check deposits – $25,000 Non-transaction details – $126,000 Borrowings – $66,000 Bank Capital – $20,000 |

Example #2

Below is the example of the Consolidated balance sheet of Goldman Sachs for the years 2017 and 2016 from their Annual 10K

Balance Sheet Assets

source: Goldman Sachs SEC Filings

- We note that the bank’s balance sheet assets are different from what we usually see in other sectors like Manufacturing etc. The classification is not based on current assets, long-term assets, inventory, payables, etc.

- The key highlight is that bank assets include securities purchased, loans, financial instruments, etc.

Balance Sheet Liabilities

- The bank’s balance sheet liability section looks very different from the ordinary liabilities (current liabilities, long term liabilities, etc.).

- Here are the key terms to note: deposits, Securities under repurchase agreements, short term and long term borrowings, etc.

Balance Sheet Video Explanation

Accounting Rules

Capital is determined by Total Assets and less total liabilities (also known as net worth). However, the recent changes have changed this definition and have made it complex to determine the true value of the bank’s net worth.

Post-2009 crisis, the government took specific initiatives to restore faith in the banking system. The Financial Accounting Standards Board has allowed Banks to value their assets at a Fair Value. Banks are now also allowed to record income on the income statement if the market value of the debt decreases. This change is because the bank could buy its debt in the market and reduce the debt amount.

Important Indicators

The word “Default” means failure to meet interest or payment obligations. Usually, banks use a Non-performance ratio, a percentage indicating the number of loans given on credit is expected to fail. This comparison helps us understand if the bank has sufficient funds to meet future contingencies.

Widely used ratios include –

- Non-performing loans / Customer loans

- Non performing loans / Customer loans + collateral

- Non-performing loans / Average total assets

- Own Resources / Average total assets

Non-performing assets or loans to loans ratio is used to measure the overall quality of the bank’s entire loan book. Not performing loans are the ones for which interest is overdue for more than three months

The third ratio is especially significant for institutions already in a bad place. When this ratio crosses a benchmark, it is considered a strong sign of insolvency

The higher fourth ratio indicates that the bank is highly leveraged, and there is lower protection against defaults on the loans mentioned above on the asset side.

Frequently Asked Questions(FAQs)

1. What is the significance of assets and liabilities on a bank’s balance sheet?

Assets represent the resources owned by the bank, such as cash, loans, investments, and physical assets. Liabilities represent the bank’s obligations to depositors, creditors, and other stakeholders.

2. How are loans classified on a bank’s balance sheet?

Loans on a bank’s balance sheet are typically classified based on their credit quality and risk of default. They are categorized into different segments, such as performing loans, non-performing loans, and specific provisions for impaired loans.

3. Why is capital adequacy important for banks?

Capital adequacy ensures that banks have sufficient capital to absorb potential losses and maintain financial stability. It is a buffer against unexpected events, economic downturns, and loan defaults.

Recommended Articles

This article has been a guide to what is Banks Balance Sheet. Here, we explain the concept along with its examples, how to read it, accounting rules, etc. You may learn more about accounting from the following articles –