Part of our Types of Taxes guide

What Is Franchise Tax?

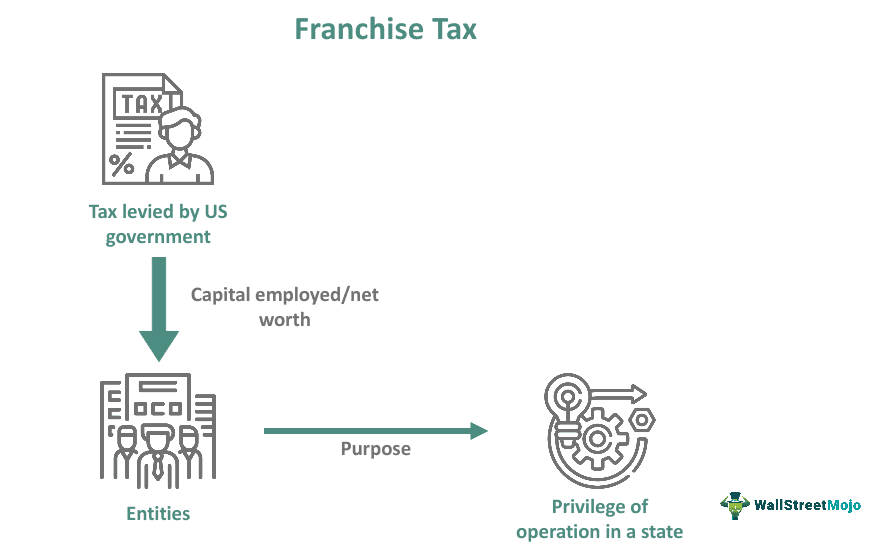

The franchise tax is a levy charged by the government in some US states for the privilege available to the entity to exist and operate within that particular state. The tax is levied on net worth or capital of the entity, and not on the income earned by the entity.

This tax is used to generate revenue for that particular state, and that it is a cost that the companies pay for using the facilities of that state, The tax helps in financing for infrastructure development in the form of education, transportation, and healthcare. Thee tax amount is not the same for all states.

Franchise Tax Explained

Franchise tax is a type of tax that some states of the United States put on the companies or organizations that operate in those areas. This is a kind of compensation or cost that these entities bear for using the amenities and infrastructures of those places.

It is a good source of revenue for the states. And helps in funding infrastructure projects and development like healthcare, education, etc. The franchise tax board collects the amount of tax that depends on the state’s rules. Still, it is generally levied on all business corporations, sole proprietors, partnerships, or limited liability companies.

In some states certain types of business does not have to pay this tax. These business include very small business or any non-profit entity. The tax is charged based on the net worth or the total assets of the organization. Sometimes the calculation can be very complicated because of not only the size of the business but also the rules of the state.

The organizations should follow the rules of the tax as per the state and follow them because if they do not do so, then penalties and interest charges are imposed on them, and the states can take legal action. Companies should ensure such compliance with the help of tax experts.

This tax is the best and most effective way of collecting the cost of any privilege that the companies get by operating in those places of United States,

How Is Franchise Tax Calculated?

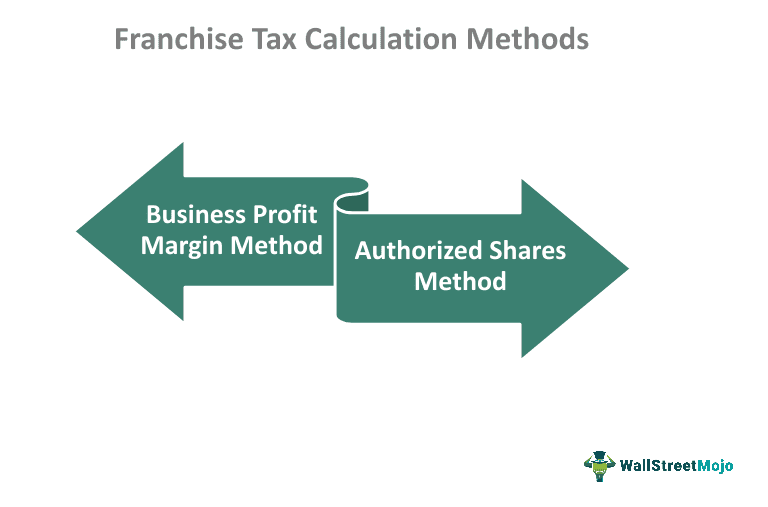

Now let us learn about the various method of calculating the tax. The franchise tax board might levy the tax based on the following methods:

#1 – Business Profit Margin Method

Under this, the profit margin is calculated first by subtracting costs and expenses from the corporation’s revenue and multiplying the margin by a percentage of business done in that state. For example, if a corporation does only 70% of its business in that state, then tax will be calculated on a 70% margin. For a corporation that operates entirely in the state will pay franchise tax on 100% of profits. The margin calculated is then taxed as per applicable tax rates of the state.

#2 – Authorized Shares Method

The tax is calculated by multiplying the total number of authorized shares the company has as per its charter by the tax prescribed per share.

Examples

Let us understand the above methods of preparing the franchise tax report by way of examples.

#1 – Business Profit Margin Method

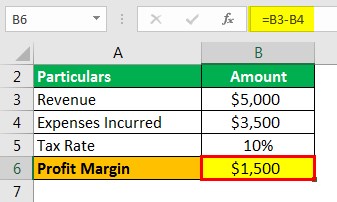

A company has earned a revenue of $5,000 during the year. Also, the company incurred expenses of $3,500 to earn revenue. The jurisdictional state levies tax at the rate of 10%.

Solution

Calculation of Profit Margin

- = $5,000 – $3,500

- Profit Margin = $1,500

Franchise Tax can be calculated as 10% on the profit margin as follows:

- = $1,500 * 10% = $150

#2 – Authorized Shares Method

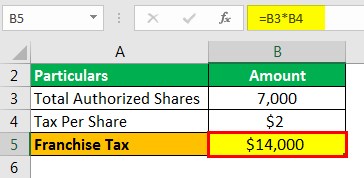

A company has 7,000 of total authorized shares. The state levies a franchise tax of $2 per share. Therefore, as per the calculation of the method, the amount of the tax will be as follows.

Solution

- = $2 * 7,000

- = $14,000

How To Pay?

Now let us look at the basic procedure to pay it. Following steps need to be followed by the company to pay Franchise Tax in the state of Texas:

Estimation of tax as per the state laws

Based on whichever method the state prescribes.

File the tax report.

The franchise tax report contains the details of the revenue as well as the calculation of tax paid. In addition, there can be the following types of returns:

– No tax due: If the annual turnover falls below the prescribed limit, no franchise tax will be levied, and this tax report can be filed.

– E-Z Computation tax form and Long-form: The form can be selected based on the annual turnover limits set by the state.File a public information report.

It is a form every corporation is required to file with the state.

File additional forms if they apply to you.

Prepare and file franchise tax payment reports with the state.

This tax is to be paid annually.

If there is any delay or failure to pay it, the state can levy penalties or legal conditions on the entity.

Franchise Tax Vs Income Tax

Companies may be subject to income tax or corporate tax. While income tax is being levied on profits earned by the company while franchise tax payment does not apply on profits. Instead, the corporation is taxed for the privilege they enjoy operating in the state.

Income tax is levied as per flat rates for the corporation on their profits. On the other hand, it can either be based on profit margin or share capital.

A corporation will pay income tax only when it has profits and not in case of losses. But it may also be payable in the absence of the profits as the same can be levied on share capital basis also.

Recommended Articles

This article has been a guide to what is Franchise Tax. We explain how to pay it, how it is calculated, differences with Income Tax along with examples.. You can learn more about finance from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.