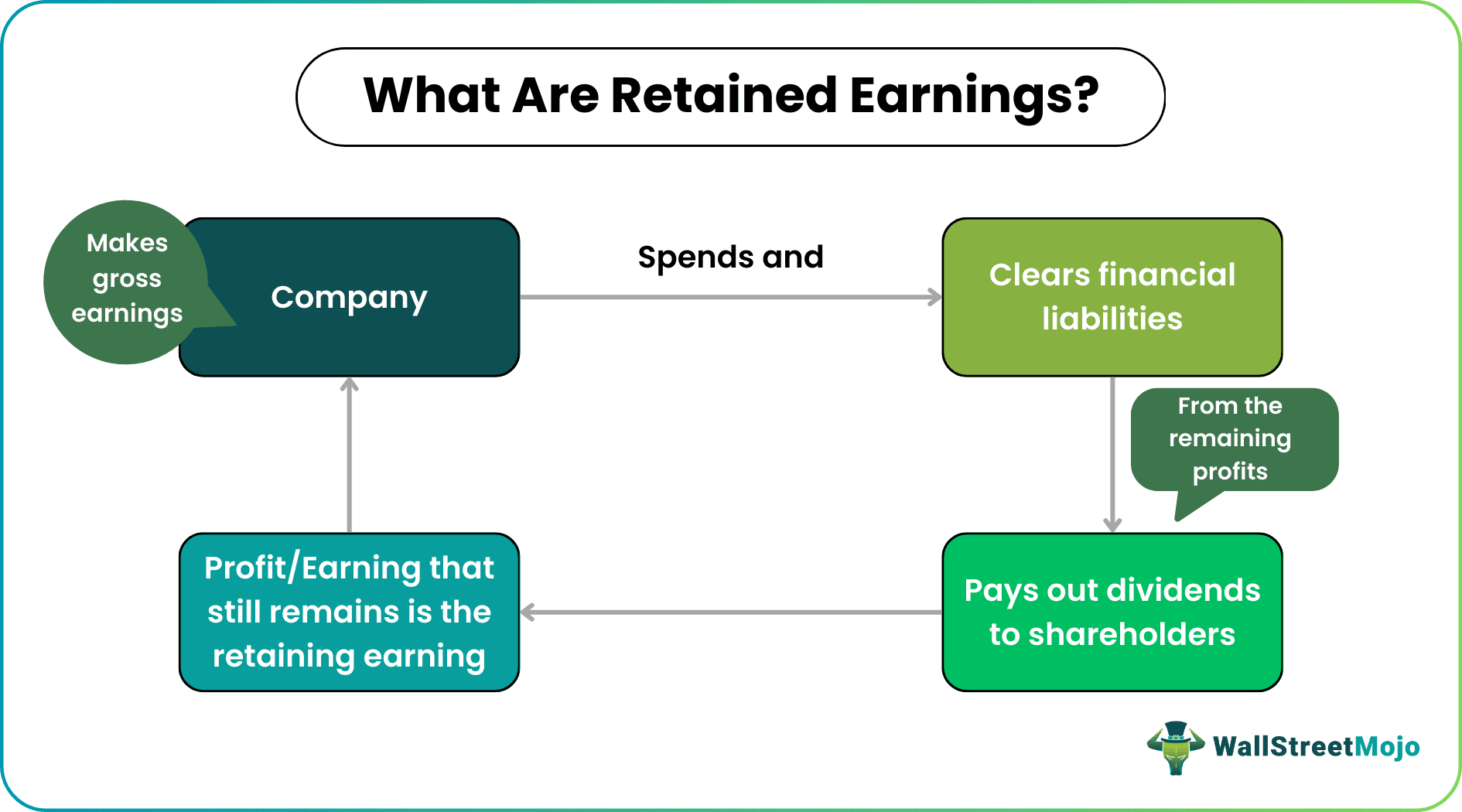

What Are Retained Earnings?

Retained earnings refer to a company’s net profit after paying out dividends to shareholders. This amount gives companies clarity on how much money their business has after paying off all their dues, including the share of the investors.

When recording details in the retained earnings statements, the values change as and when there is a change in the revenue and expense accounts. The value decreases in case companies incur losses and pay dividends, while it increases when the company records new profits.

- Retained earnings are defined as cumulative profits earned by the company after distributing the dividend or other required portions to its investors.

- These can be used for reinvestment purposes.

- Positive net income doesn’t necessarily result in positive retained earnings. The latter can be negative even if the former is positive or vice-versa.

- Retained income at the beginning of a year, net income, and dividends are three components that help calculate retained profits.

Retained Earnings Explained

Retained earnings, as the name suggests, are the sum that a company retains after meeting all its financial liabilities, including the payment of the shareholders. This retained income is the amount companies use for reinvestment, which means utilizing the money back into the business. These earnings form a part of the shareholders’ equity section of the balance sheet.

As the firms pay a dividend to the shareholders despite losses, the retained sum decreases. On the other hand, when they earn profits, the retained sum increases. Its value keeps changing depending on the increase and decrease in the revenue and expense figures.

Components

The meaning of retained earnings is clearer when the components that help calculate the same are thoroughly studied. The elements that help derive the retained income figures are – retained income in the beginning, net profit or loss, i.e., the net income, and applicable share of dividends.

- Beginning retained earnings is any accumulated surplus recorded at the beginning of a financial year. The amount depends on the companies’ profits, losses, or any surplus given to shareholders in the form of a dividend.

- Net income is a company’s total earnings in a financial year. It is the difference between the company’s expenses and revenue. If the revenue is more than all the expenses, the company earns a net profit; else, it’s a loss for that particular year. Net income is the company’s bottom line in its income statement.

- The dividend is a portion of earnings that a company distributes to the shareholders. It is the return or reward for their investment in the company. The dividend can be in the form of cash payments or stock payments, also called bonus issues.

Retained Earnings in Video

Equation

Companies calculate retained earnings at the end of a financial year by adding the net income to the company’s retained profits as recorded at the beginning of that year and subtracting the dividend from the resultant.

The equation used for retained earnings calculation is:

Retained Earnings = Retained Earnings in the beginning + Net Income – Dividend

Where,

- Net income is the difference between the total expenses and the total revenue. The expenses include material costs, general and administrative expenses, salaries of employees, depreciation, amortization, interest payable on debt, and taxes.

- A dividend can be the value of the stocks, the cash value, or the sum of both values.

How To Calculate?

Suppose the beginning retained income of the company is $150,000, and the profit earned is worth $10,000 (Net Income). Plus, the company board decides to pay $1,500 as a dividend to shareholders.

Now, the retained profits calculation at the end of the financial year will be as follows:

Retained Earnings = Retained Earnings in the beginning + Net Income – Dividend

=$(150,000+10,000-1,500)=$158,500

Thus, the retained income for the company that it can use back into the business is $158,500.

Examples

Let us understand how retained income statement is useful for an organization and what it indicated about the financial health of the organization through a couple of examples.

Example #1

Let us check the balance sheet of Colgate, displaying the retained earnings of 2015-16, and learn to locate it on the balance sheet.

Beginning RE (2015) = $18,861 million

The net income of Colgate in 2016 was $2,441 million.

Dividends paid are $1,380 million.

Ending Retained Earnings = 18,861 + 2441 – 1380 = $19,922 million

Thus, the final retained income is as follows:

Example #2

Let us summarize the above example and prepare the Statement of Retained Earnings for the Company ABC Inc. The beginning retained earnings of the Company ABC Inc. is $500,000, the company had a net income of $100,000 and paid a dividend of $50,000 to the shareholders.

The Statement at the end of the financial year is as below:

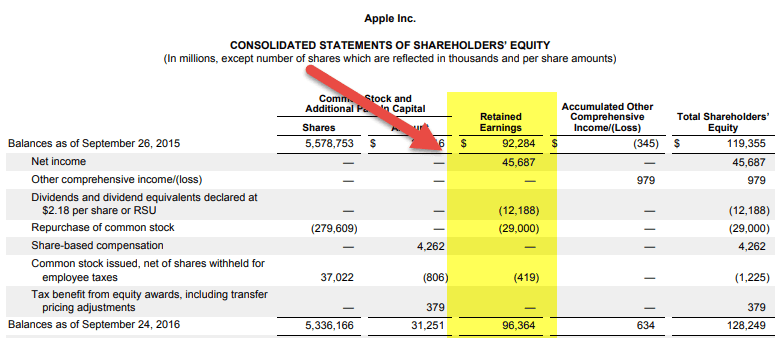

The below snapshot shows the Consolidated shareholder’s equity statement for Apple Inc. for the year ended 2018.

All figures below are in thousands.

- Apple’s Retained Earning in FY2015 = $92,284

- Net Income in FY 2016 = $45,687

- Dividends in FY 2016 = $12,188

- Buyback of common stock = $29,000

- Common stock issues (net of shares) = $419

Apple’s Retained Earnings in FY2016 = $92,284 + $45,687 – $12,188 – $29,000 -$419 = $96,364

Relevance And Uses

The retained earnings statement is very helpful to investors. Investors who have invested in a Company gain either from dividend payments or the share price increase. A mature firm is expected to pay a regular dividend. In contrast, a growing Company is expected to retain the income and invest in future business, thus expecting an increase in the share price.

Hence, it helps investors in both ways:

- It shows dividend payments to the investors or helps them predict future dividends based on the earnings.

- From retained earnings, the investors can analyze how much money is reinvested in the business, which may lead to a future increase in the share price.

Also, it can be used by investors to compare companies in similar kinds of business. However, it is not always prudent to compare two Companies only based on the retained earnings as retained earnings depend on various factors like the company’s age, dividend policy, and the business’s nature, thus affecting the dividend policy of the Company, and the nature of the business, thus affecting the profitability of the company.

Advantages And Disadvantages

While calculating the retained profits offers the owners clarity on the finances they currently have to reinvest in the business; there are a few cons that one must also be aware of:

| Pros | Cons |

|---|---|

| A permanent source of finance that stays with the company | No assurance of the returns on investment. |

| Offers huge flexibility for use as it is the firm’s internal money | Chances of tax evasion |

| This leads to an increase in the share value of the company | Investors are less impressed as the dividend is limited, given the company’s retention of its own profits |

| Businesses can use the money back into the business |

Retained Earnings vs Net Income

The two terms are synonymously used, but they are completely different. So, let us have a look at the differences between the two:

- Net income is the difference between a firm’s total revenue and expenses. At the same time, retained earnings are the sum the company has after it deducts the dividend liabilities and commitments from the net income.

- Therefore, net income becomes a significant component while making retained earnings calculations.

- Even if a net income is positive, it doesn’t signify a positive retained profits sum. There are times when the latter is negative, even when the former is positive, causing accumulated deficits for the firm.

Frequently Asked Questions (FAQs)

Are retained earnings a debit or a credit?

These earnings take the credit side. This is because it forms a part of the shareholders’ equity section of the balance sheet. However, if the value of these profits is negative, they are considered a debit balance. In short, the increasing retained sum is a credit entry.

Are retained earnings an asset?

These are not an asset themselves. However, the finances retained after the dividend payment can be used to buy assets or resources as part of business investment. For example, the funds can help buy the business’s inventory, equipment, etc.

Can retained earnings be negative?

Yes, these can be negative. When the value is negative, it signifies the poor financial health of the firm. This happens when the company incurs significant losses in the previous year. It is often assumed that the retained profits are negative only if the net income is negative. But there are instances where the net income is positive, but the retained income is still negative.

Recommended Articles

This has been a guide to what are Retained Earnings. We explain the concept along with the equation, how to calculate examples, pros & cons, and vs net income. We explain the components, equation, practical examples, and pros & cons. You may learn more from the following articles –