Part of our Shareholder Equity guide

Statement Of Owner’s Equity Definition

A statement of Owner’s Equity is a financial statement containing the change in the shareholder’s capital (reflecting additions and subtractions of equity due to business transactions) over time. When the company gains, it increases the owner’s equity; when the company makes losses, it eats away the owner’s equity.

Statement of Owners Equity Excel Template

Download Excel Template

It is an essential component of a financial statement that provides information like opening and closing balance of equity, dividends, additional investments, etc., to the management, owners, and other stakeholders for financial decision-making. It helps in understanding the sources and uses of equity and evaluating the company’s financial health.

Statement Of Owner’s Equity Explained

The statement of owner’s equity is a financial statement which gives details about the increase or decrease in the equity of the owner or the shareholder over a certain period of time through various events or transactions during that timeframe. It is an important part of financial statement preparation and reporting.

The statement of owner’s equity reports will include various items like beginning equity, net profit or loss, dividend distribution, additional investments made by the management, any income earned form foreign currency translation adjustments or changes in investment value, which are recorded as other comprehensive income and the ending equity balance.

To summarise the examples mentioned above, we can categorize the effects on the Statement of Owner’s Equity into business transactions. Income always has an incremental effect on the owner’s capital. Similarly, expenses always hurt the owner’s equity. Since net profit is the difference between income and expenses, the net income should increase the equity.

But if expenses exceed income leading to a net loss will decrease the capital account. Also, any withdrawals lead to a decrease in owner’s equity. Of course, all the examples shown above have some unique situational transactions like income without any losses, dividend distribution, or withdrawals in the case of a proprietary company, but the underlying effect is what matters.

It is to be noted that this statement gives the owners, management, creditors, investors and other stakeholders an overview about how the equity position of the business has changed over time. It also gives an idea about the sources and uses of equity fund.

Formula

The calculation is as follows:

Opening balance of owner’ s equity

+ Income earned during the period

– Losses incurred during the period

+ Owner contributions during the period

– Owner draws during the period

= Ending capital balance

A typical Statement of Owner’s Equity Example starts with the company’s name at the top, followed by the statement’s heading and the date for which the statement is being prepared. Now let’s reflect on some examples from the point of view of shear calculation.

How To Prepare?

Creating the statement of owner’s equity reports involves making a summarized document of any increase or decrease in shareholder’s equity in the business. Therefore it involves certain steps as follows:

- Gather information – This involves gathering the information and financial data regarding the opening and closing balances of equity, profit or loss made during the period which is given in the income statement, any additional investment, dividend and other comprehensive income, etc. This information collected should be authentic and detailed.

- Change calculation – Here the change is calculated during the reporting period. As per the calculation, along with the beginning owner’s equity, we add the net income, additional investment and other comprehensive income. We deduct the dividend from the same to get the ending balance of owner’s equity.

- Statement creation – The entire calculation has to be represented in a particular format which will show the addition and deduction made in a step-by-step way for easy understanding and use. This will provide a detailed and clear picture of the changes, ensuring that the true information is conveyed to stakeholders and management. The statement should also include details like company name, reporting period, and each section should be clearly described.

- Review – The next important step is to ensure that all information presented in the document is accurate and authentic which should be easy to interpret. The statement should be reviewed for any discrepancies and calculations to be confirmed to present the opening and closing balance correctly for financial recording purposes.

- Publish – The final step is to publish the document for information of stakeholders, management etc for financial decision making. In this way it will become a part of the financial statement and report.

However, the terms and descriptions used in the statement may vary depending on the company rules and regulations followed in the jurisdiction where the entity is operating.

Examples

Let us understand the concept with the help of some suitable examples.

Example 1

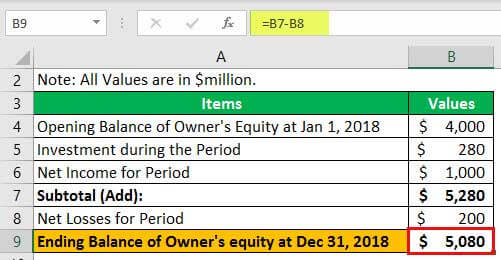

Let’s assume a company Alpha Inc. with an opening balance of owner’s equity of $4,000 million as of January 1, 2018. Now the company raises money from equity investors worth $2,800 million. Also, the company generated a net income of $1,000 million during the year. Similarly, some losses from non-operating activities were worth $200 million. The company’s Statement of Owner’s Equity should look as follows at the end of December 31, 2018:

The company appears to have reached some maturity level in its growth as investors do not seem to infuse more capital into the firm, though the earnings still look pretty good. However, the business might be losing opportunities due to various factors like obsolete product line, lack of customer-oriented focus, etc.

Example 2

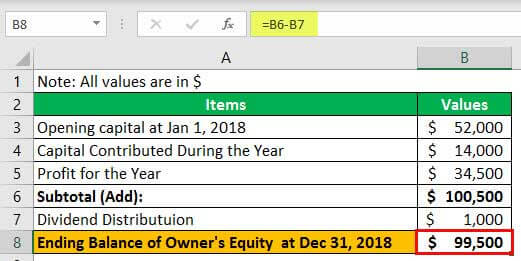

Let’s assume that a company Gamma Tech Corp. has an opening balance of owner’s equity of $52,000 as of January 1, 2018. The company had equity worth $14,00 infused from investors during the year. Also, the company made a profit of $34,500 and distributed $1,000 in the form of dividends. On December 31, 2018, the company’s statement of equity will appear as follows:

Usually, the companies that distribute dividends are perceived to have lesser opportunities to invest the capital, and hence they distribute the capital back to investors in the form of dividends. The Gamma Tech Corp. appears to have made a huge profit this year, but giving dividends back may not appear to be a step in the right direction. On the contrary, investors may perceive it as a mixed signal from the company and hesitate to invest further.

Example 3

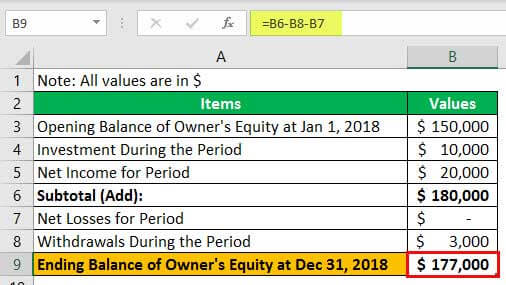

Let’s assume John has a company John Travels Limited. The entity has $150,000 of owner’s equity at the beginning of a reporting period, i.e., January 1, 2018. Now, John makes an investment of $10,000 into his company. Also, during the period, the entity earns an income of $20,000.

Though the company never made any losses since inception John urgently required some money for an unwarranted situation and hence had to withdraw $3000 from the capital account. The sequence of transactions led to the following effect on the owner’s equity:

In this example, the company raised an amount of $10,000 and also earned an income of $20,000. It can be said the company has good prospects and is valued high among investors who agreed to invest $10,000 in the company. The withdrawals are very meager as compared to the overall spike in figures.

Example 4

Beta Limited started in January 2018 with a seed capital of $80,000. The owner made $25,000 additional contributions and $5,000 in total withdrawals during the year. Assuming that the company did not generate any profit or losses during the period, the Statement of Owner’s Equity would look as follows:

A few points to note here are that the capital increased overall from a numerical point of view. But it cannot be said that the business is doing well because no income or losses came into the picture. So from the operations point of view, the business does not have any activity.

The entity only raised an amount of $25,000 from investors and had a withdrawal of $5,000. Hence, though the capital went up, it was not due to the company’s operations; hence, it is very hard to make any opinion about this business.

A few points to note here are that the capital increased overall from the numerical point of view. But it cannot be said that the business is doing well because no income or losses came into the picture. From the operations point of view, the business does not have any activity.

Purpose

This statement is extremely useful from the point of view of stakeholders and management for various purposes. Let us identify the main purpose of the statement.

- Equity changes – It clarifies the changes in equity structure of the company and the reasons behind it for the reporting period. The breakdown of the changes provides important information of the process.

- Show owner contribution – The contribution of the owners of the business is highlighted, which include extra capital injected in later part of the business.

- Comprehensive income – The statement includes income that does not arise from the regular business operations but affect the equity and so they have to be included in the statement. They are important and should be reported.

- Profit distribution – The profit distribution in the form of dividend to shareholders is reported in it. This provides a clear information about the earning distribution.

- Compliance to standards – The statement ensures compliance to reporting and accounting standards as per the rules of the company and jurisdiction.

- Financial record and transparency – The statements provide a clarity about equity related events and transactions. This in extremely valuable for potential investors, shareholders, creditors, etc who depend in the statements to take financial decisions. It also helps in keeping record of how the equity position has changes over time, which can be used as a benchmark for financial analysis.

- Financial condition analysis – Above all, it is important to have a document that will clarify the financial health of the business. This statement gives some valuable insight into it This indicates, the profitability, stability and sustainability of the business.

Thus, the document plays a very vital role in financial reporting because it provides useful information about owner’s contribution, profit distribution and serves as a tool to assess the financial performance of the business.

Statement Of Owner’s Equity Vs Balance Sheet

The above are considered to be important part of the financial statements that are prepared for any particular timeframe to evaluate the financial position. However, there are some differences between them as follows:

- The former is prepared to highlight the changes in equity position of the business over a period of time whereas the latter gives a snapshot of the financial condition at a particular date.

- The former explains transaction or events like additional investments, dividend declared, other comprehensive income, etc, but the latter gives the data about the position of assets and liabilities at a particular point of time.

- The time frame of both statements varies. The former displays financial information over a period of time but the latter displays information related to a particular date.

- In the former, all the income and investmenst are added and dividend is deducted to arrive at the ending balance of the owner’s equity whereas for the latter, the liabilities are deducted from assets to arrive at the fund balance that the business owns at a particular date.

- The former may be prepared on a quarterly or annoual basis whereas the latter is prepared either monthly, quarterly or annually. However, it depends on the company laws and rules of the jurisdiction.

Thus, the above are some important differences between the two statements, which are integral part of financial reporting.

Recommended Articles

This article has guide to Statement Of Owner’s Equity and its definition. We explain with examples, formula, how to prepare & purpose. You can learn more about Accounting from the following articles –

- Examples of Equity

- Examples of Owners Equity

- Book Value of Equity Formula

- Formula of Owner Equity

- Shares Purchase Agreement

Recommended Articles

Continue with these closely related articles from the same guide.