Part of our Accounting Concepts guide

Meaning of Going Concern

The Going Concern is an assumption made in financial statements that a company will not go bankrupt in the foreseeable future—usually referring to a period of 12 months. It is a fundamental accounting principle.

In other words, a gong concern will continue to exist in the long run, with no intention to shut down. There is no immediate uncertainty. When management considers such assumptions inappropriate, financial statements are prepared based on a break up basis.

- A going concern is an accounting assumption that a business will continue its operations for the foreseeable future. It is reflected in the financial statements of the company.

- The continuity of a business is determined by positive solvency position and enterprise values.

- According to Generally Accepted Accounting Standards (GAAS), the going concern assumption is a crucial parameter for ascertaining business longevity.

- Alarming signs that question the continuity of a business include low liquidity, decreasing market share, poor credibility, lawsuits, business losses, employee turnover, and outdated product itinerary.

Going Concern Explained

The going concern assumption is a fundamental accounting concept, similar to Consistency Principle and accrual assumption. According to this principle, financial statements are prepared, assuming the company intends to continue operations for the foreseeable future and has no motive or need to shut down.

On the other hand, if a company intends to close operations, financial statements will reflect such an intent—the company must disclose it. Unless disclosed, it is assumed by default that the company will realize its assets and settle its liabilities.

Although the going concern assumption holds no place in the Generally Accepted Accounting Principles (GAAP), it is recognized by Generally Accepted Accounting Standards (GAAS). GAAS considers this principle a crucial parameter for determining the longevity of a business.

So, when managements consider such an assumption inappropriate, they prepare financial statements using the breakup basis. The breakup basis reports assets based on the amount that is likely to be realized from the sale and liabilities—the net realizable value. For example, seasonal businesses like firecracker companies opt for the breakup basis.

Going Concern Concept in Video

Going Concern Example

Let us understand the application of this principle using examples.

Example #1

AB Ltd. is a construction company that incurred a loss of $700,000 in a housing project— due to government stay and legal action. As a result, the company missed five installments of debt worth $60,000 (total non-repayment in 5 years).

The company lost its creditworthiness in the debt market; it was on the verge of insolvency—bankrupt within 1.5 years. Before this situation, it was considered a going concern by the auditors and accountants.

Example #2

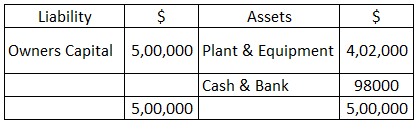

Let us assume Douglas purchased a manufacturing plant & equipment for his business by paying $400,000 out of the $500,000 investment. He also paid installation expenses, amounting to $2,000. If he is still willing to continue his business, his financial position will be as follows:

If Douglas decides to sell the manufacturing plant and equipment, he might get more or less than $402,000, which will change his financial position.

However, when we consider the concept of going concern, such a change in asset value will be ignored in the short run. The principle highlights the assumption that companies intend to keep assets and generate profits in the future—assets won’t be sold in between.

Therefore, the change in value is not realizable; Douglas and his company must not consider the going concern assumption. They must opt for the breakup basis.

Importance

The going concern assumption is crucial for the companies due to the following reasons:

- Primarily, it presumes that the firm will remain functional for an infinite period and has no liquidation plans.

- Also, it represents the financial stability of the organization and its efficiency in meeting long-term liabilities.

- It increases the creditors’ trust in the business entity—helps the firm, secure finance, overdraft facility, and credit.

- Moreover, it is necessary for ascertaining the depreciation of fixed assets.

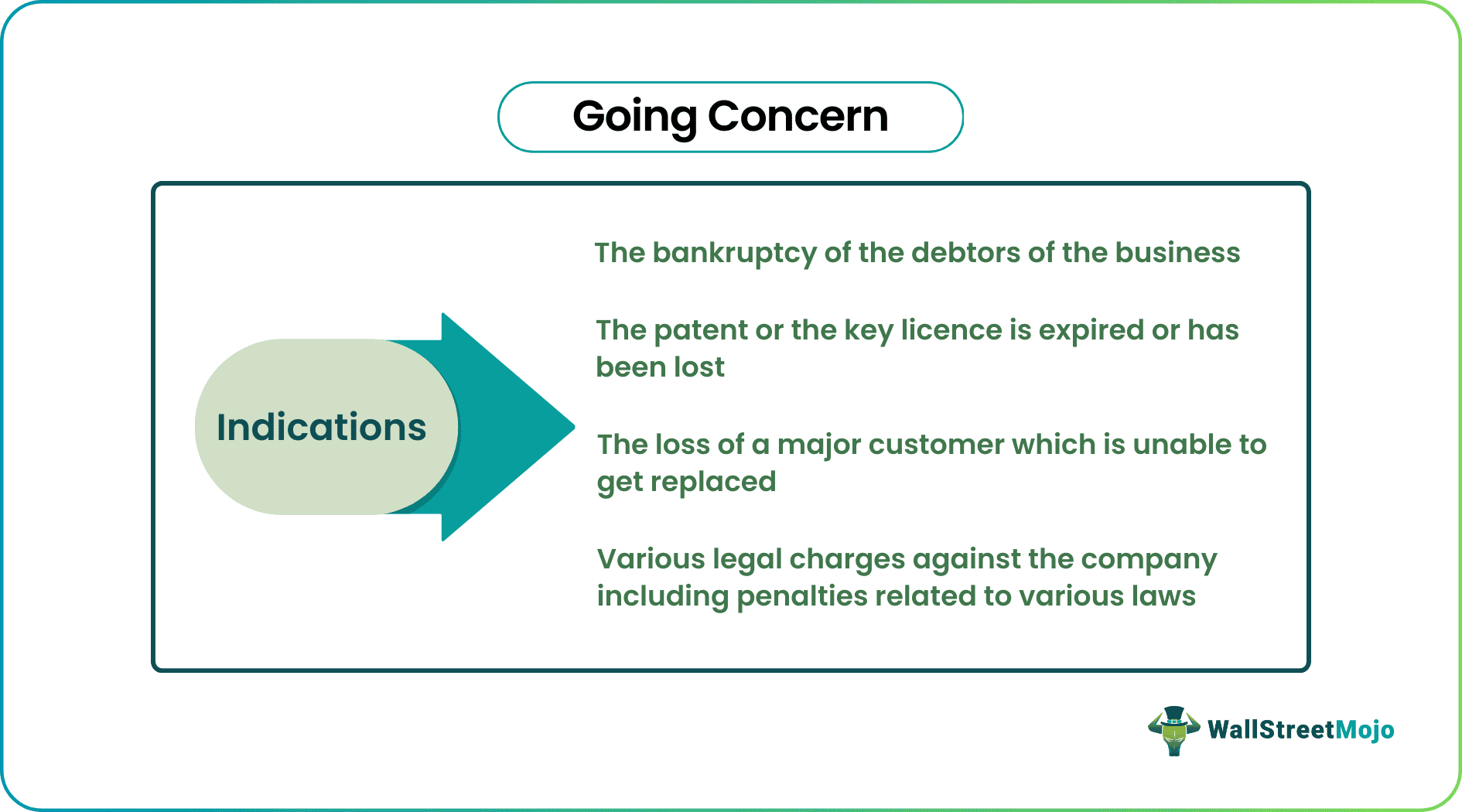

Indicators of Going Concern Problems

The following red flags indicate that a company is unable to continue as a going concern:

- Negative Trends: Decrease in sales, financial ratios, increase in costs, and recurring losses signal that the firm may not be solvent in the future.

- Employee Turnover: Loss of key managerial personnel, skilled staff, labor hardships, or strikes are red flags.

- Poor Liquidity Ratios: Declining liquidity and insufficient financing alternatives hint toward a possible bankruptcy.

- Legal and Regulatory Matters: Legal charges against the company or penalties for breach of law is a serious red flag.

- Recurring Trading Loss: Businesses risk insolvency when long-term debtors announce bankruptcy.

- Loss of Patent: Losing a license or patent raises serious concerns for investors and shareholders.

- Non-Repayment of Loan: Loan defaults are a common risk associated with any business. It is a vicious cycle; firms that desperately need financing end up with the worst credit ratings—they are unable to sanction further financing.

Frequently Asked Questions (FAQs)

What is a Going Concern?

It is an accounting assumption that defines the longevity of a business operation. By default, financial statements reflect this assumption. Unless the company discloses, it is assumed that it possesses adequate assets for fulfilling long-term liabilities.

What does it mean when a property is sold as a going concern?

It refers to properties sold for income-generating activities—on the registration date. Also, both property sellers and buyers must have VAT registration—registered as vendors. On such a transaction, the VAT charged is 0%. Also, the transaction should involve all the related assets that facilitate income generation.

What are some going concern red flags?

Warning signs include falling market share, poor creditworthiness, employee turnover, low liquidity, lawsuits, excessive business loss, and inability to innovate.

Recommended Articles

This article has been a guide to Going Concern Assumption and its meaning. Here we discuss Going Concern definition, accounting principles, audits, basis, values, and examples. You can learn more about it from the following articles –