Meaning Of Net Realizable Value (NRV)

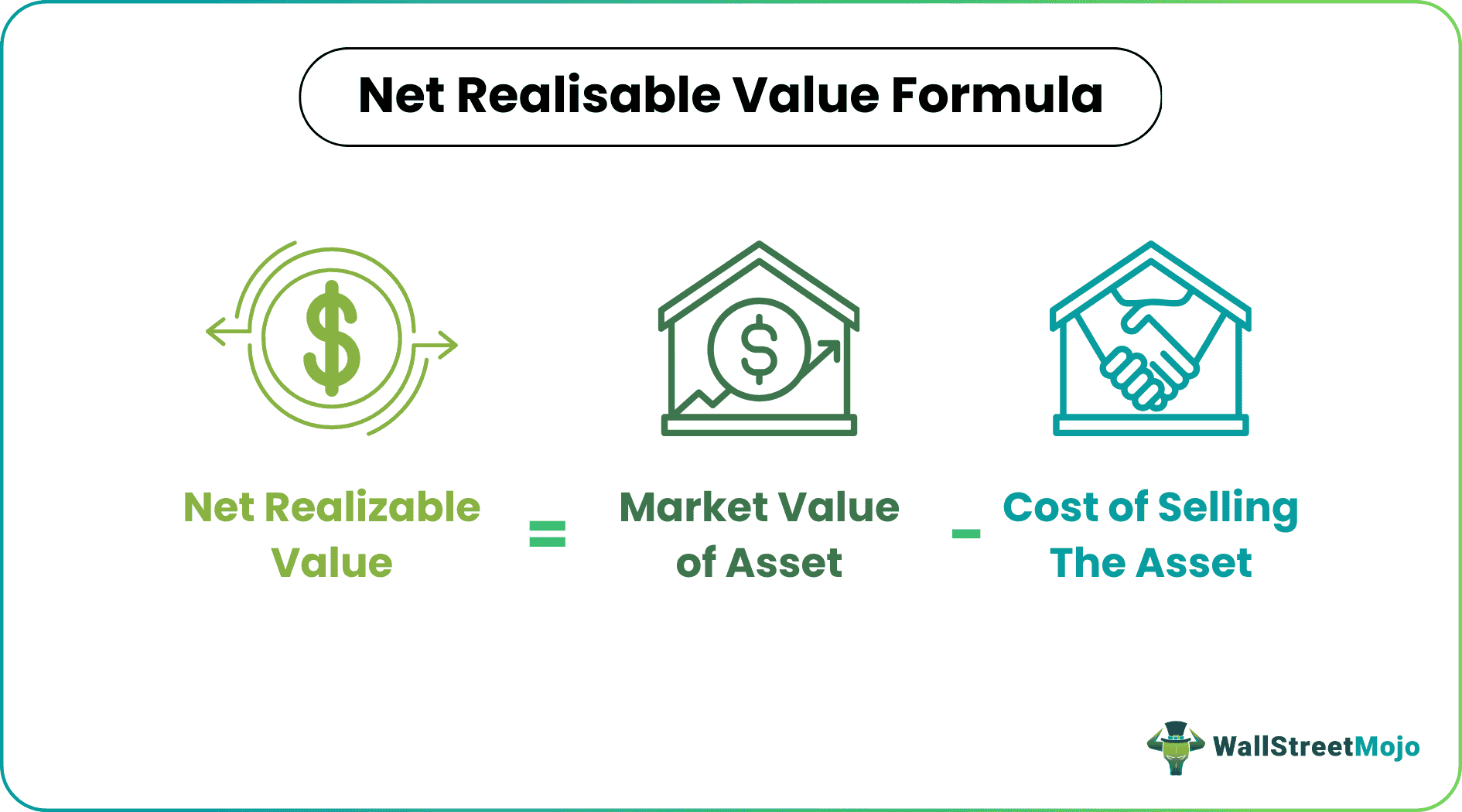

Net Realizable Value is the value at which the asset can be sold in the market by the company after subtracting the estimated cost which the company could incur for selling the said asset in the market. It is one of the essential measures for the valuation of the ending inventory or receivables of the company.

Thus, it estimates an asset’s price on disposal less the sale cost. It is a substitute for the asset’s market value if it is unavailable. It is accepted in both the accounting standards, GAAP and IFRS to ensure the ending inventory value is neither overestimated nor underestimated.

- After deducting the expected cost that the firm would incur for selling the specified asset in the market, the asset’s net realizable value is the price at which it can be sold in the market by the company.

- Since NRV is a conservative method, the accountant should record transactions that do not inflate asset values and may result in lower profits from asset valuation. Since it entails a lot of judgment, certified public accountants (CPAs) are typically needed to do the task.

- NRV is the sum that is anticipated to be converted into cash. The NRV, which can also be stated as a debit balance in the asset account, is obtained by subtracting account receivables from the credit amount.

- The conservative accounting concept can be followed while reporting assets on the balance sheet, making this strategy particularly helpful for accountants.

Net Realizable Value Explained

Net realizable value method is the value of an asset, excluding a reasonable estimate of costs associated with the disposal of the asset or the eventual sale, which is realized or derived upon the sale of that asset. It is commonly used in the context of calculating the net realizable value of accounts receivable. This method is very useful for an accountant as it allows them to follow the conservatism principle of accounting while reporting assets on the balance sheet.

It is a conservative method, which means that the accountant should post the transaction that does not overstate the value of assets and potentially generates less profit for valuing assets. It usually requires certified public accountants (CPAs) to do the job as it involves a lot of judgment.

In the context of net realizable value inventory, it is also important to understand that the companies using retail or the last in first out accounting would probably not use the net realized value or the lower of cost method, but would rather NRV inventory at lower of cost or market.

It is worth noting that the adjustments can be made for each item in inventory or for the aggregate of the entire net realizable value inventory to the lower cost or NRV. Once curtailed down, the inventory account becomes the new basis for reporting purposes and valuation.

US GAAP does not permit a write-up of write-downs reported in a prior year, unlike international reporting standards, even if the net realizable value for inventory has been recovered.

NRV Video Explanation

How To Calculate?

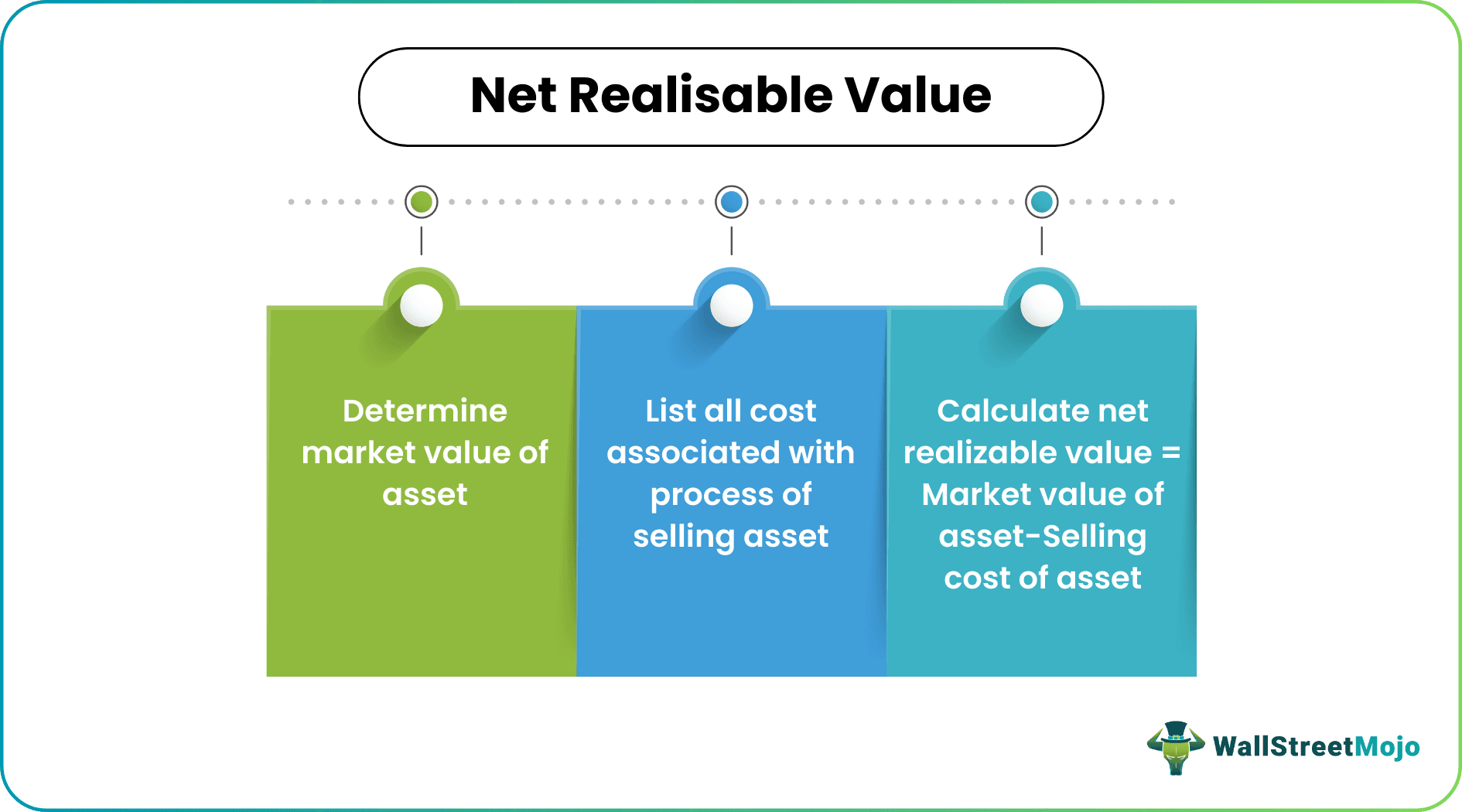

Let us see how to implement the net realizable value rule.

Determine the Market Value of the Asset

List all the cost associated with selling the Asset (including transportation, insurance, production, testing, tax, etc.)

Calculate NRV = Market Value of Asset – Selling Cost of the Asset

Example

Let us take some examples to understand the Net realizable value rule.

Example #1

A company XYZ Inc. is trying to get rid of some of its outdated phones, and it expects to sell them for $5,000 to a local buyer, but it must pay $240 to have them shipped and insured and another $40 to complete the paperwork.

So the telephones’ NRV can be calculated as $5,000 – $240 -$40, which is equal to $4,720.

Example #2

Year 1

Company ABC has an inventory i2 that costs $70. The market value of this inventory i2 is $200, and the preparation cost to sell this inventory i2 is $30.

NRV = $200 – $70 – $30 = $100.

Since the cost of the inventory i2 is $70 is lower than NRV of $100, we value the inventory on the balance sheet at $70

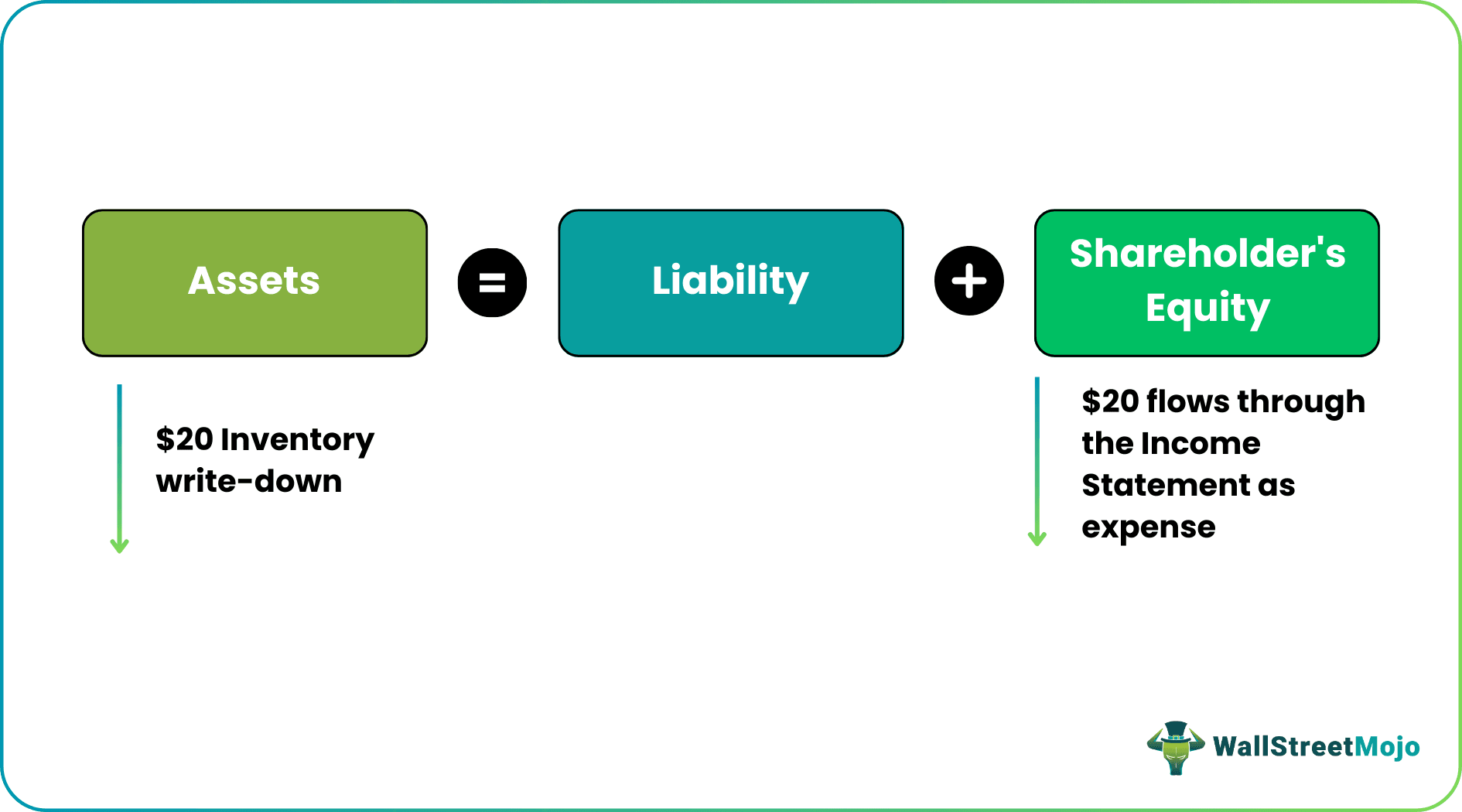

Year 2

The market value of the inventory i2 declines to $150. However, inventory i2 and the preparation cost to sell this inventory i2 remain the same at $70 and $30, respectively.

NRV = $150 – $70 – $30 = $50.

Since the cost of the inventory i2 is $70 is higher than the NRV of $50, we get the net realizable value for inventory on the balance sheet at $50.

Inventory Write-Down = $70 – $50 = $20

Example #3

NRV is the amount that is expected to turn into cash. Net realizable value of accounts receivable minus the credit balance give you the NRV, which can also be expressed as a debit balance in the asset account.

For instance, if the debit balances in the account receivables are $10,000 and have a credit balance of $800, then $9,200 is the resulting value of accounts receivables in the net realizable value method.

Net Realizable Value Vs Fair Value

Net realizable value is the amount realized after selling an asset and fair value is the current selling price of the asset. Let us look at the differences between them.

| Net Realizable Value | Fair Value |

|---|---|

| It is the sale price of asset minus the cost incurred for sale. | It is the current selling price of the asset. |

| It is always possible to estimate this value. | It is not always possible to acquire the market value. |

| It is more associated with the value of receivables and inventory. | It is associated more with the price estimate made by sellers and buyers. |

| It is company specific. | It is not company specific. |

Frequently Asked Questions (FAQs)

What else could you call net realisable value?

Consequently, net realizable value is also known as cash realisable value. The terms “net realizable value” and “current assets” are frequently used concerning inventory and accounts receivable.

What happens if NRV is less than cost?

According to the notion of lesser cost or net realizable value, inventory should be recorded at the lower of its cost or the price at which it can be sold. The estimated selling price of something in the regular course of business, less the completion, selling, and shipping costs, is known as the net realizable value.

Can NRV be adverse?

A positive NRV implies that your inventory will generate profits for you, whereas a negative NRV shows that the value of your goods is lower than their cost.

Recommended Articles

This has been a guide to Net Realizable Value and its meaning. We explain how to calculate it along with examples and its differences with fair value. You may learn more about accounting basics from the following articles –