Part of our Accounting Concepts guide

What Is Prudence Concept In Accounting?

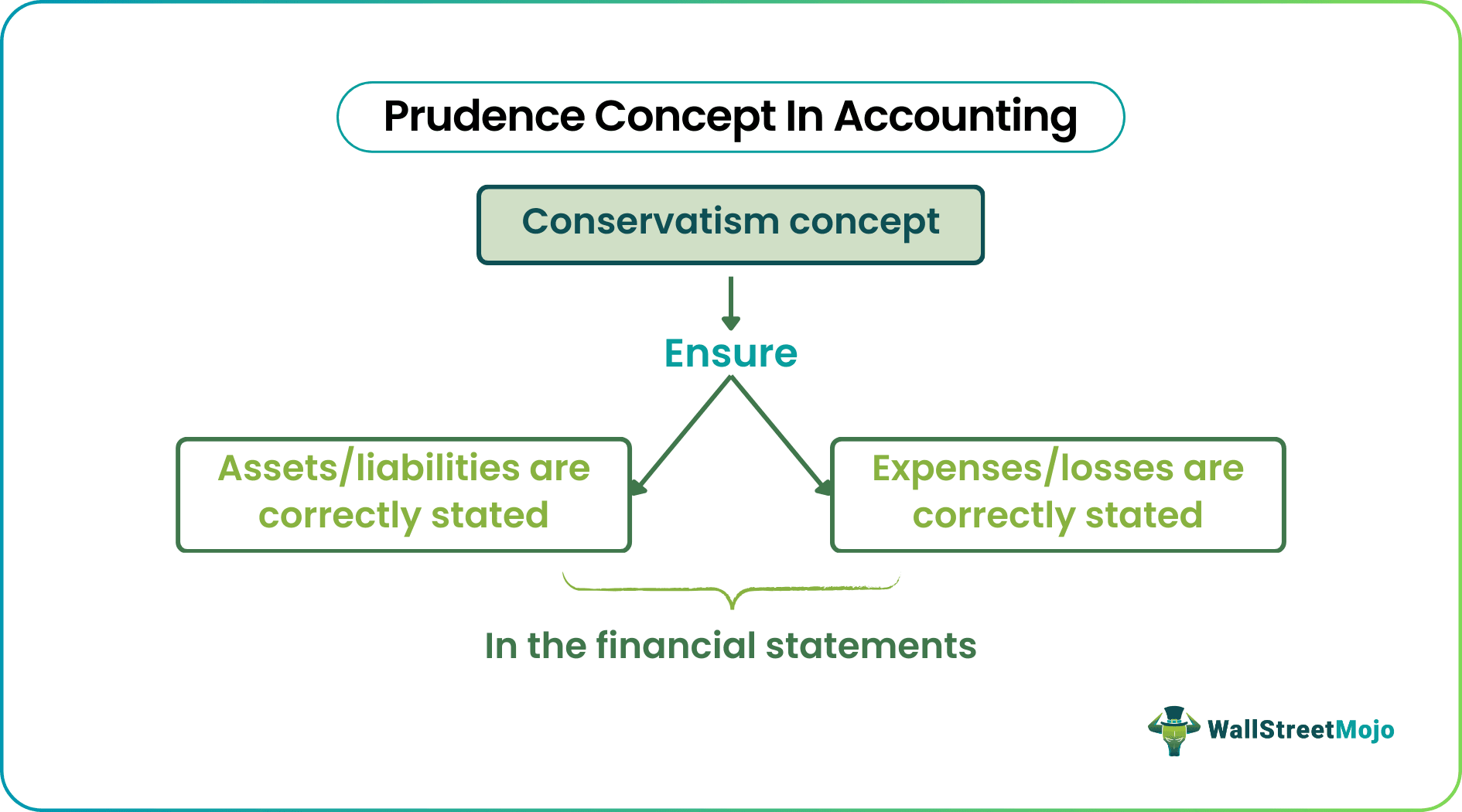

Prudence Concept or Conservatism principle is a key accounting principle that makes sure that assets and income are not overstated, and provision is made for all known expenses and losses whether the amount is known for certain or just an estimation, i.e., expenses and liabilities are not understated in the books of accounting.

By applying this concept there is less change of companies to overstate their own financial health. It helps the stakeholders take an informed financial decision and predict the future prospects of the business. However, businesses should not use it to hide any kind of information or distort it in the process.

Prudence Concept In Accounting Explained

Prudence concept has been put in place to ensure that the person who is making the financial statements makes sure that the assets and income are not overstated to make sure the company is not overvalued. The expenses are not understated to ensure that the company is not rightly valued.

The prudence principle in accounting is often described using the phrase “Do not anticipate profits, but provide for all possible losses.”

In other words, it considers all prospective losses but not the prospective profits. The application of the prudence concept ensures that the financial statements present a realistic picture of the state of affairs of the enterprise and do not paint a better picture than what is.

Recognizing Revenues

- The prudence concept principle says that whenever you have a situation where you have some future income, you should not recognize or include that in your books of accounts.

- So, when I prepare my financial statements, my books of accounts or my balance sheet, or profit or loss account, I will not recognize the prospective income as part of my income for the current year’s financial records because I am acting on a conservative basis.

- This principle is not to overstate your income unless and until you have possession of that income.

- As per the prudence concept in accounting, we cannot overstate income. We cannot take into account the future income which may arise.

Recognized Expenses

- At the same time, the concept of prudence principle in accounting says that you should never underestimate expenses. If there is an expectation that some expenses are likely to be incurred, you should provide it in your books of accounts.

- It would be best to make a provision today in your book of accounts for the above-mentioned future claims. In the future, you have to make the payment, and effectively this claim is in respect of whatever income you have made to date, i.e., till the date you are preparing your balance sheet (in this case, till 31.03.2018).

- In this case, the prudence concept in accounting says that you should never underestimate the expenses, and if there is a likelihood of expenses, we call it a provision. We should make a provision for expenses in your book of accounts.

Examples

Let us understand the concept with the help of some suitable examples.

- Let us assume that you have prepared your company’s financial statements for 31.12.2018. So as the balance sheet date, which is 31.12.2018, you get additional information stating that the company may earn $1 million from a particular contract. As you are closing your financial statements, you know in advance that some income possibility would be there shortly. At the same time, let’s assume that there is also a possibility that some claim may come, which may result in an expense of, say, $500,000.

- There is a “provision for bad and doubtful debts,” which is reported in the receivables section of current assets and is deducted from the final figure of debtors/receivables. This provision doesn’t show the debtors that have resulted a bad debts; instead, it shows the debtors that may end up as bad debts based on their trading history with the company or their specific circumstances. Ultimately, the company may not recover money from these debtors. These debtors are included in the provision under the prudence concept in accounting.

- In IAS2 (International Accounting Standard for Inventory), the inventory is always valued at lower cost (original cost) or NRV (net realizable value – selling price less cost to sell), so that inventory may not be overvalued, as the figure of inventory directly impacts the “cost of sales” figure, because

“Cost of sales = Opening Stock + Purchases – Closing stock.”

- Many liabilities are not certain either in terms of amount or date, but they have a high possibility of occurrence. In such cases, the liabilities are recorded in the statements, and a corresponding expense is also recorded. So it makes sure that liabilities are not undervalued.

The above examples give us a clear idea about how to account for various items in the financial statement by following the prudence concept in a transparent manner, which is easy to interpret and use.

Importance

Some points of importance of the financial concept are as follows:

- The prudence concept or conservatism principle is well known and used worldwide. This principle gives the companies a base on which companies could build or prepare their financial statements.

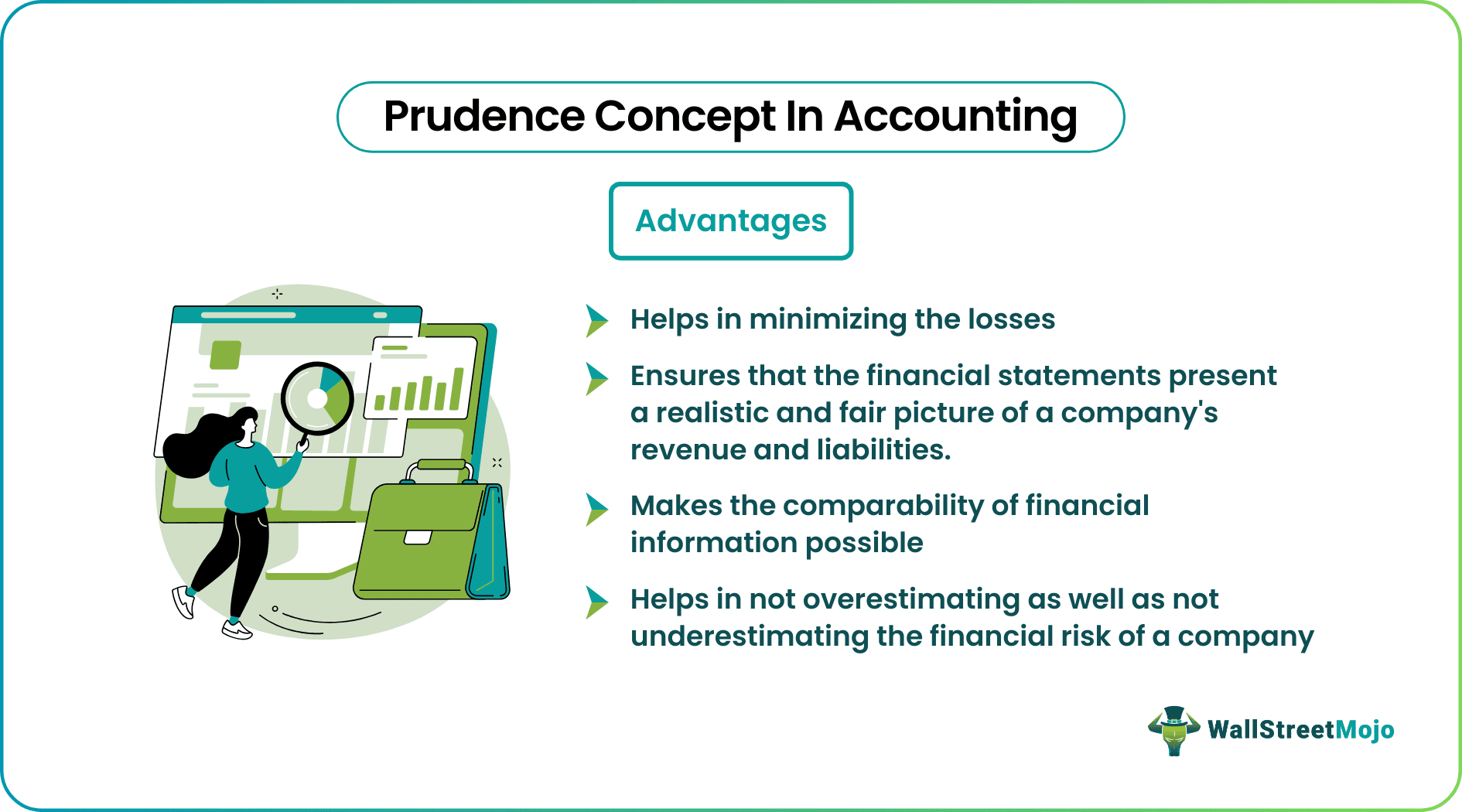

- Prudence principle in accounting ensures that the financial statements present a realistic and fair picture of a company’s revenue and liabilities.

- It helps in the minimization of losses.

- It helps in not overestimating as well as not underestimating the financial risk of a company.

- The Prudence concept makes the comparability of financial information possible.

Disadvantages

The concept also has certain disadvantages, which are as given below:

- The prudence concept in accounting doesn’t always necessarily consist of correct facts.

- You cannot apply the prudence concept to cultures that are outside of the IFRS or the GAAP.

- A company may try to create provisions that are not required, resulting in the creation of some private reserves.

- It lowers the earnings and profits, given the stakeholders the idea that the company is not performing well. This may reduce its value in the market and investors may back away.

- It may impact management decision because they may try to invest in opportunities that look more profitable but is risky. In order to prioritise profits and avoid losses, they may miss good opportunities.

- Since it is not accepted in all accounting standards, there is lack of standardization in financial reporting. Therefore the interpretation and application may vary.

- The concept involves some level of subjectivity which creates possibility of manipulation to meet investor’s expectations.

Thus, it is necessary to understand the advantages and limitation of any financial concept clearly so that they can be applied in the appropriate time and place for maximum value creation.

Recommended Articles

This has been a guide to what is Prudence Concept In Accounting. We explain it with examples, its importance and the various disadvantages of the concept. You may also find some useful accounting articles below –

Recommended Articles

Continue with these closely related articles from the same guide.