Part of our Accounting Concepts guide

What is the Money Measurement Concept in Accounting?

Money Measurement Concept is one of the accounting concepts according to which a company should record only those events or transactions in its financial statement which can be measured in terms of money and where assigning the monetary value to the transactions is not possible. It will not be recorded in the financial statement.

It means that only those transactions and events are recorded in the books, which can be measured in monetary terms. In other words, all those events and transactions that could not be quantified in monetary terms are not recorded in the financial statements of the company.

Examples of transactions that are not recorded in the financial statements are as follows –

- Unfavorable Government Policies

- Skills set of employees and workers

- The working atmosphere and office culture of the organization

- The efficiency of the administrative and backend processes within the company

- Quality of the products and services

- Satisfaction of stakeholders

- Safety Measures within the company to prevent any hazard

Although it is difficult to assess the impact of such events in numbers, they have an indirect effect on the business’s financial performance either by way of assets, liabilities, incomes, or expenses. The following cases would help us understand the events and their impact on the business.

Practical Example of Money Measurement Concept in Accounting

The story of “Maggi”: Immeasurable Nestle India Controversy

The enduring success of any company can be effectively measured in terms of the brand value it creates in the market, but more than that, it is the brand image in the consumer’s eyes that matters the most. The USP of a particular product has to be the impact on environmental, social, and human health criteria. In 2014, a laboratory in Gorakhpur proved that the samples of Maggi contained lead and monosodium glutamate-1 (MSG) much beyond the permissible limit.

Although Nestle India challenged this decision, the results by Kolkata Central Laboratory in 2015 corroborated the previous results. Consequently, several state governments began testing samples and banned the product. Within a few days, Maggi was off the shelves from every grocery store and Kirana shop in the country.

Though Maggi has returned, this incident will always be referred to and remembered as a black spot in the reputation of Nestle India. Though it is indirectly shown in the books of accounts, the top line has been affected by this event. Despite the inevitable event, the money measurement concept doesn’t account for it in the books of accounts.

Apart from that, Nestle had to spend a considerable chunk of money to control the damage to its brand image and get back its customer base. This happening resulted in many brand-building exercises like dedicated social media handles, customer service helplines, and other PR activities, resulting in an increase in expenses and reducing the top line.

Market Sentiments and Stock Prices

It may seem a little off-topic, but by keeping the fundamentals and numbers of the company unchanged, the market sentiment of a particular stock can influence the movement of its stock price.

The sentiments are based on the disruptions in the market climate, i.e., Political, Economic, Social, Technological, Environmental, or Legal (PESTEL) factors related to a particular company, sector, or industry that can move the prices either upwards or downwards depending on the outlook. Unlike inputs such as sales, depreciation, taxation, etc., the events that affect the stock prices aren’t recorded in the company’s financials, but they invariably affect the business. It reflects the downside of the principal, as these intangibles invariably can influence the price and the business. However, still, these are not being taken into the books of accounts actively.

Important Factors

Keeping the above principle in mind, other important factors should be kept in mind while analyzing the financials of the company regardless of the fact, whether it could be accounted for or not: –

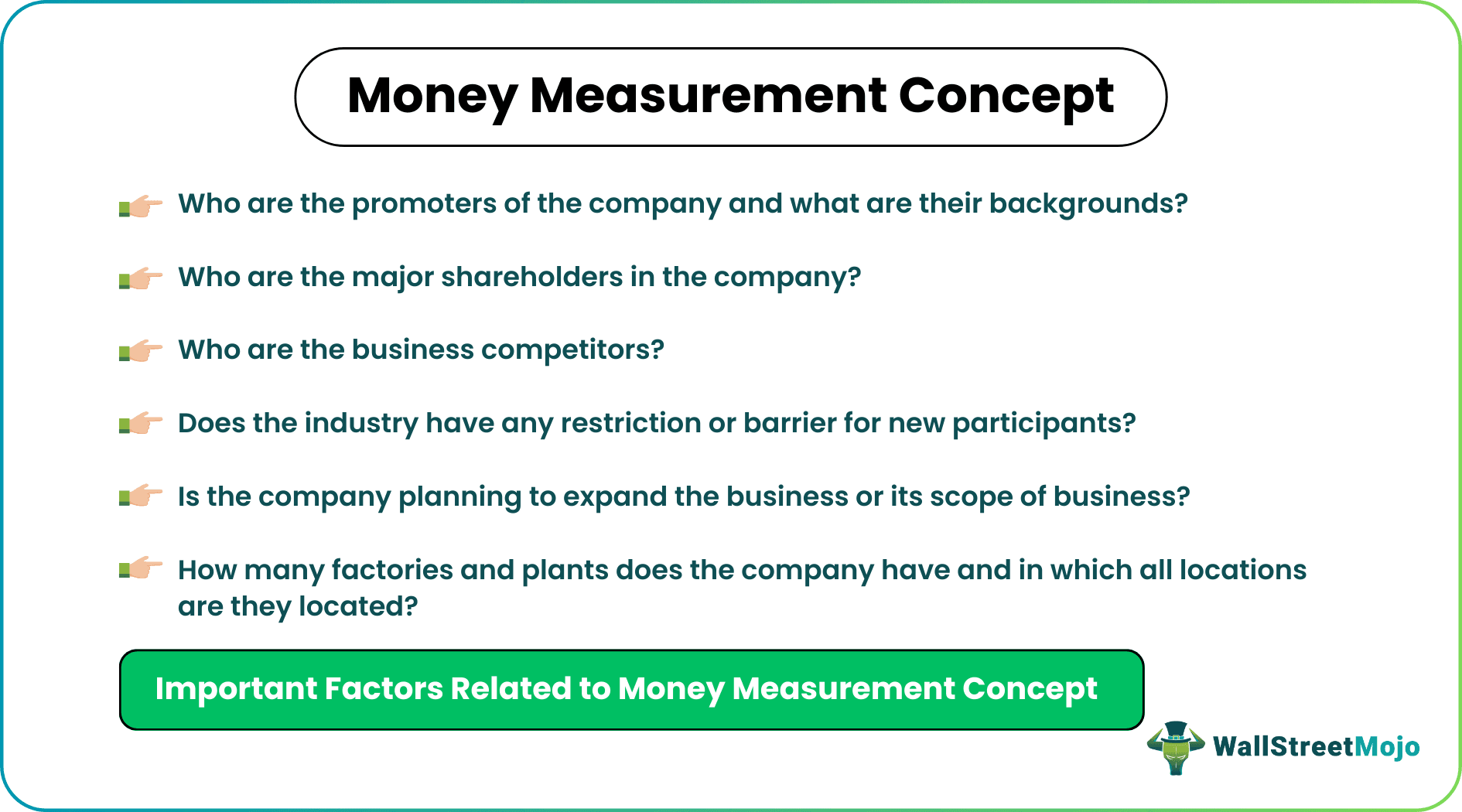

- Who are the promoters of the company, and what are their backgrounds?

This data is vital as the balance sheet doesn’t talk about the people behind the business. Their sanity check is relevant to understand if they have any political affiliations or criminal backgrounds, as these factors do hold weight more than the numbers.

- Who are the majority shareholders in the company?

It is also advisable to understand who owns the company’s shares and its background. It could give us a positive outlook if the shareholders’ names are renowned.

- Who are the business competitors?

It helps to know the competition in the market, as it makes us aware of the profit margins. The structure within which the business operates, whether it is a monopoly, duopoly, or monopolistic market.

- Does the industry have any restrictions or barriers for new participants?

Understanding the barriers helps us know the long-term growth potential available in the market.

- Is the company planning to expand the business or its scope of business?

It will let us know about the Research & Development wing operating in the business. It will also make us aware of how innovation-driven the business is.

- How many factories and plants does the company have, and in which all locations are they located?

It will let us know the company’s geographical presence apart from that at times. The factories may be located at a prime location, which could go off the balance sheet making the company undervalued.

- Working atmosphere or culture of the company

If the working atmosphere or culture of the company is unfavorable, in that scenario, the employee retention would be below, which would result in the additional cost burden for the company to attract and train new employees.

The major problem in the money measurement concept is that many factors can lead to long-term changes in the financial results or financial position. Still, the concept does not allow them to be accounted for in the financial statements. The only exception would be discussing relevant items that management includes in the disclosures that accompany the financial statements. Therefore, it is possible that some vital underlying advantages of a business are not disclosed, which tends to under-represent the long-term ability of a business to generate profits. The other way round is typically not the case since management is encouraged by the accounting standards to disclose all business current or potential liabilities in the notes accompanying the financial statements.

Conclusion

In short, the money measurement concept can lead to the issuance of financial statements that may not adequately represent the future upside of a business or uncertainties. However, if this concept were not in place, managers could deliberately add intangible assets to the financial statements with little or no supportable basis.

Recommended Articles

This article has been a guide to the Money Measurement Concept in Accounting and its definition. Here we learn terms related to this Concept along with practical examples. You may learn more about accounting from the following articles –