Part of our Accounting Concepts guide

What is the Consistency Principle?

The consistency principle states that all accounting treatments should be followed consistently throughout the current and future period unless required by law to change or the change gives a better presentation in accounts. This principle prevents manipulation in accounts and makes financial statements comparable across historical periods.

Explanation

All accounting policies or accounting assumptions are to be followed consistently to compare financial statements easily. Suppose an entity changes its accounting policies or assumptions. In that case, it should be by the reason that law demands the change or change gives better preparation and presentation in accounts and if there is change due to any other reasons that reason to be stated clearly and also an effect of change and nature of the change to be disclosed in the financial statements so that it attracts the attention of users and users can understand the change in profit due to change in accounting estimate or assumptions.

Example of Consistency Principle

- If the business entity follows the straight-line method of depreciation and after some time law changes, every entity must follow the written down value method of depreciation retrospectively. Now, an entity has to provide depreciation as per written down value method retrospectively and accordingly charge the depreciation and effect on profit due to a change in method of depreciation to be disclosed and the fact that method of depreciation has been changed due to change in law also to be disclosed in the financial statement so that users can understand easily.

- Another Example is a Business entity following the LIFO method for valuation of inventory valuation. The law demands the Average weighted method or FIFO method to be used for valuing the inventory. So, an entity has to change the method of valuation of inventory retrospectively and value inventory accordingly and change in valuation and effect of change due to change in method of inventory change on profit to be disclosed appropriately. Disclosure gives better preparation and presentation and also catches users’ attention on change in profit due to change in the method of inventory valuation.

- Another Practical example is as INDAS and IFRS are introduced and applicable to companies, and traditional Accounting standards override the INDAS and IFRS. Financial Statements have to disclose the change in profit due to a change in law and disclose that change is due to a change in the law.

Uses and Importance of Consistency Principle

- All entities need to follow accounting policies and principles consistently. As consistency is one of the fundamental accounting assumptions unless the change in accounting policies is disclosed, it is assumed that all accounting policies followed last year are followed in the current year. Consistency makes the financial statements comparable, and it also gives ease in the preparation of accounts. It is used in all industries, whether manufacturing, trading, or service industry.

- It is important in every industry as it makes sure that accounting policies and assumptions are followed continuously. If accounting policies or assumptions change every year, it confuses the accountants and users of financial statements also get diverted due to heavy fluctuations in profits.

- This principle is important from both the accounting and auditing point of view as the following consistency gives accountants ease in recording business transactions. For auditors, it helps compare financial statements with last year.

- For shareholders and stakeholders, the consistency principle is important as it gives them the satisfaction that financial statements are more accurate and reliable. The correctness of a decision depends on the accuracy of financial information and the proper presentation of financial statements.

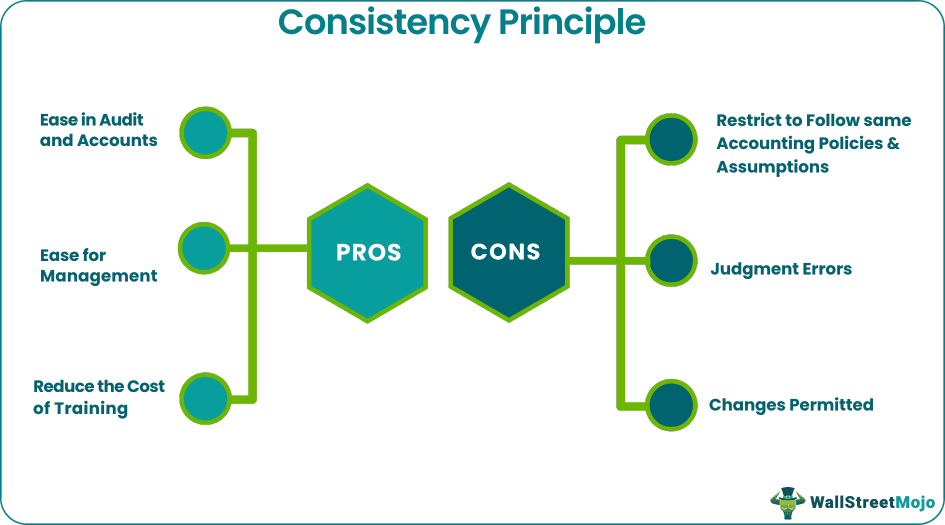

Advantages

- Ease in Audit and Accounts: It helps accountants record the accounting transactions and deal with the accounts. It helps the auditors compare the financial statements and provides the basis for the reliability of financial statements.

- Ease for Management: When accounting principles and estimates are applied consistently, management becomes familiar with the accounting procedures, technologies, treatments, and their effects and helps in proper decision making.

- Reduce the Cost of Training: If accounting principles are followed consistently, then only initial training is to be provided to the accounting staff, reducing the training cost.

- Makes the Financial Statements Comparable: By following the principle of consistency, the financial statements make the comparison, and it helps the auditors and users of financial statements compare financial statements.

Disadvantages

- Restrict to Follow the same Accounting Policies and Assumptions: This restricts the management to follow the same principles and assumptions over the years, and due to changes in technology, situations demand the change in accounting, but this principle restricts the same.

- Judgment Errors: As the Principle of consistency is based on whether change gives a better presentation in accounts, critical errors and problems arise.

- Changes Permitted: Only when the new method is considered better and gives a better presentation in accounts. The change and its effect on profit to be disclosed in the financial statements creates lots of calculations and pressure on accounting staff.

Conclusion

- It is a very important principle and is almost followed by all organizations, whether Governmental organizations or private organizations, profit-making or nonprofit organizations. According to this principle, all accounting policies are to be followed consistently so that financial statements make the comparison.

- It gives ease to both auditors and accountants. Due to consistency, auditors find the financial statements more reliable, and accountants give help in accounting procedures and making accounting records. The change and effect of the change are to be disclosed in the financial statements.

- Change is probably to be calculated from retrospective effect; hence it becomes difficult for accountants to calculate the effect of change retrospectively as it involves the maximum calculations. Changing accounting policies and estimates due to better presentation and preparation is a matter of judgment; hence conflict arises.

Recommended Articles

This has been a guide to What is the Consistency Principle & its Definition. Here we discuss the examples of consistency principle accounting and its uses & importance along with its advantages and disadvantages. You can learn more about it from the following articles –