What are Index Options?

The index option is a derivative instrument that tracks the performances of the entire index and gives the right to buy (or sell) units of an index at a contracted rate on a certain future date. Dow Jones Index Option is one example, where the underlying is based on 1/100th of the DJIA index, and the multiplier is $100.

- Index options allow buying or selling units of a whole index at a set price on a future date. Dow Jones Index Option is based on 1/100th of the DJIA index with a $100 multiplier.

- To calculate option premiums, we consider factors like spot price, strike price, days until expiration, stock price volatility, risk-free rate of return, and dividends. These determine the premium paid option buyer.

- Investors can use index options to hedge a stock portfolio or speculate on the index’s future. Various strategies include bull/bear spreads, covered calls, and protective puts. These strategies may reduce profits but also lower risks.

The most common examples of index options include (but are not restricted to):

- S&P 500 and SPX

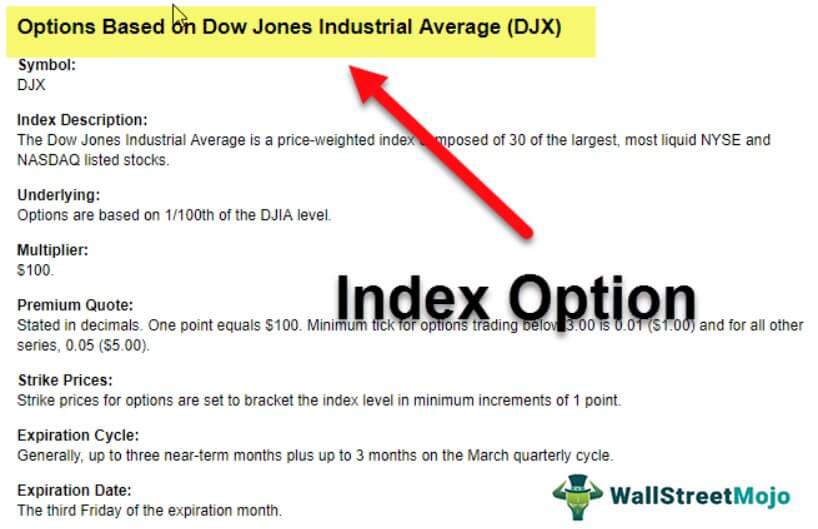

- DJX – Dow Jones Index

- IWB – iShares Russell 1000® Index Fund

- NDX – Nasdaq-100

- OEX – SP100 Index

- QQQ – Options on Nasdaq-100 Index Tracking Stock

- RMN – Mini-Russell 2000®

- RVX – CBOE Russell 2000® Volatility Index Options Index

Components and Types of Index options

Just like any vanilla option, Index options are characterized by:

- An underlying index

- The strike price of the option

- The maturity/ expiry date of the option

- Whether it’s a put or a call option

The underlying index is what differentiates one option from others, e.g., an option contract on S&P 500 will give an option buyer the right to buy (or sell) certain units (as earlier agreed upon in the contract) of the S&P index and the option writer will have to sell (or buy). Index options may have broad-based indices such as S&P or the Dow Jones or sector-specific indices that focus on industries like Information technology, healthcare, banking, etc., e.g., TSX composite bank index.

Index Option Example with Calculations

#1 – Pricing of an Index Option

Option pricing is the first and, ideally, the most complex. Pricing means the premium an option buyer must pay upfront to assume the right to buy (or sell). Option Premium theoretically can be calculated using a replicating portfolio, hedge ratios, and binomial trees. Still, more advanced methods like Black Scholes Merton pricing formula, Vanna Volga pricing, etc. are used in Financial Markets types.

The premium paid by the option buyer is calculated using various methods. The common inputs for Option Premium calculations are Spot Price, Strike Price, Days to expiry, Volatility of Stock price, Risk-free rate of return, dividends, if any, etc.

The Black Scholes Merton pricing formula is expressed as below:

c = S0 N(d1) – Ke-rTN(d2)

p = Ke-rT N(-d2) – S0 N(-d1)

Where, d1 = ln(S0/K)+ (r+σ2/2)T / σ√T

d2 = ln(S0/K)+ (r+σ2/2)T / σ√T = d1- σ√T

Source: quantlabs.net

Where

- c: Premium/ price of the call option

- p: Premium/ price of the put option

- S0: Spot price

- K: Strike price

- N(d1): Probability distribution of Spot (Delta of the option)

- N(d2): Probability distribution of forward price movement

- T: time to expiry

- r: Risk-free rate of return

- σ: Estimated volatility

The Vanna-Volga pricing model takes BSM one step further and adjusts the above formula for risks associated with volatility.

The main problem associated with the above models in pricing the index options is how to account for the dividends associated with different stocks in the index basket. To estimate the dividend component, individual stock’s dividend needs to be ascertained and weighted in proportion to each stock in the index. Another way is to use dividend yield published by data sources like Bloomberg.

#2 – Valuation or Mark to Market of an Ongoing Option Contract

The Value of the Call Option to the buyer (Or seller) after the contract till expiry keeps changing. Depending on that, either party can terminate the options contract by paying cancellation charges as agreed.

The calculation involved in Valuation is similar to the pricing of the option. Parameters such as volatility and time to risk-free expiry rate of return keep changing depending on how financial markets work.

#3 – Payoff Calculation

Assume that Firm A needs to invest in the Dow Jones index (DJX) after one month. Currently, Dow Jones trades at $267. Firm A is bullish on Dow Jones and believes the DJX will trade at $290 basis the analysis of financial data in the market. Another Firm, B, is bearish on the DJX and believes DJX will stay below $265.

The two firms will then formally enter into a Call option Contract with a Strike Price of $265 and a maturity of 1 month.

- Firm A will belong to the Call option contract and thus will have the right to buy units of DJX from Firm B for $265, even if the Shares of ABC are trading at $290.

- To get this right to buy, Firm A will have to pay some upfront amount known as Option Premium.

- Firm A will not be obliged to buy units of DJX if the price is less than the strike price of $265, thereby having downside risk.

- Firm B will be short on the Call option contract and have to sell the units of DJX irrespective of what rate DJX is trading at.

- The contract expires after a fixed expiry date, i.e., 1 Month

The concept can be explained using the below given chart, where there is a profit booking during fall in the index. Thus, in case of a bear market, an option strategy can be used comfortably to earn profit. But there is also the possibility to lose the entire investment. The strike price is assumed to be $195, with a premium of $3.90 for each contract.

Therefore, this is a long-put option which will earn profit only when the market will go down. Now if we assume that the index has gone down to $192, still the option has not even reached the breakeven. It will reach the breakeven only when the index goes below $191.10, which includes the strike price plus the premium. The lower the index moves, the higher is the profit for the trader. This is how the index option works.

Advantages of Index options

The following are the advantages of these options.

- Diversification: Index options are based on a large basket of stocks. This gives an easy diversification alternative to the investors.

- Volatility: Index options are less volatile, hence easier to predict.

- Liquidity: Since Index options are popular among traders, hedge funds, and investment firms, the volume available for trading is enough to keep the bid-ask spread in check, and prices are very close to a fair price.

- Cash Settlements: Index options are cash-settled. This makes settlements easier than the actual delivery of stocks in stock options.

- Relatively low-cost investment alternative to buying individual stock options.

Disadvantages of Index Options

Below are the limitations of Index options.

- Index options being a little less rewarding, may not be attractive for investors who are willing to take on higher risks for more rewards.

- The pricing models for options are very complex, and to account for underlying indices, it becomes way too complex to price.

Frequently Asked Questions (FAQs)

How do index options differ from stock options?

Whereas stock options are based on a single company’s shares, index options are based on a basket of equities reflecting either a large or a small band of the total market.

Are index options European style?

Index options are of the European kind, which prevents early exercise. On the other hand, equity options are always exercisable. While index options settle to cash, stock options agree to shares of the underlying stock.

What is the role of implied volatility in index options?

Implied volatility represents market expectations for future price fluctuations. Higher implied volatility usually leads to higher option premiums and vice versa. Traders often consider implied volatility when evaluating potential option trades.

Are index options regulated?

Yes, index options are regulated financial instruments and are traded on organized options exchanges. Regulatory bodies oversee these exchanges to ensure fair and transparent trading practices.

Conclusion

Index options can be used for hedging a portfolio of individual stocks or speculating the index’s future movement. Investors can implement various option trading strategies with index options viz. Bull spreads, bear spreads, covered calls, protective puts. These strategies may lead to lesser profits, but the risk is minimized greatly.

Recommended Articles

This has been a guide to What is Index Options and their definition. Here we discuss the types of index options and how it is priced, along with calculation examples, advantages, and disadvantages. You can learn more about derivatives from the following articles –