What Is A FHA Loan?

Federal Housing Administration Loans or FHA Loans is a mortgage process by which a loan is backed by the Federal Housing Administration and is specifically designed for people from low to moderate-income groups. Most applicants for these loans have a lower credit score. Moreover, FHA loan rates require borrowers to pay lower down payments than conventional loans.

For borrowers who have become homeowners for the first time, these loans might seem like the best possible options to acquire a mortgage loan. Since these loans are insured, banks are reassured and provide loans at concessional rates and low down payments as well. Otherwise, individuals with low credit scores might not secure loans easily.

- FHA loans are loans made by approved lenders and insured by the Federal Housing Administration.

- They are structured to help low to moderate-income groups of people qualify for home financing with more flexible credit and down payment requirements.

- The types of FHA loans include the FHA203(k) improvement loan, energy-efficient mortgage program, sections(245) loans, and fixed-rate and adjustable-rate loans.

- The Federal Housing Administration acts as a mortgage insurer for the borrower and reimburses the lender in case of default. This insurance has helped stimulate the housing market in the US for many decades.

FHA Loans Explained

FHA loans are a type of mortgage loan curated for borrowers who find it difficult to secure loans from financial institutions or private lenders. Therefore, the federal government insures these loans to ensure these individuals from the middle-income group can also fulfil their dreams of owning a home.

Although FHA loans started in 1934 to get out of economic depression and help people buy their own house, their actual application started in 1965. The Federal Housing Administration acts as an insurer for a mortgage for the borrower and payout debt if the borrower defaults.

FHA has successfully promoted the housing market in the US over many decades, and many Citizens can fulfill their dream of buying their own house at an early stage with the help of an FHA loan.

The FHA loan limit allows borrowers to make down payments of a mere 3.5% and borrow up to 96% of the home value if they have a credit score of 580 and above. For borrowers with a credit score between 500 and 579, this loan can still be availed if they can make a down payment of at least 10% of the value of the property.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

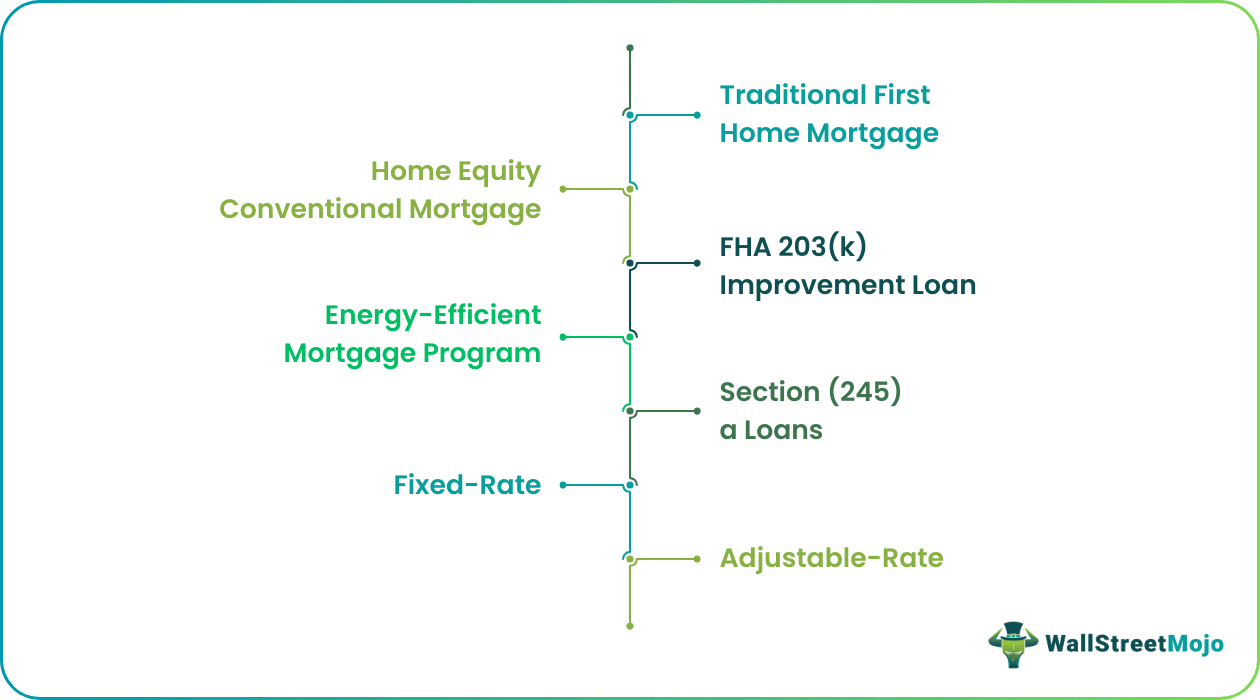

Let us understand the different types these loans and how borrowers can use a FHA loan calculator to find the best possible fit for their current financial conditions and credit scores.

#1 – Traditional First Home Mortgage

For individuals or families looking towards buying their first home.

#2 – Home Equity Conventional Mortgage

It is designed for senior citizens to help them convert the equity in the home to cash while retaining the title of the house. They can choose a monthly payment or line of credit or a combination of both.

#3 – FHA 203(k) Improvement Loan

This facility allows an individual to add the amount of renovation and certain repairs required on a home into the loan taken. i.e., this facility takes responsibility for home buying and improvements for the owner.

#4 – Energy-Efficient Mortgage Program

This program allows upgrades such as insulation, solar, or wind energy system installation for homes. The main purpose is to promote the concept of energy-efficient homes with lower operating costs. It will help the borrower in terms of reduction in bills over the years.

#5 – Section (245)a Loans

When the borrower expects an increase in their income level, this program initially charges a lower monthly payment, which increases gradually over time. It allows the borrower to buy dream homes at an early stage of their career and payout mortgage as the income level grows.

#6 – Fixed-Rate

A fixed rate is applied on the mortgage to help the borrower to understand payment terms and amounts. It is designed for borrowers who think loan interest rates can go up and avoid that, so they select this option.

#7 – Adjustable-Rate

The interest rate in such a program is adjusted as per market condition, so payment amount and terms depend on the interest rate in the market.

Insurance

FHA insures mortgage payment on behalf of the borrower, so if the borrower defaults, the lender will still be able to recover mortgage payment from FHA. FHA loan rates charges a fee to a borrower.

- Upfront Mortgage insurance premium of 1.75% on the base loan amount.

- The borrower pays a modest monthly fee with each ongoing payment, which depends on the level of risk involved for FHA. A shorter period and less amount reduce fee level, but charges are around 0.45% to 1.05% annually.

- Applicable for various properties like single-family homes, manufactured properties, duplexes, etc.

Examples

Let us understand the concept of FHA loan limit with the help of a couple of examples. These examples will help us understand the intricacies of the concept.

Example #1

If a borrower has borrowed $400,000 under FHA. Then,

Down Payment = $7000 and the monthly insurance premium is around 0.90%,

Therefore, 90% X $400,000 = $3,600 per year or $300 per month.

This amount is paid additionally over the upfront mortgage insurance premium.

If the loan to value ratio is below 90%, individuals pay the annual mortgage for around 11 years, and if it is above 90%, then the Individual will pay it throughout the loan term.

Example #2

When an individual looks to take out a loan backed by the Federal Housing Administration, the three things any lender looks at it are, sufficient income to repay the loan, required savings to pay the down payment and the credit score of the individual.

The Biden government has announced that it would become cheaper for first-time homeowners to purchase a home on a mortgage backed by the FHA. The dip in premium payments is estimated to be between $600 to $1,000 annually, depending on the size of the loan.

Even though $1,000 might seem like not too much has changed, for middle-income individuals, it might be a significant difference as they can spend it on necessities or even better, save or invest the amount.

Requirements

Let us understand the requirements that allow a borrower to under their FHA loan limits through the explanation below.

- Credit Score: To qualify for this loan, the minimum credit score requirement is 500.

- Debt to Income: The debt to income ratio indicates the percentage of your income before tax you spend on paying a debt, including mortgage, credit card, student loan, etc. The outstanding debt to income ratio is 50% or less.

- 5% Minimum Down Payment: FHA requirement changes as per an individual’s credit score, but a minimum of 3.5% of a down payment is applicable for an individual with a credit score higher than 580. For an individual with a credit score within the range of 500 to 579 minimum down payment of 10% is applicable.

- 75% upfront mortgage insurance premium payment of base loan amount.

- Primary Residence and Property Requirements: the house must be the primary residence of an individual or family and must qualify all property requirements as per law. E.g., Safety, security, and sound condition.

- Individuals must have at least two credit accounts. E.g., credit cards.

- It should be clear regarding the legal procedure without a history of fraud or any crime related to taxation or debt.

- The donor must declare down payment with the help of the third party in writing.

FHA Loan Limits for 2020: The loan limit for 2020 ranges from around $331,700 to $765,600, depending on area and country.

How To Apply?

The process of applying and understanding FHA loan rates can be bifurcated into four major steps. Let us understand each of these steps through the discussion below.

A – Personal and Financial Documents

- Social Security Number.

- Proof of US citizenship, legal permanent residency, or eligibility to work in the US.

- Bank statement for one month at least. With documentation of any deposit made during this time.

B – Lenders Requirement

- Credit reports.

- Tax records.

- Employment records.

- Additional paperwork for further proof if the borrower is a student or a fresh graduate.

C – The decision of the right plan applies to you.

D – Discussion with broker and loan officer regarding your application.

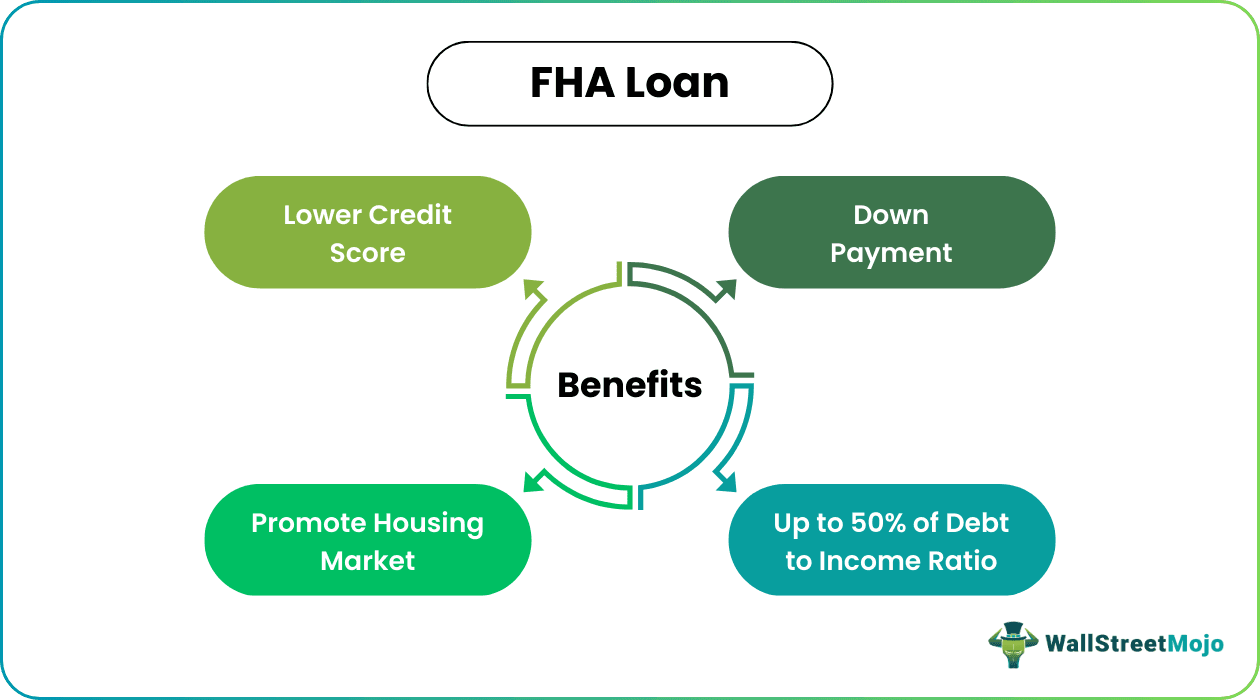

Benefits

Let us understand the advantages or benefits of using a FHA loan calculator and opting to buy a house that is backed by a federal entity through the points below.

- Lower Credit Score: FHA programs are specially designed for lower to middle-level income groups who don’t have a higher credit score required in the conventional loan process.

- Down Payment: Minimum Down payment of 3.5% is required, which is much less than the conventional loan process, where the minimum down payment requirement can be up to 20%, which is not possible for everyone.

- Up to 50% of Debt to Income Ratio: Even with higher debt-to-income ratio, up to 50% of income individuals can apply for these loans.

- Promote Housing Market: In terms of the economy, it is helpful and promotes the young generation to buy their own house.

Disadvantages

Despite the benefits mentioned above, there are a few factors from the other end of the spectrum that prove to be a hassle or hurdle for both the lenders and applicants. Let us understand the disadvantages of FHA loan limits through the discussion below.

- Mortgage Insurance Premium: Every month, a mortgage insurance premium can last for the entire loan term in case of a down payment of less than 10%.

- Property Standards: To qualify for FHA loan property, which the borrower wants to buy must qualify according to safety, security, and sound condition. These conditional requirements are observed strictly.

- Loan Limit: Compared to the conventional loan process, FHA loans have to limit the location of a property. An agency decides the minimum and maximum amount for a loan, and only that much can be provided as a loan.

FHA Loan Vs Conventional Loan

Let us understand the differences between a conventional loan and a FHA loan rate through the comparison below.

| Sections | FHA Loan | Conventional Loan |

|---|---|---|

| Definition | A loan insured by the Federal Housing Administration is specially designed for individuals falling under lower to middle-income level groups to help them buy their own house. | A loan through a Bank or any financial institutions qualifies as per their terms and conditions and can provide proof and necessary payments. |

| Credit Score | Minimum 500 | Minimum 620 |

| Down Payment | Individuals above credit score of 580 minimum 3.5%, For an individual with a credit score within a range of 500 to 579 at least 10% of down payment. | Minimum of 3% for individuals with a high credit score and up to 20% for lower credit score. |

| Period | 15- 30 years | 10 – 30 years |

| Insurance Fee | Upfront MIP of 1.75% on Loan Base amount and up to 11 years or throughout loan term depending on Loan to Value ratio. | Not applicable on a down payment of 20% or if a loan is paid up to 78% of its value. |

| MIP | Upfront MIP of 1.75% on Loan Base amount and Annual payment between 0.45% to 1.05%. | 0.5% to 1% of the loan amount per year. |

| Assistance Available | Yes | No |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions

What is an FHA loan with bad credit?

An FHA loan with bad credit is a type of home loan insured by the Federal Housing Administration and designed for individuals with less-than-perfect credit. These loans have more flexible credit requirements than conventional ones and may be a good option for those with lower credit scores or limited credit history.

What is an assumable FHA loan?

An assumable FHA loan is a type of mortgage that allows a new buyer to assume the remaining balance of an existing FHA loan from the original borrower. This means the new buyer takes over the loan with the same terms and interest rate as the original borrower without applying for a new loan. Assumable FHA loans can be a good option for homebuyers in a rising interest rate environment or those who want to avoid paying closing costs on a new loan.

Is it possible to refinance an FHA loan?

Yes, one can refinance an FHA loan. FHA loans can be refinanced through a program called the FHA streamline refinance. This program is designed to help FHA borrowers refinance their existing FHA loans to lower their monthly payments or reduce their interest rates. The FHA streamline refinance does not require a new appraisal or credit check and has more relaxed documentation requirements than other refinance programs.

Recommended Articles

This has been a guide to what is a FHA Loan. Here we explain its requirements, insurance, examples, how to apply, and compared it with conventional loans. You can learn more about Corporate Finance from the following articles –