Part of our Types of Bonds guide

What Is A Floating Rate Note (FRN)?

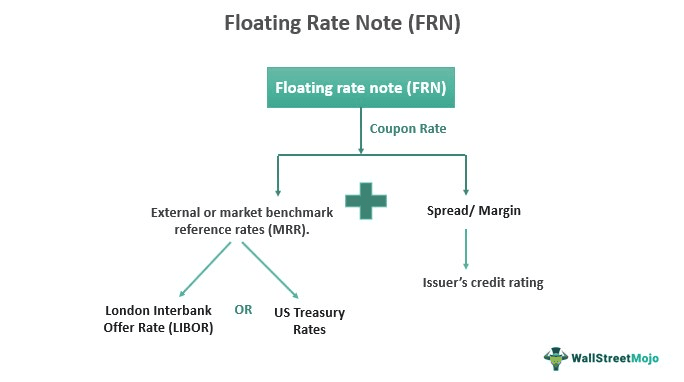

A Floating Rate Note (FRN) is a financial debt instrument that has a variable coupon rate. The coupon rate depends on external or market reference rates (MRR) like the London Interbank Offer Rate (LIBOR) or the US Treasury Rates plus a spread.

Thus, the interest will fluctuate depending on reference rate changes. The spread, also known as the margin, remains constant, is expressed in terms of basis points, and depends on the issuer’s credit rating. It is inversely proportional to the issuer’s creditworthiness. The MRR periodically resets, which changes the FRN’s coupon rate accordingly.

Key Takeaways

- An FRN is also called a floater and has a variable or a floating interest rate.

- The interest depends on an external benchmark rate which might be the US Treasury Rates or London Interbank Offer Rate (LIBOR) plus a spread.

- The external rate varies, due to which the interest on the FRN fluctuates. The spread remains constant.

- The spread in the interest rate depends on the issuer’s credit rating and is fixed when the bond is issued.

Floating Rate Note Explained

FRNs are bonds that do not have a fixed coupon payment. The rates have two parts, one is spread that remains fixed, and another is variable, depending on the benchmark rates or MRR like LIBOR or US Treasury Rates.

The spread identifies with the issuer’s credit rating, and the benchmark rate fluctuates, making the interest and the cash flows of an FRN variable. The coupons are mostly given quarterly. But they can also be monthly, quarterly, semi-annually, or yearly.,

Changes in market interest rates have little effect on the floater’s interests since it resets periodically. Thus, the risk of a fall in bond value due to a rise in interest rate is very low, making FRN highly preferable for investors who expect an interest rate increase.

An inverse floating rate note will have a coupon that is inversely related to the reference rate in which, when the interest rate rises, the interest in the inverse floating rate note will go down and vice versa, which is preferable to investors expecting a fall in reference rates.

An FRN or floater may be floored, ensuring the interest does not fall beyond a point or cap, which prevents the rate from rising beyond a level. A capped FRN is helpful for the issuer, which ensures that interest payment will not exceed a limit during rising rates. An FRN can have both a cap and a floor feature in it. Such a note will be called a collared note.

A floating rate note duration usually ranges from two to five years. They are issued by government-sponsored enterprises (GSEs) in the US and financial institutions and banks in Asia and Europe.

Floating Rate Note Pricing And Valuation

The coupons of FRNs have two parts. One part is the market reference rate (MRR), which depends on the benchmark rates like LIBOR or US Treasury Rates, and the other is the spread, which measures the issuer’s creditworthiness. The most common rates are three months MRR plus 20 basis points (0.2%), where one bps is 1/100th of a percentage. Here, the 20 basis points (20 bps) are the spread.

Assuming a floater with semi-annual coupon payments in June and December of a particular year, 20XX, the rate is expressed as a six-month MRR plus a spread of 125 bps. Now let us assume that the MRR is 3% in December 20XX. Thus, as per the floating rate note formula in the coming year 20XY, during June, the coupon rate will be 3% + 1.25% = 4.25%.

Again, if the MRR reduces to 2.75% in June 20XY and the spread remains the same, as per the floating rate note formula, the new FRN coupon in December of that year 20XY will be 2.75% + 1.25% = 4%.

The above example shows how creditworthiness is calculated using the MRR and the spread. But while selecting a note, an investor must check the issuer’s creditworthiness to ensure there is no default in coupon payment.

Floating Rate Note Discount Margin

Discount margin is the average return expected from a bond or FRN over and above the market reference rate. The discount margin depends on the price of the floating rate financial instrument, which can be calculated using a floating rate note calculator. Since the interest rate on the bond is variable and fluctuates due to changes in the reference rate, the margin is estimated by studying the pattern of return from issue to maturity.

The discount margin method is used to calculate the spread part of the coupon payment. Through this method, the margin helps in equating the present value of the expected cash flows of the future to the current market price.

The concept of the time value of money is used to calculate this margin across N number of periods. The following variables are considered:

PV – present value

QM – quoted margin

M = bond period

FV – face value

R – A reference rate

DM – discount margin

The calculation is as follows:

PV=[(R+QMm×FV)/(1+R+DMm)]+[R+QMm×FV/(1+R+DMm)^2] +……+[(R+QM/ m)×FV+FV/ (1+R+DMm)^N]

However, the above calculation needs a floating rate note calculator or a financial spreadsheet.

Examples

Let us understand the concept with some examples.

Example #1

ABC Fingroup, a US-based financial institution, has issued floaters for raising funds and helping investors diversify their investments. The notes have the following features:

- The minimum purchase price is $100

- Duration of 3 years.

- At maturity, the investors will get the entire face value.

- The coupon payment is quarterly, with a variable rate with a 3-month Treasury Bill benchmarked at 4.50%.

- Coupons will be subject to federal income tax.

- They may be sold before or at maturity.

ABC Fingroup issued floating-rate bonds with the above features. The rising interest rate environment in the US led to a subscription by a large number of investors.

Example #2

The continuous rise in federal interest rates has allowed investors to earn a good return on floating-rate notes. They offer interest that is more than the inflation rates, with lower volatility. As a result, FRNs are suitable for those looking averse to duration and credit risk.

Historically, floaters have shown a very low volatility level compared to other investment options, but their yields have always been down due to their shorter duration. However, slowly the yield levels are taking over the rise in inflation and showing a positive future outlook.

Example #3

Goldman Sachs has announced that it will redeem all outstanding and issued FRNs. After redemption, no interest will accrue in any of them. Accordingly, all investors should contact their banks or respective brokers for the process and obtain any payment of any floaters in which they have an interest.

Advantages And Disadvantages

FRNs or floaters have certain advantages and disadvantages, as follows:

#1 – Advantages

- It is beneficial for investors who expect interest rates to go up since rising interest will also raise the coupon of floaters.

- The floating rate note duration is less than fixed-rate notes. This feature is helpful because it helps limit the fall in the value of bonds in a rising interest rate environment.

- From the issuer’s point of view, a cap and floor FRN estimate the range within which the interest payment may vary.

- The reset period in the bond’s prospectus informs the investor how frequently the interest rate will change.

#2 – Disadvantages

- The FRN’s coupon will also fall in the falling interest rate environment, which is a loss for investors.

- The FRN coupon rate has a spread part, which depends on the issuer’s creditworthiness. Therefore, if this rating falls, the overall interest will also decrease.

- The yield is less for FRN due to less duration of the bonds. Comparatively, fixed-rate bonds have high yields due to more prolonged periods.

- The floater’s interest rate may rise slower than the market rate. Thus, the investor may lose interest amount.

- The issuer may default on the FRN’s interest payment.

Frequently Asked Questions (FAQs)

Are floating rate notes a good investment?

They are good investment options because they offer beneficial interest rates, especially in a rising rate environment, and limit the fall in bond value. In addition, the default risk is less due to issuers being mostly enterprises backed by the federal government.

Are floating rate notes money market instruments?

They are bonds by nature, so they are a part of the bond market. However, like money market instruments, they are not liquid or of a duration of less than one year.

Are floating rate notes liquid?

FRNs are not liquid because they are bonds that invest their holding in fixed-income securities and floating-rate funds. However, liquid funds invest their corpus in securities that have a concise duration, like bank deposits, commercial papers, short-term treasury bills, etc.

Are floating rate notes secured?

They are not free of default risk. Even though government-backed enterprises mainly issue them, some private entities also issue FRNs. They are also exposed to credit default risk. Therefore, verifying the issuer’s creditworthiness is necessary before investing in them.

Recommended Articles

This has been a guide to what is a Floating Rate Note (FRN). We explain its examples, pricing, advantages, disadvantages, valuation, and discount margin. You can learn more about finance from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.