Part of our Financial Statements guide

Interim Report Meaning

An Interim Report is financial statements reported by a firm for less than one year (semiannually, quarterly, or even monthly basis) and normally reviewed by a company’s internal auditors rather than going for a complete statutory audit which would be impractical and time-consuming considering the frequency with which these reports are published.

Although regulators prescribe an annual reporting of data, it helps establish better and transparent communication with the investors by providing updated information between annual reporting periods.

As per ICAI – “Timely and reliable interim financial reporting improves the ability of investors, creditors and others to understand an enterprise’s capacity, to generate earnings and cash flows, its financial condition and liquidity“.

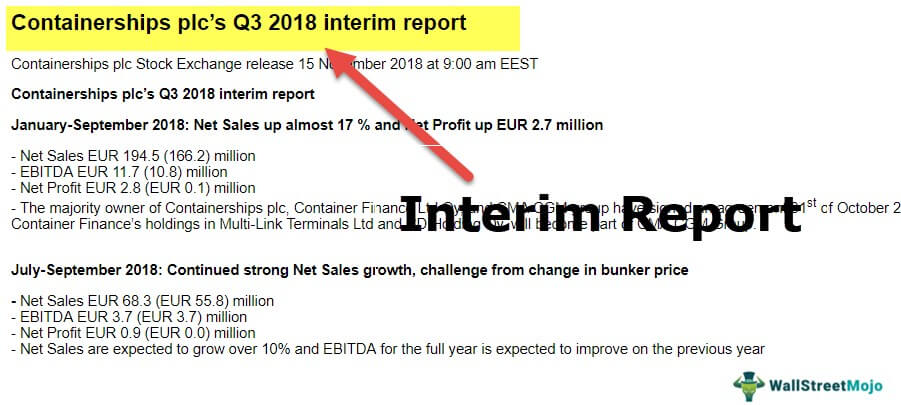

Interim Reporting Example

Interim financial reports are declared at various periods providing evidence about the firm’s performance at different intervals during the accounting period.

- Public listed companies come up with quarterly financial numbers,

- Real estate firms come up with their numbers on a Project basis as and when these projects are completed.

They implicitly provide essential analytical information.

Consider the following financials of a Major IT company.

| Financial Performance | Fiscal Year 2018 | Fiscal Year 2017 | Growth | Quarter ending Dec 31 2018 | Quarter ending Dec 31 2017 | Growth |

|---|---|---|---|---|---|---|

| Revenues | 70522 | 68484 | 3.0% | 17794 | 17273 | 3.0% |

| Gross Profit | 25392 | 25231 | 1.0% | 6344 | 6433 | -1.4% |

| Operating Profit | 17148 | 14353 | 19% | 4319 | 4334 | -0.3% |

| Profit after Tax | 16029 | 14353 | 12% | 5281 | 5154 | 2.5% |

Even though the operating profit has risen on a year-on-year basis, there is a drop in quarterly numbers. It suggests that Q4 was not good for the firm, even though there was a good 12% annual profit increase.

The information implicitly signifies the seasonality of the IT business in the Oct-Dec quarter. This info should guide the management in planning for their long-term strategic initiatives.

Interim Report Explained in Video

Objectives of Interim Reporting

The investment decisions are taken around the year. Investors don’t wait for the annual reports declared at the end of the fiscal year. With companies relying not only on organic but also on inorganic growth, annual data is insufficient to evaluate the industry’s and the firm’s developments and earnings projections. In such a dynamic business environment, interim reports offer a better periodic snapshot to the shareholders. Providing current information will always keep a firm in the investors’ good books, making the allocation of capital investment easy, leading to better market liquidity, which is the primary goal of capital markets.

Following are the major objectives :

- Estimation of annual earnings based on interim financials

- Make cash flow projections

- Identify turning points in the firm’s financial status

- Evaluate management performance

- To formulate internal control procedures

- To supplement the annual report

Advantages

- It helps in establishing a better connection with the investors.

- It is beneficial for big conglomerates that are running multiple business lines, helping them track if their short-term initiatives are in line with the long-term strategy.

- Material misstatement (Errors and frauds) in a financial statement can be detected and prevented early compared to an annual report.

- It helps in the implementation of a comprehensive internal control procedure, which further makes accounting policies robust.

- Declaration of interim dividend is possible when financial statements are reported for short periods incentivizing the shareholders to hold on to their investments.

Challenges/Limitations

- Although interim announcements reduce the reporting period, it increases the impact of errors in estimations leading to concern in reporting accurate information.

- Various operating expenses are incurred in one period, and the benefits are earned in the subsequent periods like advertising, repairs, and other maintenance costs. Such expenses can distort the firm’s financial status for an interim period, although in the longer term might be quite helpful.

- The impact of seasonality and economic cycles is felt more in interim statements and almost nullified in the Annual report. They are also more prone to management manipulation by presenting strong quarterly growth in the early and ending quarters. This difference affects the consistency and comparability of such reports

- Inventory is the main element of revenue generation in any business. Determination of the quantity of inventory and its valuation leads to unnecessary adjustments in the interim financial statements Periodic inventory calculations in an interim period are repetitive, time-consuming, and error-prone.

- The absence of a regulatory framework for disclosure practices leads to confusion as to what extent these should be provided. The disclosure can differ between two companies within the same sector, misleading to the shareholder.

- Interim Report creates an overemphasis on short-term results, sometimes presenting a distorted picture which can be detrimental for both investors and companies

Guidelines

A firm may report limited information to avoid redundancy and reduce complexity considering the nature of interim reports. However, it should contain at least the following components:

- Condensed Balance sheet

- The condensed Cash flow statement

- Condensed P &L statement

- Explanatory notes relevant to the Data reported

There are also some guidelines for explanatory notes. It should include:

- A disclosure that the same accounting policies are followed in the interim report and followed in annual reporting.

- Notes on the items affecting sections of financial statements like assets, liabilities, equity, Income;

- Any new issuance of stocks, buybacks, repayments, or restructuring of debt;

- Dividends for equity shares.

- Impact of new acquisitions or long-term investments incurred during the interim period.

- Any investor or regulatory complaints during the interim period;

Conclusion

Interim reporting is not much different from Annual reporting in terms of content but only differs in the timing of the publication. It is a subset of annual reporting that provides all important financial data like Revenues, Income, expenditure, losses, etc., for a particular period. A firm doesn’t need to publish it, but doing so can benefit the firm, investors, and stakeholders, leading to a better and mature economic ecosystem.

Recommended Articles

This article is a guide to Interim Report. Here we discuss this topic in detail, including its meaning, example of interim financial reporting, objectives, advantages, challenges, and limitations. You can also take a look at some of the useful articles:-