Restatement Meaning

A restatement corrects inaccuracies in financial statements pertaining to past accounting periods. These inaccuracies are caused by accounting errors, inaccurate financial reporting, clerical mistakes, frauds, and non-adherence to GAAP or accounting standards.

Not all errors have the same impact. Material errors are those that affect the final reporting. These impact financial figures to the extent that it results in inaccurate analysis and comparison. Financial statements are restated to ensure that stakeholders get an accurate picture of the company’s financials.

- A restatement is the amendment of financial statements pertaining to one or more previous accounting periods. It rectifies errors resulting from material misappropriation.

- Material errors include clerical faults, non-compliance with accounting standards, fraud, or inaccurate financial reporting.

- Restating a financial statement also arises when there are changes in the accounting standards, changes in GAAP, changes in the corporate structure, or changes in the type of reporting organization.

- Financial statements can be restated as a reissuance, revision, or out-of-period adjustment.

Restatement Explained

A restatement is changing something that has been declared previously. Financial statements are restated to report errors. Not all errors have the same impact. Material errors are those that affect the final reporting. These errors impact financial figures to the extent that it results in inaccurate analysis and comparison.

Although accounting managers are responsible for presenting the correct financial reports every year, it is the auditors’ responsibility to find errors in them. Such misappropriations can be identified by the internal auditors or the external authorities.

The issuance of restated financial statements is necessary so that the stakeholders, investors, financiers, and creditors get the correct picture of a company.

Reasons to Restate a Financial Statement

GAAP highlights the following three major reasons for restatement:

- Accounting Error: This includes all accounting mistakes like recording errors, improper accounting methods, and lack of information. As a result, the financial statements have to be restated.

- Non-Compliance with GAAP: Statements that fail to meet the Generally Accepted Accounting Principles guideline or any other accounting standard require restatements.

- Fraud or Misrepresentation: If the company or its accounting personnel deliberately reported incorrect financial information in the previous years, restating becomes necessary.

If any of the above errors are found, it has to pass the materiality test. Materiality is decided on the basis of impact. An error is considered material if it affects the stakeholders in their decision-making. Therefore, all errors do not need restating.

In addition to significant errors, there are some other errors:

- Changes in GAAP: If accounting standards like GAAP put forth new accounting methods or rules applicable from the current accounting period, restarting is required. However, if applied retrospectively, such changes would impact prior statements as well. In order to facilitate comparison then, restatement becomes necessary.

- Changes of Reporting Entity: If there are changes to the corporate structure or ownership type of the business entity, the comparative statement of the previous years has to be restated. Restating is done only when there is a significant impact on financial reporting.

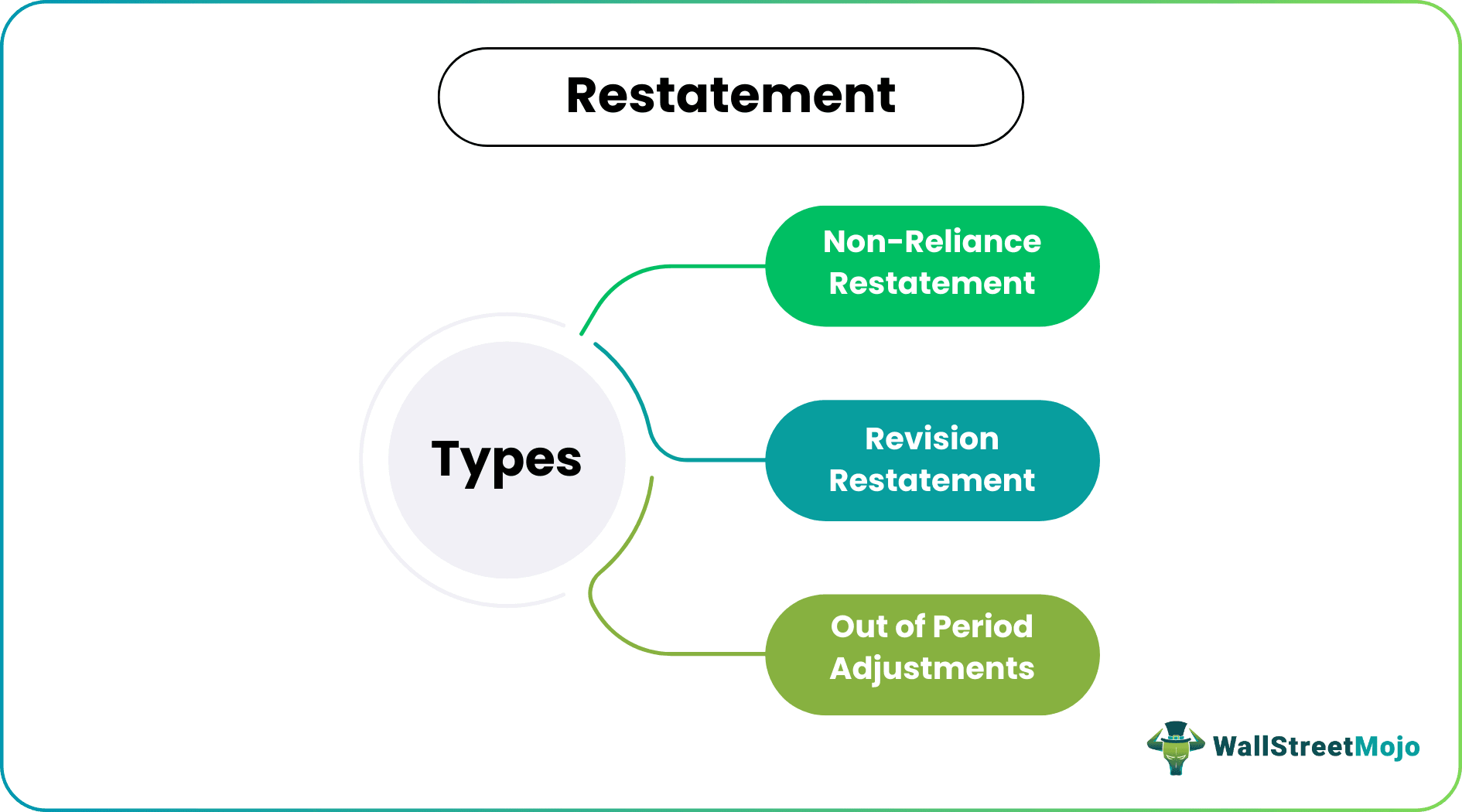

Types of Restatement

The errors found in the previous years’ financial statements determine the type of restatement the company has to proceed with. These are explained below:

#1 – Non-Reliance Restatement

A reissuance or “Big R Restatement” is issued when there are mass errors found in statements pertaining to earlier periods. Mass errors render previous and current financial statements unreliable.

The company, therefore, must restate publicly by filing an 8K form—an audit opinion states the restatement. An audit opinion is a statement expressed by independent auditors to their client’s financial statements as the result of auditors’ examination.

#2 – Revision Restatement

The stealth or small r restatement is released when a consolidated material error is discovered in various financial statements pertaining to previous years. Since it cannot be rectified with a one-time adjustment, doing so will result in misrepresentation of the current period’s financial statement. Therefore, the company has to restate prior financial statements. This has to be mentioned in the footnotes of the current statements.

#3 – Out of Period Adjustments

If the degree of error is not significant enough to affect the reliability of any period’s financial statement, then it doesn’t require any restatement. However, its effect can be taken collectively and incorporated into the current financial statement. This should be accompanied by a disclosure note since it will affect the comparability.

Effect and Prevention

Every company should know the consequences of restating and ways to avoid one. Following are the effects of restating:

- If restatement is issued because of integrity or operational issues, the stakeholder’s confidence in the company shatters.

- It generally results in excessive audit fees. The auditor has to dig into the errors and determine the type of restatement required for the particular case—it consumes a lot of time and effort.

- It furthers hampers the goodwill and credibility of the company since the investors, shareholders, and other associated parties lose trust in the firm’s accounting system.

- Moreover, it undermines the company’s valuation and thus limits funding.

Following are the ways of avoiding restatements:

- It is essential to conduct internal audits and accounts review before issuing the financial statement.

- Another crucial measure is to ensure a strong and effective internal control system to check misappropriation and fraud.

- Firms should address the accounting issues and the smallest error before it’s too late. Firms must develop a culture of trust and transparency within the organization to eliminate chances of manipulation.

- It is equally important to have a team of expert accounting professionals who prepare accurate financial statements.

Restatement Example

Molson Coors Brewing Co. is a Chicago-based beverage company. They announced restated financial statements pertaining to 2016 and 2017. Molson’s financial reporting bore material weakness related to deferred tax liabilities resulting in accounting error in its income tax computation. Therefore, under the guidance of its audit committee and Pricewater Coopers LLP, the firm decided to go for a non-reliance restatement of its financial statements.

Source – www.sec.gov

Frequently Asked Questions (FAQs)

What is a Restatement?

Restating is the process of making amendments to the released financial statements pertaining to one or more previous accounting periods. This is done to rectify the material errors. The misrepresentation can be related to clerical mistakes, non-adherence to GAAP, accounting faults, and fraud.

What is a prior period adjustment?

A prior period adjustment refers to the rectifications made to the previous years’ financial statements. It is a rectification of various accounting inaccuracies like wrong accounting methods, mathematical mistakes, or the ignoring of crucial information.

What is the difference between a revision and a restatement?

In accounting practice, any immaterial error can be corrected by revising the company’s financial statements. This can be done for any of the previous three accounting periods. However, such rectification is permitted only once in every financial year. Also, the company has to seek permission from the respective Court of Audit.

On the contrary, restatement corrects material inaccuracies in the previously issued financial statements (i.e., past accounting periods).

Recommended Articles

This article has been a guide to What is a Restatement & its Meaning. Here we discuss restatement types, examples, effects, and prevention. You can learn more about it from the following articles –