Part of our Real Estate Investing guide

What Is A Listed Property?

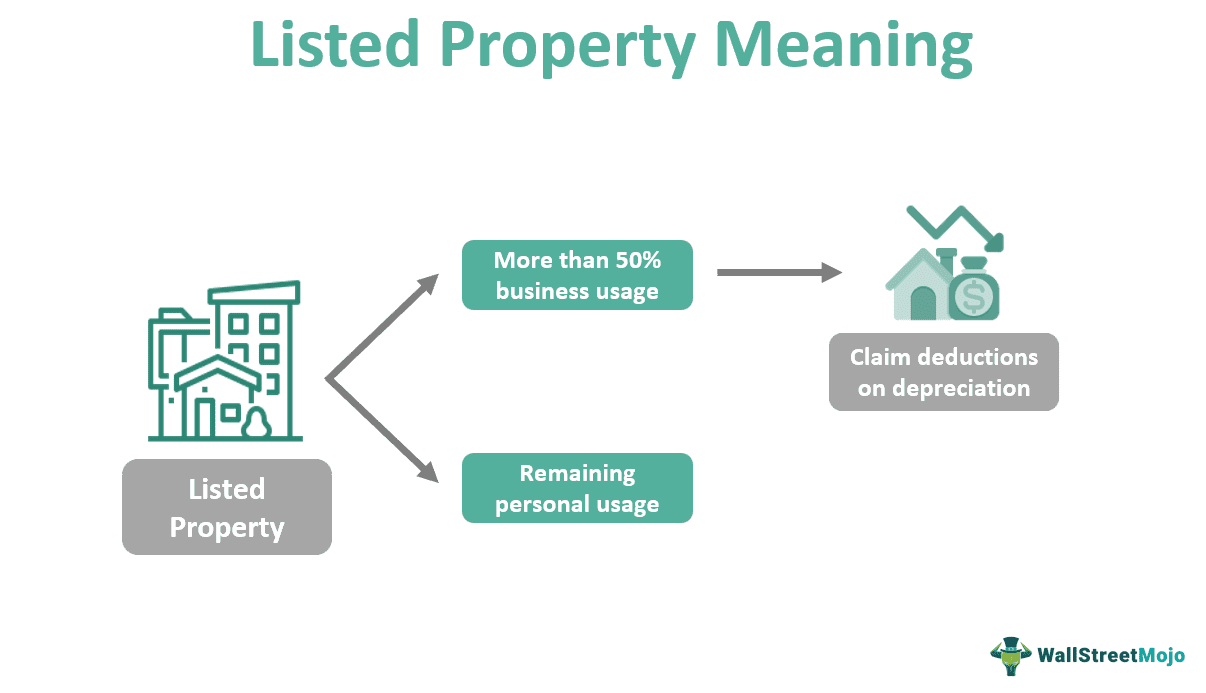

Listed property is a type of asset mainly used for business purposes and is subject to depreciation. The property can also have personal uses, but it should be used at least 50% of the time as a business asset to qualify for tax benefits and deductions.

Listed property or mixed-use property taxation was introduced by the Internal Revenue Service (IRS) to prevent people from claiming tax deductions on their personal-use property by representing it as a business asset. Examples of mixed-use property include vehicles, electronic equipment (except mobile phones, computers), etc.

- The listed property refers to any property used for business purposes at least half the time. It can also be used for personal purposes, but only for the remaining time.

- The property must satisfy the 50%-mark (predominant use test) to qualify for special taxation,

- Otherwise, it will be treated as personal property, and the tax treatment will differ. For this, the taxpayer should maintain proper records regarding its use, expenditure, and appropriate measure exclusively for business.

- A mixed-use property is depreciable and follows the modified accelerated cost recovery system.

Listed Property Explained

Listed property is a special kind of depreciable property. Special rules regarding the use of the property for business and personal use were laid out to prevent people from claiming tax deductions for personal-use property in the name of business-use ones. Listed property tax is an important area of concern for the IRS. IRS clearly states the rules for depreciation and taxation of mixed-use property. Let’s see how it works.

Firstly, taxpayers can claim deductions on mixed-use property in Form 4562 (deduction for depreciation and amortization). However, the property must pass the predominant use test, which proves that the property has a business-related use more than 50% of the time. In addition, all properties with partial or complete business use are liable for depreciation from the time it was put into the business.

The basis for listed property depreciation in most cases is the modified accelerated cost recovery system (MACRS). MACRS is of two types – general depreciation system (GDS) and alternative depreciation system (ADS). The GDS should be followed for most properties unless otherwise specified.

ADS is used in some situations, like when a property is used for business and personal use but does not qualify for the predominant use test, tax-exempt property, etc. Similarly, MACRS is not used in some cases, such as intangible property or property placed in service before 1987.

After filing Form 4562, taxpayers can attach the Form to the current year’s tax returns. Then, they can claim the section 179 deduction. The IRS provides percentage tables to help taxpayers calculate the applicable depreciation rates on the property. The total depreciation depends on the depreciation followed (cost/other) and the period of the property.

Examples

Let’s look at some examples to understand listed properties better.

Example #1

Jane purchased a pickup truck in 2017 for $20,000 for her business. But she used it at times for personal purposes too. So she claimed the section 179 deduction. Here’s how it went.

The pickup truck is a 5-year property (according to the IRS), and the percentage table A-8 is applicable.

| Year | Depreciation percentage | Depreciation cost |

|---|---|---|

| 2017 | 10% | 2000 |

| 2018 | 20% | 4000 |

| 2019 | 20% | 4000 |

| 2020 | 20% | 4000 |

| 2021 | 20% | 4000 |

| 2022 | 10% | 2000 |

Thus, the calculation of depreciation can be a complex process. But the IRS percentage tables can be helpful if one uses the right table.

Example #2

Mobile phones and computers were once considered listed properties. They had significant business use and personal use. Hence, they were eligible for a section 179 deduction. However, over the years, the exponential rise in mobile phones and personal computers lends doubt to the purely business use of such devices.

The main aim of the IRS when it introduced the listed property tax rules was to prohibit taxpayers from wrongly claiming deductions. Therefore, keeping this in view, the government removed the two items – mobile phones and computers – from the listed property. The Small Business Jobs Act has restricted the use of mobile phones as a listed property as of January 01, 2010. Later, under the Tax Cuts and Jobs Act, computers and other peripheral equipment were removed from the list, with effect from January 01, 2018.

Advantages And Disadvantages

Let’s analyze the pros and cons of the listed properties.

| Advantages | Disadvantages |

| The government can prevent tax avoidance by restricting those who represent personal use properties as business-use. | Although the taxpayers are required to present records of the business use, many people misrepresent the information for maximum tax benefits. |

| Taxpayers can enjoy maximum utilization of assets. | Many businesses use electronic devices like computers and cell phones in this digital era. Thus, the removal of these devices from the list can be disadvantageous to small businesses. |

| Taxpayers can also claim tax benefits for the commercial use of a property. |

Listed Property vs Direct Property

- The listed property has part business and part personal use. It can also manage the owner’s investments (computers put in service before 2018). However, half of its usage should be related to business.

- Direct property is either a fully commercial or fully personal asset, i.e., it is not for mixed-use.

- The main difference between these two properties would be the taxation they follow. Assets are subject to depreciation. But a business can claim the depreciation on its assets as deductions.

- A business specifying the list of its direct property can easily file for depreciation. However, for a listed property, the extent of use of the property for business use determines the depreciation.

Frequently Asked Questions (FAQs)

1. What is the listed property for depreciation?

Listed property depreciation is an important procedure with legal implications. Any person claiming deductions for the use of mixed-use property should depreciate the property regularly and according to the method suggested by the IRS. Usually, GDS applies to most properties. However, there are some exceptions.

2. What is the listed property on Form 4562?

Any taxpayer claiming deductions on a mixed-use property should file Form 4562 for depreciation and amortization. Before this, their property has to pass the predominant use test by proving that it functions as a business test for more than half the time. After doing so, they can claim a section 179 deduction.

3. Are computers still listed properties?

The answer depends on the purchase date or the computer’s business use date. Computes put into business use before January 01, 2018, are listed and depreciable. But computers purchased after this date are not considered listed property under the Tax Cuts and Jobs Act.

Recommended Articles

This has been a guide to what is Listed Property & its meaning. Here, we explain it with examples, its advantages, disadvantages, and comparison with the direct property. You can learn more about financing from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.