What Is Deed In Lieu Of Foreclosure?

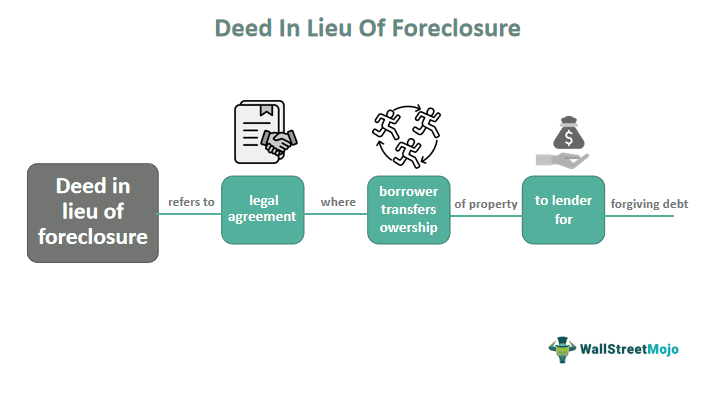

A deed in lieu of foreclosure is a legal agreement between a borrower and a lender that allows the borrower to transfer the ownership of their property to the lender in exchange for the lender forgiving the outstanding debt. Essentially, the borrower voluntarily gives up the deed to their property instead of going through foreclosure.

The purpose of a deed in lieu of foreclosure is to provide a mutually beneficial solution for both the borrower and the lender. For the borrower, it can provide a way to avoid the negative consequences of foreclosure on their credit score and financial stability. For the lender, it can provide a quicker and less costly way to recoup some of their losses on a defaulted loan.

- Deed in lieu of foreclosure allows the borrower to transfer property ownership to the lender in exchange for forgiven debt.

- Provides mutually beneficial solutions for both borrower and lender.

- Helps borrowers avoid the negative consequences of foreclosure and reduce the financial burden on the estate of a deceased homeowner.

- It may have tax implications and impact borrowers’ credit scores.

- Borrowers should carefully consider the pros and cons and seek professional advice before proceeding.

How Does Deed In Lieu Of Foreclosure Work?

The deed in lieu of a foreclosure agreement, allows the borrower to voluntarily transfer the ownership of their property to the lender. In exchange, the lender agrees to forgive the outstanding debt and refrain from pursuing foreclosure proceedings against the borrower.

To initiate the process, the borrower must typically contact the lender and express their desire to participate in a deed in lieu of foreclosure. The lender will then evaluate the borrower’s financial situation and the property’s value to determine whether a deed in lieu of foreclosure is a viable option.

If both parties agree to move forward with the agreement, the borrower will sign over the deed to the property and vacate the premises. The lender will then assume ownership of the property and release the borrower from any further obligations related to the loan.

It is important to note that the lender may still report debt forgiveness, which could result in tax consequences for the borrower. Additionally, the lender may require the borrower to meet certain conditions, such as maintaining the property and paying any outstanding liens or taxes, before agreeing to the deed in place of foreclosure.

Examples

Let us look at the examples to understand the concept better.

Example #1

Suppose John is a homeowner who has fallen behind on his mortgage payments due to financial difficulties. His lender, ABC Bank, has initiated foreclosure proceedings against him, but John is eager to avoid the negative consequences of foreclosure on his credit report and financial stability.

John contacts ABC Bank and expresses his interest in a deed in lieu of a foreclosure agreement. Hence, after evaluating John’s financial situation and the value of his property, ABC Bank determines that a deed in lieu of foreclosure is a viable option.

ABC Bank and John agree to the terms of the agreement, which stipulate that John will sign over the deed to his property and vacate the premises. Thus, in exchange, ABC Bank will forgive the outstanding debt and refrain from pursuing foreclosure proceedings against John.

John signs over the deed to his property and vacates the premises, and ABC Bank assumes ownership of the property. However, the bank may still report the debt forgiveness to the IRS (Internal Revenue Service), which could result in tax consequences for John. Additionally, the bank may require John to maintain the property and pay any outstanding liens or taxes before completing the deed in lieu of foreclosure.

Example #2

Consider that Sarah owns a commercial property she has been using as collateral for a loan with her lender, XYZ Bank. Unfortunately, Sarah has fallen behind on her loan payments due to financial difficulties and is in danger of defaulting.

Recognizing that foreclosure proceedings could be costly and time-consuming, XYZ Bank offers Sarah a deed in lieu of a foreclosure agreement. In addition, if Sarah agrees to transfer ownership of the property to the bank, XYZ Bank will forgive the outstanding debt and refrain from pursuing foreclosure proceedings against her.

Sarah agrees to the terms of the agreement, signs the deed to the property, and vacates the premises. As a result, XYZ Bank assumes ownership of the property and releases Sarah from any further obligations related to the loan.

As part of the agreement, XYZ Bank may require Sarah to maintain the property until the transfer of ownership is complete. Additionally, the bank may still report the debt forgiveness to the IRS, which could result in tax consequences for Sarah.

In this example, the deed in lieu of a foreclosure agreement provides a mutually beneficial solution for Sarah and XYZ Bank. As a result, Sarah can avoid the negative consequences of foreclosure on her credit report and financial stability. At the same time, XYZ Bank can recoup some of its losses on the defaulted loan without resorting to costly and time-consuming foreclosure proceedings.

Tax Consequences

A deed in lieu of foreclosure may have tax consequences for the borrower, as the debt forgiveness by the lender could be treated as taxable income by the IRS. The forgiven debt is generally considered income and reported to the IRS on Form 1099-C by the lender. Thus it means that the borrower may be required to pay income tax on the amount of debt forgiven, which could result in a higher tax bill for the borrower.

However, under certain circumstances, borrowers may be able to exclude the forgiven debt from their taxable income. For example, the Mortgage Forgiveness Debt Relief Act of 2007 allowed taxpayers to exclude up to $2 million of the forgiven debt on their primary residence from taxable income. Still, this law expired at the end of 2020.

Borrowers need to consult with a tax professional to determine the potential tax consequences of a deed in lieu of foreclosure and to explore any available options to minimize the tax impact.

Advantages And Disadvantages

Deed in lieu of foreclosure can have advantages and disadvantages for borrowers and lenders.

Advantages For Borrowers

- Avoidance of foreclosure and the negative consequences on credit score and financial stability.

- Faster resolution of the defaulted loan compared to a foreclosure.

- Potential for a more favorable outcome on the borrower’s credit report.

Disadvantages For Borrowers

- Potential tax consequences due to debt forgiveness.

- Possible negative impact on credit score, though it’s generally less severe than a foreclosure.

- May be required to meet certain conditions, such as maintaining the property or paying outstanding liens or taxes, before completing the agreement.

Advantages For Lenders

- Quicker and less expensive resolution of defaulted loans compared to a foreclosure.

- Avoidance of legal complexities associated with foreclosure proceedings.

- Possibility of recouping some of the losses on the defaulted loan.

Disadvantages For Lenders

- Possible reduction in the amount of the outstanding debt due to debt forgiveness.

- Risk of taking on a property with unknown defects or liens.

- Potential for legal challenges by borrowers who feel they were not treated fairly in the agreement.

Deed In Lieu Of Foreclosure vs Short Sale

| Feature | Deed in Lieu of Foreclosure | Short Sale |

|---|---|---|

| Definition | The borrower voluntarily gives up ownership of the property to the lender in exchange for forgiveness of the outstanding debt. | The borrower sells the property for less than the outstanding debt, and the lender agrees to accept the proceeds as the satisfaction of the debt. |

| Effect on Credit Score | The negative impact, but generally less severe than foreclosure. | The negative impact, but generally less severe than foreclosure. |

| Process | Initiated by the borrower who contacts the lender to express their interest. | Initiated by the borrower who lists the property for sale, and the lender agrees to accept the proceeds as the satisfaction of the debt. |

| Time to Complete | Quicker than foreclosure but may take several weeks to several months to complete. | Longer than deed in lieu of foreclosure, typically takes several months to complete. |

| Tax Consequences | Forgiveness of debt may be treated as taxable income by the IRS. | Forgiveness of debt may be treated as taxable income by the IRS. |

| Possibility of Deficiency Judgment | The lender may still pursue a deficiency judgment against the borrower for any remaining balance owed after the sale. | The lender may still pursue a deficiency judgment against the borrower for any remaining balance owed after the sale. |

| Relinquishing Property | The borrower voluntarily gives up ownership of the property to the lender. | The borrower sells the property to a third party. |

Frequently Asked Questions (FAQs)

1. What is a deed in lieu of foreclosure for the deceased?

In the case of a deceased homeowner, a deed in lieu of foreclosure may be an option for the estate to avoid foreclosure and potentially reduce the financial burden on the estate.

2. What is a deed in lieu of foreclosure consequences?

The consequences of a deed in lieu of foreclosure can include multiple implications due to debt forgiveness, the potential impact on credit score, and possible conditions that must be met before completing the agreement.

3. Does a deed in lieu of foreclosure affect credit?

Yes, a deed in lieu of foreclosure can harm the borrower’s credit score. The extent of the impact on the credit score may depend on various factors, such as the borrower’s credit history and the lender’s reporting practices. However, the negative impact is typically less severe than that of foreclosure.

Recommended Articles

This article has been a guide to what is Deed in Lieu of Foreclosure. We compare it with short sale, its tax consequences, examples, advantages, & disadvantages. You may also find some useful articles here –