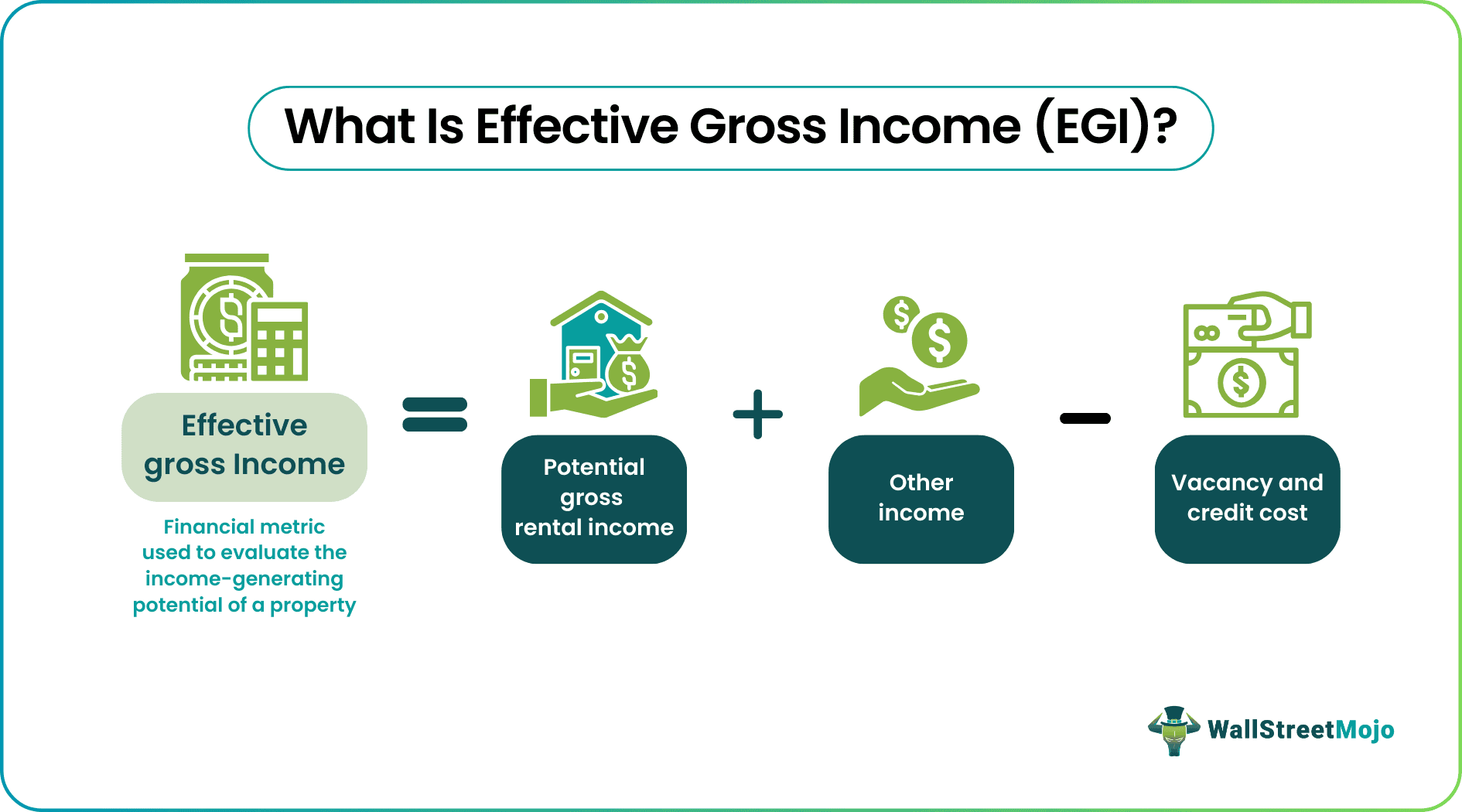

What Is Effective Gross Income (EGI)?

The Effective Gross Income (EGI) in real estate is an important metric that helps homeowners and prospective buyers analyze the net cash flows from renting the house. It is because, apart from the rental income, homeowners should consider other revenue sources and expenses for a complete picture of profitability.

Other income streams are added to the gross potential rental income, while other expenses are deducted. The homeowner should lease the house only if the cash flow is positive and large enough. It reflects the return on investment from purchasing or holding the asset.

- The effective gross income in real estate can be defined as an evaluation metric to analyze the cash flows from leasing a property.

- It is a more realistic measure that considers additional non-recurring, variable income and other expenses, such as allowances and provisions incurred by a homeowner.

- It is essential to note that operating expenses are not deducted from the gross potential rental income.

- It can help homeowners and homebuyers decide and indicate the appropriate amount of rental income to collect from tenants.

Effective Gross Income Explained

The effective gross income of the property is a financial parameter that homeowners and prospective investors calculate as part of decision-making. It is easy to randomly state a value as rental income and compute how much a homeowner will make in a year. Nevertheless, primarily, the homeowner will get a different amount.

If a person estimates a random rental income, they base their expectations, forecasts, and expenses on that amount. In reality, many factors affect a homeowner’s gross rental income. These factors can be positive, thus increasing the rental income, or they can be negative and decrease the rental income.

When these factors act, the homeowner’s net cash flow is affected. However, homeowners should only approve the EGI if it is significantly positive. It will ensure that they do not incur any losses, pay for operating expenses, and set aside a sufficient amount as reserves or provisions.

Homeowners can also decide the appropriate rental income they should demand through EGI calculations. Suppose the person can approximately estimate their other income, operating expenses, and other expenses (such as provisions). In that case, they can pre-determine an amount of EGI and decide their monthly or annual rental income accordingly. Nevertheless, the value should also consider location, amenities, accessibility, and other factors.

Formula

Let’s understand how to calculate effective gross income of the property by using the following formula:

EGI = Gross Potential Rental Income + Other Income – Vacancy Cost – Bad Debts

- Gross potential rental income would be the maximum income from leasing a property if it were occupied throughout the year and never vacant. It also considers the situation where the tenant would pay the total rent on time.

- Other income refers to the revenue a homeowner receives apart from the rent. These sources need not be recurring, or only some tenants will pay them, as they do not require these services. Examples include maintenance fees, laundry charges, storage units, pet fees, etc.

- Vacancy cost is the loss incurred by a homeowner due to a vacant unit. Even if they do not receive any income from an unoccupied unit, they will have to incur some expenses toward that unit, such as maintenance, repairs, etc., resulting in a net loss.

- Bad debts or credit costs refer to the condition where a tenant in an occupied unit fails to make a rent payment or does not make full payment. It is again a loss for the homeowner, as they would be undertaking expenses toward the unit anyway.

- The vacancy and credit costs are based on historical data and forecasts. The homeowner usually creates a provision for these expenses.

Examples

Let’s discuss a few examples to understand EGI.

Example #1

Let’s consider an example to calculate the EGI for the year 2022 in a real estate scenario.

Monthly gross potential rental income = $3000

Monthly maintenance charges = $200

Pet charges = $50 per month

Annual provision for bad debts = $5000

The annual allowance for vacancy cost = $5000

We can determine the Annual EGI by calculating the annual figures and applying the EGI formula. To calculate the EGI for 2022.

First, let’s find the annual figures:

Gross potential rental income = $36,000

Other income = $3000

Other expenses = $10,000

EGI = Gross potential rental income + Other income – Other expenses

= $36,000 + $3000 – $10,000

Annual EGI = $29,000

Example #2

Suppose Ken is an investor looking for a low-risk, high-worth asset. His friend advises him to buy a house and lease it. After some research, Ken finds a home in Brooklyn and a duplex apartment in Manhattan. Here are the details regarding the two investments. Which one should Ken go for if the upfront investment is not an issue for him?

| Basis | Brooklyn House | Manhattan Apartment |

|---|---|---|

| Price | $800,000 | $1,500,000 |

| Tenants | 1 | 2 |

| EGI | $100,000 | $250,000 |

| EGI: Price ratio | 12.5% | 16.67% |

Considering the EGI: Price ratio, the Manhattan apartment seems a good option. But it is important to note that many other factors must be considered. Ken should choose the Manhattan apartment if his decision is solely based on this information.

Effective Gross Income vs Potential Gross Income vs Net Operating Income

Understanding the differences between EGI, Potential Gross Income (PGI), and Net Operating Income (NOI) is essential in real estate. These metrics play distinct roles in analyzing and evaluating a property’s financial performance.

Let us understand them.

| Basis | Effective Gross Income (EGI) | Potential Gross Income (PGI) | Net Operating Income (NOI) |

|---|---|---|---|

| Definition | The income generated after accounting for non-recurring expenses and vacancy losses. | The total income a property can generate if fully leased. | It is the profitability of a property after deducting operating expenses. |

| Purpose | Reflects the actual cash flow potential of the property, accounting for various expenses. | Represents the maximum income the property can generate if fully occupied. | Reflects the profitability of the property after considering operational costs. |

| Treatment of Financing Costs | It does not consider financing costs. | It does not consider financing costs. | It deducts financing costs from EGI. |

Frequently Asked Questions (FAQs)

1. What is an effective gross income multiplier?

The EGI multiplier is a measure of the value of a real estate asset. It is calculated by dividing the asset’s selling price by the EGI value. This parameter is of specific importance to prospective home buyers who plan to lease the property after purchase. It will also help them to decide if the asset’s selling price is accurate or overrated.

2. What is monthly effective gross income?

Monthly EGI is calculated by dividing the annual EGI by 12 (full months in a year). It can be done when specific figures are specified annually and some monthly. For instance, rental income may be collected monthly, but provisions for credit or vacancy costs will be established annually.

3. What is the ratio of operating expenses to effective gross income?

Operating expenses divided by gross operating income will give the operating expense ratio (OER). The EGI can be used as the gross operating income, as both are the same.

Recommended Articles

This article has been a guide to What Is Effective Gross Income. We explain its formula, comparison with potential gross and net operating income, and examples. You may also find some useful articles here –