Part of our Real Estate Investing guide

What Is FFO (Funds From Operations)?

FFO (Funds from Operations) usually refers to the cash flows generated by Real Estate Investment Trusts (REITs) and is calculated by subtracting Interest income and gain on the sale of assets from the net income during the period and adding the Interest expense, depreciation, and Losses on the sale of assets to it.

FFO is used to measure the cash flow from operations. Thus, it is similar to ‘Cash Flow from Operations.’ However, it is generally used in reference to cash flows generated by ‘Real Estate Investment Trust’ (REIT). Even Though FFO is widely considered for determining REIT’s profitability; it can often be susceptible to accounting changes, restatements, and manipulation.

FFO (Funds From Operations) Explained

Funds from operations concept are required for the analysis of a REIT because when the underlying assets increase in value, then depreciation should not be factored into the results of operations. It is considered to be a better indicator of the financial results of a business than net income; however, since the accounting chicanery can impact a variety of aspects of the financial statements, it is always better to rely upon a mix of measurements rather than a single measure while making investment decisions.

- For Real estate companies, FFO meaning in finance states that it is used as a performance benchmark as real estate values are proven to fluctuate with macroeconomic conditions, and using the cost accounting examples to compute the financial conditions do not usually serve as an accurate measurement of performance.

- It includes funds generated from business operations, excluding financing-related cash flows, such as interest income or interest expense. It does not include any depreciation or amortization of fixed assets or gains or losses from the disposition of assets.

- Real Estate Investment Trusts (REITs) is a business that primarily operates on income generated from real estate transactions. Such REIT companies are involved in commercial real estate. It includes selling, leasing, and financing offices and buildings, warehouses, hospitals, shopping centers, hotels, etc. Such companies commonly use FFO.

Formula

The formula commonly used in the calculation of the same are given below. Let us try to interpret it and understand the FFO meaning in finance.

All the factors used while calculating the Funds from operations can be found in the company’s income statement. These factors include net income, depreciation, amortization, and gains on sales of property andextraordinary items.

FFO Formula = Net Income + Depreciation and Amortization of Real Estate Assets – Gains (losses) on Asset Sale + Losses (Gains) on Restructuring Debt or Extraordinary Items

Example

Let us understand the concept with the help of a suitable funds from operations example.

- Identify the Net Income from the Income Statement

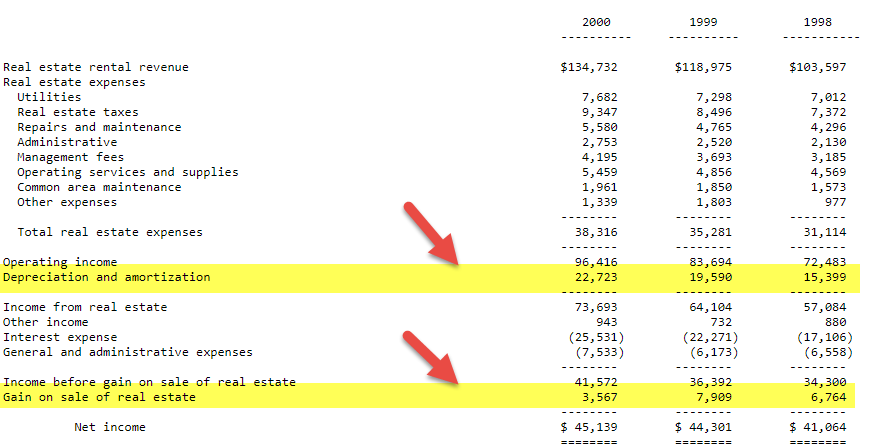

We note above that the net income of Washington REIT for 2000 is $45,139. Likewise, its net income for 1999 and 1998 is $44,301 and $41,064, respectively.(please note the figures are in thousands)

- Identify Depreciation and Amortization of Real Estate Assets

It is part of the Income Statement.Depreciation and Amortization (2000) = $22,723Depreciation and Amortization (1999) = $19,590Depreciation and Amortization (1998) = $15,339

- Identify Gains (Losses) on Sales of Assets

This figure is also part of the income statement.Gains on Sales of Assets (2000) = $3,567Gains on Sales of Assets (1999) = $7,909Gains on Sales of Assets (1998) = $6,764

- Identify Gains (Losses) on Restructuring Items or Extraordinary Items

There are no gains (losses) on restructuring expenses or extraordinary items in these three years.

- Apply Formula

FFO Formula = Net Income + Depreciation and Amortization of Real Estate Assets – Gains (losses) on Asset Sale + Losses (Gains) on Restructuring Debt or Extraordinary ItemsFFO (2000) = $45,139 + $22,723 – $3,567 = $64,295FFO (1999) = $44,301 + $19,590 – $7,909 = $55,982FFO (1998) = $41,064 + 0$15,339 – $6,764 = $49,699

From the above funds from operations example, we et a clear understanding of the metric and how exactly it is used along with a step by step guidance of the calculation process.

Adjusted FFO

Adjusted funds from operations (AFFO) are calculated after making adjustments to net income and are intended to compensate for accounting methods. These methods might distort a real estate investment trust’s true performance. The calculation for AFFO subtracts from FFO any recurring expenditures that have been capitalized, such as projects for building improvements.

Generally Accepted Accounting Principles (GAAP) require depreciating the investment properties over time. However, real estate appreciates over time. For this reason, the required depreciation expense, which is charged as per GAAP, tends to make the net income appear artificially low.

FFO also adjusts for non- recurring items as they do not occur in regular business scenarios. For instance, gains (or losses) on the sale of properties are to be removed/ added accordingly, as they are not like regular business operations and therefore do not contribute to the REIT’s ongoing dividend-paying capacity. In addition, some analysts further consider rent increases and certain Capex for calculating adjusted Funds from operations (AFFO).

FFO per share is used as a carefully scrutinized metric to gauge a REIT’s profitability per unit of shareholder ownership. Funds From Operations is further used as general valuation multiple and P/E multiples. Thus it is a key driver of share prices as well.

Why Is FFO Important For Real Estate?

- While equity investors give importance to metrics like earnings per share EPS or a price-earnings ratio (P/E) while analyzing stocks, REIT investors decide based on FFO.

- Before investing in a REIT, be sure of the price; the decision is not based solely on FFO or AFFO as the investment which looks good on the surface may not turn out to be a good decision in the future as the prices may decline due to too many investors buying it.

- Compared to conventional stocks, the earnings per share (EPS) for a REIT will be naturally low or even negative. Thus, the price-to-earnings (P/E ratio) of a REIT is not a good multiple, while making investment decisions should be considered a distant second metric when evaluating it

Thus, the above points clearly justify why this financial metric is widely used in the real estate market and investors depend on it for property value assessment. However, it is not full proof since it does have the limitations related to manipulation, under or over statement of value along with sudden policy changes.

FFO Vs CFO

Both the above terms are very commonly used in the financial market for fundamental analysis of stock or any other type of asset. However, there are some differences between them. Let us try to point them out.

- As the name suggests, cash flow calculates the total amount of cash and cash equivalents generated from the operations of a business. However, FFO is a more important measure for the real estate business as these measures compensate for one important component, which is depreciation.

- For the real estate business, the value of properties always increases over time; thus, this isn’t an expense at all. As per IRS, when businesses own long-term assets such as equipment, computers, and buildings, these assets have to be depreciated to reflect the current financial position.

- However, when it comes to real estate, these properties don’t have a “shelf life” or, in other words, would never depreciate to a minimal value over the period. On the contrary, these assets would appreciate and, therefore, not count as an expense to be charged to the income statement.

- Thus operating cash flow and FFO are similar metrics. However, they’re not quite the same thing. Cash flow can be a great way to evaluate financial well-being. Still, when it comes to the real estate industry, the metrics differ from the regular business scenario.

- To assess whether a REIT is earning enough to cover its dividends, FFO is the way to go. It helps in getting a better picture than a regular CFO would.

Recommended Articles

This has been a guide to what is Funds From Operations (FFO). We explain it with example, differences with cash from operation(CFO), formula & adjusted FFO. You may learn more about cash Flows from the following articles –