Table Of Contents

What Is Mutual Company?

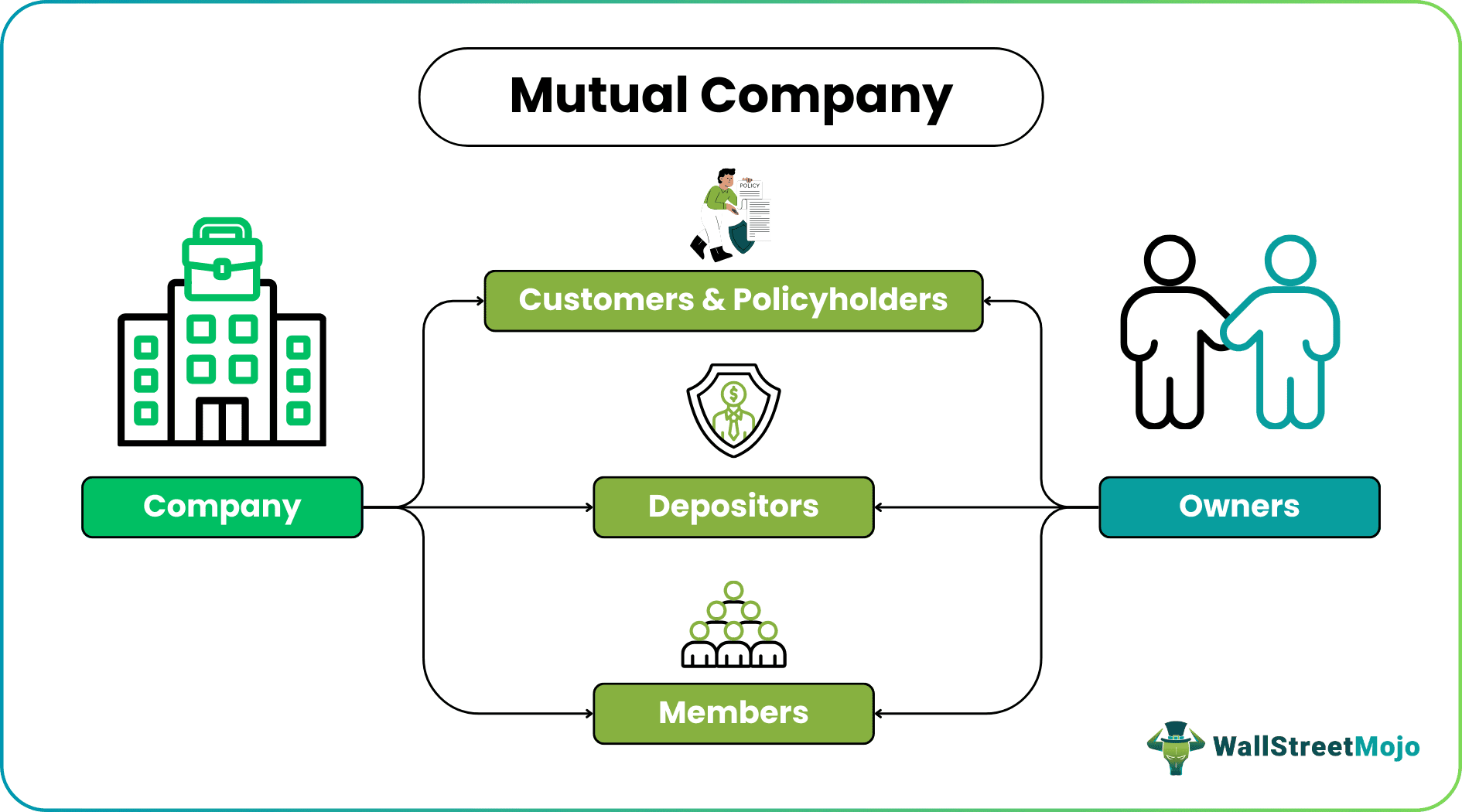

A Mutual Company is an organization where depositors, customers, and policyholders hold ownership rights. Therefore, there is no single owner, and everyone is entitled to receive a share in the profits generated by the business based on their ownership participation. Such companies have a structure that differs from typical companies or firms in various sectors.

Usually, insurance companies and certain financial services institutions follow this structure. Different countries adopt this structure for different reasons. For instance, in Canada, insurance companies are typically built or designed to comply with the mutual company definition. Since customers are company owners, they accept the risk involved in operating it and are thus entitled to profits.

Table of contents

- What Is Mutual Company?

- A mutual company is owned by its members, customers, policyholders, and depositors. They are entitled to share the profits a company makes.

- Typically, these companies operate in the insurance industry. Also, many credit unions, insurance firms, and banking trusts in Canada and the US follow the mutual company structure.

- A mutual company can be converted to a stock company by issuing shares for capital sourcing.

- Cooperative companies differ in many ways from these companies as their ownership rights, structure, and objectives, among other things, are different.

How Does A Mutual Company Work?

A mutual company is a legal entity where ownership is shared between its members, depositors, and policyholders. Such companies are typically seen in the insurance industry. They have a different corporate structure than other privately held or publicly traded companies. Customers benefit from the company's performance—the more they invest, the higher their profit share and dividend payout.

The mutual company definition states that it operates on a pro-rata basis. Therefore, customers and members receive low dividends when profits are down. Simply put, they share operational or business risks as they have a say in operations. Not all insurance firms are mutual companies. Companies operating in a specific field or delivering expert services in a particular field have a single goal. Hence, they focus on certain areas. As they specialize in a fixed domain or area, they are suited to operate as mutual companies.

When we discuss the mutual company meaning, it includes covering certain salient characteristics. One of the noteworthy features is that such companies focus on policyholders, follow transparent underwriting procedures, and offer a long-term commitment to members to provide top-notch insurance services. However, these companies have limited access to capital since no other funding sources are employed. Retained earnings form a major source of their income, in addition to the premiums they receive from policyholders.

Such companies may consider demutualization, which refers to a mutual company becoming a joint stock company by raising funds from other sources. If external funding or investor money is pumped into such a company, it can be converted into a stock company in certain situations.

Financial institutions, credit unions, mutual healthcare providers, banking trusts, cooperative banks, and societies are some common examples of mutual companies. Such entities have no external shareholders and do not typically intend to expand, accumulate, or maximize their capital gains.

Examples

Given below are two examples to take this discussion ahead.

Example #1

Suppose ABC & Co, an insurance company, operating as a mutual company, accumulates funds from its members and policyholders. In exchange, it offers life insurance and a package of shared services to everyone associated with the company. The company's members have the right to make decisions and share profits from company operations. In this way, the company operates as an entity specializing in insurance, shares profits, and delivers excellent services to its members.

Example #2

Frankenmuth Insurance, a US-based insurance company, became a mutual company in January 2023. The conversion gave birth to a new mutual holding company called Frankenmuth Mutual Holding Company.

The erstwhile Frankenmuth Mutual Insurance Company, an entity operating as an insurance service provider under the umbrella of the holding company, became a wholly owned stock subsidiary of Frankenmuth Holdings, Inc. Under the new regime, it is called Frankenmuth Insurance Company.

Per the new structure, Frankenmuth Insurance Company’s members and policyholders have ownership rights. In terms of business operations, no material changes occurred. Also, the conversion did not affect or modify the terms of the agreement between the company and its stakeholders. Fred Edmond, President and CEO of Frankenmuth Insurance, stated that this structural conversion gave the company great opportunities to raise capital.

Benefits

The benefits of such companies are:

- Customers and policyholders are company owners. Hence, their monetary interests are prioritized.

- Mutual companies pay dividends to their members and share profits. This generates goodwill in the specific industry or sector.

- Company performance is a key parameter here. The profit-sharing system follows a pro-rata distribution pattern in terms of the revenue (and subsequently profits) the company generates. Hence, a fair profit distribution is possible.

- These companies have a long-term vision, aim for corporate stability, and follow sound procedures for strategic decision-making.

- These companies are customer- and member-centric. Hence, they are focused on delivering excellent products and services.

Mutual Company vs Stock Company

The key differences between a mutual company and a stock company are:

- It is owned by its policyholders, but a stock company is privately or publicly listed.

- Mutual companies collect money from customers. In contrast, stock companies raise capital through investors.

- Customers and depositors are responsible for the smooth functioning and growth of a mutual company, but stock companies are businesses run by the joint efforts of various stakeholders. For instance, the board of directors steers the business while several teams supervise operations.

- The members enjoy dividends from corporate profits, but stock companies have outside investors. Hence, shareholders or investors receive dividends. Policyholders are not issued dividends.

Mutual Company vs Cooperative Company

The key differences between a mutual company and a cooperative company are:

- Members of a such company have ownership rights. In a cooperative company, ownership rights depend on the establishment type. For example, in certain cooperative companies, suppliers and producers can become members of the cooperative establishment.

- The policyholders in such companies receive dividends. On the other hand, cooperative companies are formed for equitable distribution of goods and services. Hence, their focus is on negotiating for the fair distribution of goods and services among various entities or groups in society.

- Mutual companies do not usually operate in the manufacturing sector. In contrast, cooperative companies can include entities from various sectors, including agriculture, banking, manufacturing, etc.

- The governance in mutual companies extends only to the members. However, most cooperative companies assign equal voting rights to participants or members.

Frequently Asked Questions (FAQs)

These companies are formed for the following reasons:

- To leverage the skills and expertise of members in a specific area and protect their professional and financial interests.

- To ensure sufficient funds are available and the company functions smoothly.

- To issue dividends to members from time to time on a pro-rata basis.

The disadvantages are:

- The capital-raising capacity of such companies is limited. Also, funds are managed in a set or fixed manner, as no external entity participates in decision-making.

- The risks of operating are higher. Such risks are borne by customers and members.

- As the corporate structure is different, work processes and performance cannot be measured against the general standards or benchmarks in the industry.

Typically, mutual companies are private entities. But if a company undergoes demutualization, it can opt for becoming a public company and changing its structure. In such cases, its members receive ownership conversion rights or compensation (in the transition), mostly in the form of shares.

Recommended Articles

This article has been a guide to What is Mutual Company. Here, we compare it with stock company and cooperative company, explain its examples, and benefits. You may also find some useful articles here -