Underwriting Meaning

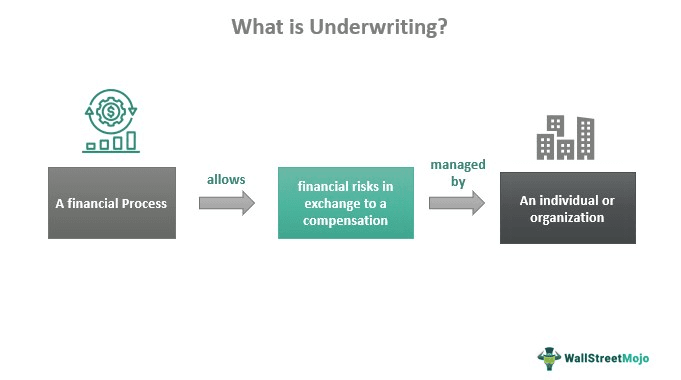

Underwriting is a procedure that allows a person or organization to accept financial risk in exchange for compensation. Its purpose is to estimate the degree of risk associated and set the prices accordingly at which the contract can be offered.

The underwriting process serves a crucial role in the financial sector due to its contribution to establishing reasonable premiums, affordable borrowing costs for credit, and the development of a marketplace for securities through the precise pricing of investment risk. As a result, a wide range of industries, including the insurance industry, the banking industry, and the stock market, use this procedure.

- Underwriting is the process by which an organization or investor assesses, investigates, and calculates an investment risk.

- An underwriter’s job is to assess the costs, interest rates, and regulations associated with a credit or transaction.

- Underwriting risk refers to the likelihood that the premiums paid by insurers won’t be sufficient to cover the expenses that the insurance company would be liable for if the disaster or catastrophe covered by the policy happens.

- Initial public offerings are when this process is employed the most frequently. It is because an underwriter who owns a substantial amount of a company’s stock provides the commodities with essential finance, improving financial sustainability.

Underwriting Process Explained

Underwriting indicates that the lenders confirm the borrower’s revenue, possessions, debts, and public records before approving the loan. Then, a financial specialist known as an underwriter examines the accounts and determines the level of risk a lender is willing to tolerate in exchange for a loan.

Under the insurance sector, underwriters decide how much an insurance company should take on covering a customer. They assess customer threat and exposure, as well as the amount of coverage that should be provided, the amount that should be paid for it, and if they should give the customer an insurance policy.

The most frequent times when manual underwriting is used are during the initial public offerings. It is because an underwriter who maintains a sizable portion of shares of a company is providing fundamental financing for the commodity, which improves economic stability.

Underwriters perform the crucial task of assessing a prospective user’s credit scores and deciding whether it is appropriate to provide credit. They evaluate the client’s credit history based on various factors, including their previous financial background, accounts, and the value of any offered securities.

What is Underwriting of Securities? Explained in Video

Factors

An underwriter assesses the following three fundamental factors:

#1 Revenue

Income is crucial in determining if a borrower’s earnings can afford the loan’s monthly repayments. The overall revenue is the sum of both net and gross income. Therefore, the borrower must submit the balance sheets, financial statements, and individual and commercial tax documents pertinent to the loan’s objective.

#2 Inspection

Inspections confirm the asset’s value or any other purpose for the loan. In this procedure step, an evaluator either examines the business or assesses the loan’s aim to gather essential decisive data, such as profitability or investment potential.

#3 Credit score

The borrower’s ability to make timely payments on credit, particularly credit cards and loans, can be ascertained by looking at their credit score. A lender’s debt-to-income (DTI) proportion, provided by their credit score, can be used to determine whether they have enough money to repay this loan and any other loans they may have. A cheaper interest rate may be available to borrowers with solid credit.

Types

There are several methods of manual underwriting, but the following are the most frequently employed for risk assessment:

#1 Loan underwriting

Risks associated with providing money to prospective borrowers are assessed and calculated throughout the loan underwriting process. Three primary factors—income, valuation, and credit score —are used by loan underwriters to determine whether a loan will be repaid.

The loan underwriting process frequently relates to a mortgage. A borrower’s history and the asset they request a loan for are evaluated during property investment. If the borrower cannot repay the loan, whether the property will be able to regain its worth will be determined during the underwriting agreement procedure.

#2 Insurance Underwriting

A potential insurance applicant is evaluated for existence, healthcare, welfare, properties, leasing, or other types of coverage. The likelihood of making significant or recurrent claims is assessed, together with the amount of coverage that can be provided, the amount that should be paid, and the likelihood that an insurance provider will make a payment to compensate the insured.

Gender, profession, healthcare, medical history, family history, lifestyles, pastimes, and other characteristics are considered part of the life insurance screening process to determine the risks of the prospective insurer. Health-related considerations or pre-existing diseases may result in restrictions on health insurance. A policy’s coverage is determined by evaluating factors such as accident propensity, possible damage, and environmental effects.

#3 Stock Market Underwriting

An investor locates lucrative assets offered by a firm conducting an initial public offering (IPO), and the buyer subsequently offers those stocks and bonds for a gain. A group of underwriters will purchase the assets to sell stocks to distributors or investors. The term “underwriting spread” refers to the profit this group receives from a disparity.

Examples

Let us understand the concept of underwriting better with the help of examples.

Example #1

Catherine lives in a house and is situated on a recognized floodplain. Every 10 to 15 years, homes in the area experience severe flooding. As a result, Cameron has struggled to find home insurance coverage. Finally, one insurance provider consents to look into it.

Excluding the flood risk, the firm’s underwriter finds that Cameron’s home complies with their loan underwriting process requirements. However, the underwriter wants Cameron’s company, so she agrees she would issue Cameron an owner’s insurance policy. Still, she will add an endorsement that levies a $10,000 penalty for flood-related complaints.

Example #2

After significant losses and controversies, Credit Suisse will shortly disclose what is anticipated to be a substantial reform. The Zurich-based financial institution is preparing arrangements should that become required but would prefer to keep new shares at the present low values. The institution will transfer assets that it intends to unwind.

Credit Suisse is also considering creating a new division out of its consulting teams and stretched finance business, possibly operating under the revitalized first Boston name and seeking outside funding.

Underwriting Risk

It refers to the possibility that more than the payments made by insurers will be needed to satisfy the demands that the insurance provider will be responsible for paying in the instance that the incident or catastrophe protected against occurs. This risk may include undervalued policies currently being used, miscalculated debts resulting from abandoned contracts issued in prior years, or lapsed policies.

An incorrect assessment of the risks associated with creating an insurance policy may occasionally result in underwriting agreement problems. The insurance could also cost the insurer more than it made in premiums due to circumstances far beyond the underwriter‘s influence.

It should be noted that the amount that the policyholder pays goes toward more than administrative expenses. It must also include protection against any claims the insured might make. In addition, it must consist of a management fee equal to the profitability as measured by the insurance share capital of the company, which is meant to protect the insurer from unpredictability.

Underwriting vs Origination

Specialists in the finance industry include both loan originators and underwriters. Assisting borrowers in obtaining credit and lenders in ensuring that credits are disbursed are the roles of these two groups. These two roles are not identical but differ in several significant ways. Let’s see how they contrast with one another based on similar criteria.

| Comparison | Underwriting | Origination |

| Definition | Financial institutions assess a credit application and determine the risk level of the credit by charging an additional fee. | Lenders levy an up-front cost called an origination fee for screening. It represents a portion of the amount borrowed. |

| Roles | Underwriters examine mortgage applications to ascertain whether the client qualifies for the credit. | Loan originators guide potential borrowers as they select financing that best suits their requirements and helps them comprehend their alternatives. |

| Work environment | The majority of time underwriters spend at their desks analyzing applications is spent working in an office setting. | Based on the kind of organization they work for, loan originators operate in various settings. |

Frequently Asked Questions (FAQs)

1.Can underwriting deny loans?

Because there is insufficient information to support an application, an underwriter may reject a loan application. An explanation letter with a valid explanation and proof may assist the underwriter in comprehending a sizable bank deposit in the accounts, explaining job interruptions or a liability paid off by another party.

2.Is underwriting a good career?

Anyone interested in working in the banking or insurance industries might consider a career in underwriting. Underwriters sometimes earn a good income with possibilities for career advancement.

3.What happens when a mortgage goes to underwriting?

The creditor evaluates the debtor’s dependability and determines whether or not the application satisfies the requirements for the loan throughout the underwriting process. As a result, a few hours or weeks may pass before a loan is approved.

4.Are underwriting fees tax deductible?

Even if the seller pays them, loan origination expenses may still be written off. These are the costs that bankers want to execute and underwrite a mortgage.

Recommended Articles

This has been a guide to Underwriting and its meaning. Here, we explain its types, factors, risks, examples, and comparison with origination. You can learn more about it from the following articles –