CPA Exam REG Section

REG CPA Exam (Regulation) exam section tests a candidate’s competency in applying the concepts of federal taxation, business law, and ethics. It is a four-hour exam with 15 minutes break.

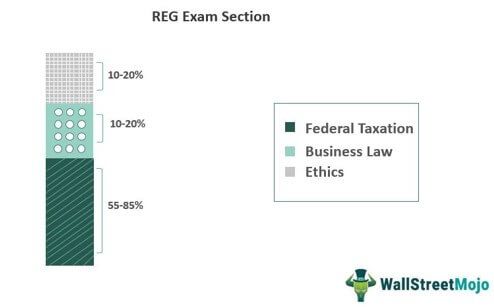

In the REG exam section, the main focus is on federal taxation. Federal taxation accounts for more than 50% of the exam questions. So, prepare this area with the utmost dedication. Emphasize memorizing, understanding, and applying all the concepts of taxation.

REG Pass Rates

- The average percentage of students passing in the REG section is around 50%. In the last few years, the lowest recorded pass rate was around 44%. However, over the years, the pass rates have shown a remarkable upward trend, especially since 2018.

- Since the past three years, this section has witnessed significant growth in pass rates, from 47% in 2017 to 62% in 2020. The second quarter of 2020 recorded the highest pass rate of around 76%.

- Despite being a challenging exam, REG has emerged as the second-best performing section in the recent times. In the first quarter of the 2021, the REG pass rate stood at 59.29%.

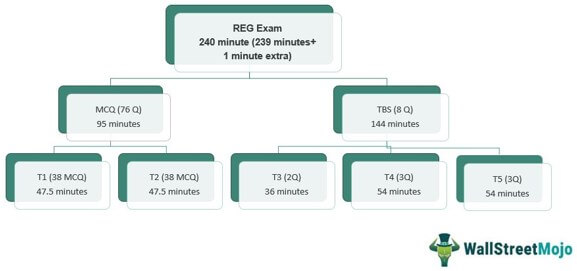

CPA REG Exam Format

The REG section comprises five small blocks or sections called testlets, with two types of questions:

- Multiple-choice question (MCQ) – 2 testlets

- Task-based simulations (TBS) – 3 testlets

Each MCQ testlet contains 38 questions. One testlet from TBS contains two questions, and the other two include three questions each. The overall weightage of these two segments is equal. In the following image, T stands for testlet, and Q stands for questions.

A candidate needs to have an exhaustive understanding of the subjects and excellent time management skills to finish on time and perform well in this section.

CPA REG Testing Process

A candidate has to take five testlets consecutively (2 MCQs and 3 TBSs) in the REG exam section. The AICPA labels the MCQ testlets as either ‘difficult’ or ‘medium,’ depending on their difficulty levels.

#1 – MCQ Testing Process

AICPA uses a multistage adaptive test delivery model for the MCQ testlets. The first testlet is of the same difficulty for all the candidates. On the other hand, the second testlet is based on their performance in the first testlet.

The candidates with a weaker performance in the first testlet get a medium-level second testlet, whereas the candidates who perform well get a difficult testlet.

Please note that scores for each question are factored in based on the difficulty of that particular question. A medium testlet doesn’t ensure better scores.

#2 – TBS Testing Process

The TBS testlets are common for all the candidates. The candidates get the TBS testlets after completing the second MCQ testlet. Once submitted, candidates cannot retake a testlet.

The scores of individual sections (MCQs & TBSs) are scaled and weighted according to the AICPA’s policy such as the answer to the question being correct and its relative difficulty. For more details related to grading, check the section below.

CPA REG Question Types

There are two types of questions in the REG section.

#1 – Multiple-Choice Questions (MCQ)

The multiple-choice questions present multiple answer options, and the candidates have to select the correct one. They appear in the first two testlets of the REG section.

#2 – Task-Based Simulations (TBS)

Task-based simulations are real-life case study questions that test candidates’ ability to apply the principles and concepts learned. They appear in the last three testlets of the REG section.

All questions in this section (MCQ and TBS) are either pretest or operational.

- Operational Questions – The operational questions are the ones that contribute to a candidate’s overall score. There are 64 operational questions in MCQ and seven in TBS.

- Pretest Questions – Pretest questions are not scored. The AICPA puts them in the exam to see their viability in future exams. These pretest questions are likely to be seen in the forthcoming exams. There are 12 pretest questions in MCQ and one in TBS sections.

Keep in mind that a candidate cannot identify such classification in the exam, so it is advised not to ponder it too much.

How is CPA REG Graded?

- On a scale of 0 to 99, a candidate must score a minimum of 75 to pass the REG exam section. Both the MCQ and TBS sections contribute 50% each to the final score. The overall score of the REG section is a weighted combination of scaled scores of all testlets (MCQ and TBS).

- MCQs carry weightage according to their difficulty. A candidate performing well in the first testlet might face a difficult testlet in the next round. A difficult testlet implies that the questions would be carrying a higher weightage than the others. This is where a candidate can increase the overall score.

- AICPA does not score TBSs according to their difficulty. Please note that there is no negative scoring. So, please make sure to attempt all questions.

CPA REG Exam Content

To help you understand better, we have put together some of the Acts that form a crucial part of the REG section:

- Uniform Accountancy Act

- Uniform Commercial Code

- Treasury Regulations

- Internal Revenue Code of 1986, as amended

- Treasury Department Circular 230

- Public Law 86-272

- Uniform Division of Income for Tax Purposes Act (UDITPA)

The AICPA divides the entire syllabus into areas, groups, and topics. Each section has a separate weightage. As per AICPA CPA Exam Blueprint, below is a table briefly describing the syllabus for REG Section. From the following break-up of the content, it is evident that federal taxation forms a significant portion of the REG section.

| S.No. | Content Group | Topics | Weightage |

|---|---|---|---|

| 1. | Ethics, Professional Responsibilities, and Federal Tax Procedures | 1. Ethics and responsibilities in tax practice • Regulations governing practice before the IRS • Internal Revenue Code and regulations related to tax return preparers 2. Licensing and disciplinary systems 3. Federal tax procedures • Audits, appeals, and judicial process • Substantiation and disclosure of tax positions • Taxpayer penalties • Authoritative hierarchy 4. Legal duties and responsibilities • Common law duties and liabilities to clients and third parties • Privileged communications, confidentiality, and privacy acts | 10-20% |

| 2. | Business Law | 1. Agency • Authority of agents and principles • Duties and liabilities of agents and principles 2. Contracts • Formation • Performance • Discharge, breach, and remedies 3. Debtor-creditor relationships 4. Federal laws and regulations 5. Business structure • Selection and formation of business entity and related operation and termination • Rights, duties, legal obligations and authority of owners and management | 10-20% |

| 3. | Federal Taxation of Property Transactions | 1. Acquisition and disposition of assets • Basis and holding period of assets • Taxable and nontaxable disposition • Amount & character of gains and losses, and netting process (including installment sale) • Related party transactions (including imputed interest) • Cost recovery (depreciation, depletion, amortization) • Gift taxation | 12-22% |

| 4. | Federal Taxation of Individuals s (including tax preparation and planning strategies) | 1. Gross income (inclusions and exclusions) 2. Reporting items from pass-through entities 3. Adjustment and deductions to arrive at adjusted gross income and taxable income 4. Passive activity losses (excluding foreign tax credit implications) 5. Loss limitations 6. Filing status 7. Computation of tax and credits | 15-25% |

| 5. | Federal Taxation of Entities (including tax preparation and planning strategies) | 1. Tax treatment of formation and liquidation of business entities 2. Differences between book and tax income (loss) 3. C corporations • Computations of taxable income, tax liability, and allowable credits • Net operating losses and capital loss limitations • Entity/owner transactions, including contributions, loans, and distributions • Consolidated tax returns • Multijurisdictional tax issues (including consideration of local, state & international issues) 4. S corporations is another topic covered under the REG CPA exam. The topic covers • Eligibility and election • Determination of ordinary business income (loss) and separately stated items • Basis of shareholder’s interest • Entity/owner transactions (including contributions, loans, and distributions) • Built-in gains tax 5. Partnerships • Determination of ordinary business income (loss) and separately stated items • Basis of partner’s interest and basis of assets contributed to the partnership • Partnership and partner elections • Transactions between a partner and the partnership (including services performed by a partner and loans) • Impact of partnership liabilities on a partner’s interest in the partnership • Distribution of partnership assets • Ownership changes 6. Limited liability companies 7. Trusts 8. Tax-exempt organizations • Type of organizations • Unrelated business income | 28-38% |

Please prepare a study schedule, keeping in mind the weightage assigned to each group. Furthermore, the AICPA’s CPA Exam Blueprints comprehensively specify the content and skill levels tested for the REG exam section.

How Hard is it to Pass REG?

- CPA is one of the most challenging exams to pass. All the four sections are undeniably tough. Although the pass percentage has been around 50% in the past decade, the vast course makes it hard to ensure quality preparation.

- The REG section tests a candidate for skills to match the high standards required for tax practice. It is considered a challenging exam section as it involves memorizing many laws and regulations related to taxation, which are subject to frequent changes.

- Apart from memorizing, a candidate must use his/her reasoning ability to answer real-world task-based questions. The length of the exam is another factor that makes this section hard to crack.

- To clear this section, a candidate must have a thorough understanding of the structure and content of the exam. The pattern or the type of questions shouldn’t come as a shock to the candidate.

Skill Levels Tested in REG Exam

The CPA exams usually test candidates based on four skills, remembering, application, analysis, and evaluation. The REG exam section checks the candidate for all these skills except for evaluation.

A candidate expected to memorize the provisions and understand their underlying purpose. Based on the understanding, candidates are supposed to express their skills in the application of these provisions.

The weightage of each skill in the REG section are as follows:

| S.No. | Skills Tested | Weightage |

|---|---|---|

| 1. | Memorizing and understanding | 25-35% |

| 2. | Application | 35-45% |

| 3. | Analysis | 25-35% |

When should I take the REG CPA Exam?

- It is a crucial decision to place the REG section in the proper sequence to perform well. The candidates are supposed to consider many factors while deciding the timing of the exam.

- First and foremost is their liking towards the subject. Some candidates, who have a thing for taxation and law, can consider taking this section first. Also, candidates should be aware of their strengths and weaknesses. If you feel that you are sufficiently prepared for REG, you could opt for the exam during the 18 months as it will not take away the preparation time of other sections.

- Since the REG section mainly comprises federal tax laws, a candidate with prior experience in taxation could also appear for this section first. The course requires a considerable amount of memorization, which could be difficult without working in the relevant field. However, candidates who are generally good at memorizing can give it a shot first.

- Candidates with no prior experience in taxation, general dislike for the subject or insufficient preparation may schedule it first. Doing so will leave them more preparation time as opposed to the restrictive 18-month period.

- However, some may contend that appearing for this section first and not clearing it can deter and demoralize them. So, the candidates must take this call themselves according to their circumstances.

REG CPA Exam Time Management

All CPA exams are for four hours. With limited time and a multitude of tough questions, time management is very crucial.

- The MCQs (76 questions) and TBSs (8 questions) contribute 50% to the exam score. Thus, we have two hours or 120 minutes for each. Prima facie calculation tells us that a candidate must take 1.5 minutes (120/76) for each MCQ question to finish the MCQ testlets in two hours.

- However, since MCQ questions are marked on difficulty level, allotting 1.5 minutes to each question is not sensible. We must factor in extra time for difficult questions and the TBS section. Hence, a maximum of 1 minute for medium and 1.5 minutes for difficult MCQ seems ideal. So, an average of 1.25 minutes per MCQ question.

- In the TBS section, we arrive at 15 minutes (120/8) for each TBS question. Since the TBS section is generally tough and time-consuming, 15 minutes won’t suffice. The time factored from the MCQ section (25 minutes) can be accommodated here. We can use around 3 minutes (25/8) more for each TBS question. Hence, a TBS question should not take more than 18 minutes.

Please remember that the REG section contains a higher number of MCQs, so don’t spend more than 1.5 minutes on an MCQ. If you stumble upon a question that is too difficult and you cannot solve it within the stipulated time, jump to the next question. Return to it only if you have any time left.

Also, note that there is no time limit for each testlet. Candidates have the freedom to manage it according to their comfort.

How do I Prepare for REG?

AICPA issues blueprints for each section containing the entire syllabus. It divides content into areas, groups, and topics. Every area has a separate weightage in the exam.

Your preparation should be according to the weightage provided in the AICPA exam blueprints. You can prioritize your syllabus according to it but keep in mind that every area is crucial. You cannot afford to skip any topic. For more exam tips on the REG, check the section below.

What is the best way to study for the REG CPA Exam section?

Consider the following exam tips while preparing for the REG CPA section:

#1 – Do not ignore Business Law

The portion mainly consists of federal taxation, because of which many students tend to ignore or give less attention to business laws. CPA is a professional exam, and it requires a professional approach. Your preparation should be towards a fool-proof study plan to cover every topic at an early stage itself.

#2 – Focus on practical application

The REG section requires both memorization and practical application of the provisions. Examinees tend to ignore the application part of the exam and only focus on learning the relevant provisions. This will not give the desired results, and they might have to reappear.

#3 – Have a plan

Having a well-structured study plan will always ensure that all topics are prepared well in advance. As these exams take a lot of time to prepare, candidates are at the risk of getting drained and giving up without a proper schedule.

Recommended Articles

This has been a guide to REG CPA Exam Section. Here we provide you with complete guide on REG CPA exam format, pass rate and how to prepare for it. You can learn more about finance exams from the following articles –