Part of our Shareholder Equity guide

Reserves and Surplus Definition

Reserves and surplus is the item in the balance sheet that reflects a portion of profits of a company that is kept aside to achieve specific future goals of a business. Some of these business plans may include buying of fixed assets, paying dividends, debt repayments, legal settlements, etc.

The reserves and surplus in balance sheet are recorded under shareholder’s equity section. The accumulation of these amount enables businesses to have their own portion of their profits stored to be used any time without having to take financial obligation from any third-party.

Reserves and Surplus Explained

Reserves and surplus created by the company are the reserves that the company can utilize for the purpose according to nature or the type of such reserve and surplus. Generally, the company creates these reserves to settle any future contingencies. E.g., for strengthening and increasing the company’s financial position in the market, paying off the dividends to all the shareholders of the company, increasing working capital in the company, etc., after fulfilling all the conditions required for that reserve. Sometimes reserves and surplus are maintained in cash to manage the reduction in revenues and slow-paying customers.

The utilization of the reserves and surplus includes purposes such as dividend distribution, meeting future obligations, overcoming losses, managing working capital requirements, fulfilling funds requirements for business expansion, etc.

It is required for the company to maintain reserves, sometimes in cash, to manage the reduction in revenues and slow-paying customers. Generally, the maintenance of cash reserves depends upon the company’s business type.

Types

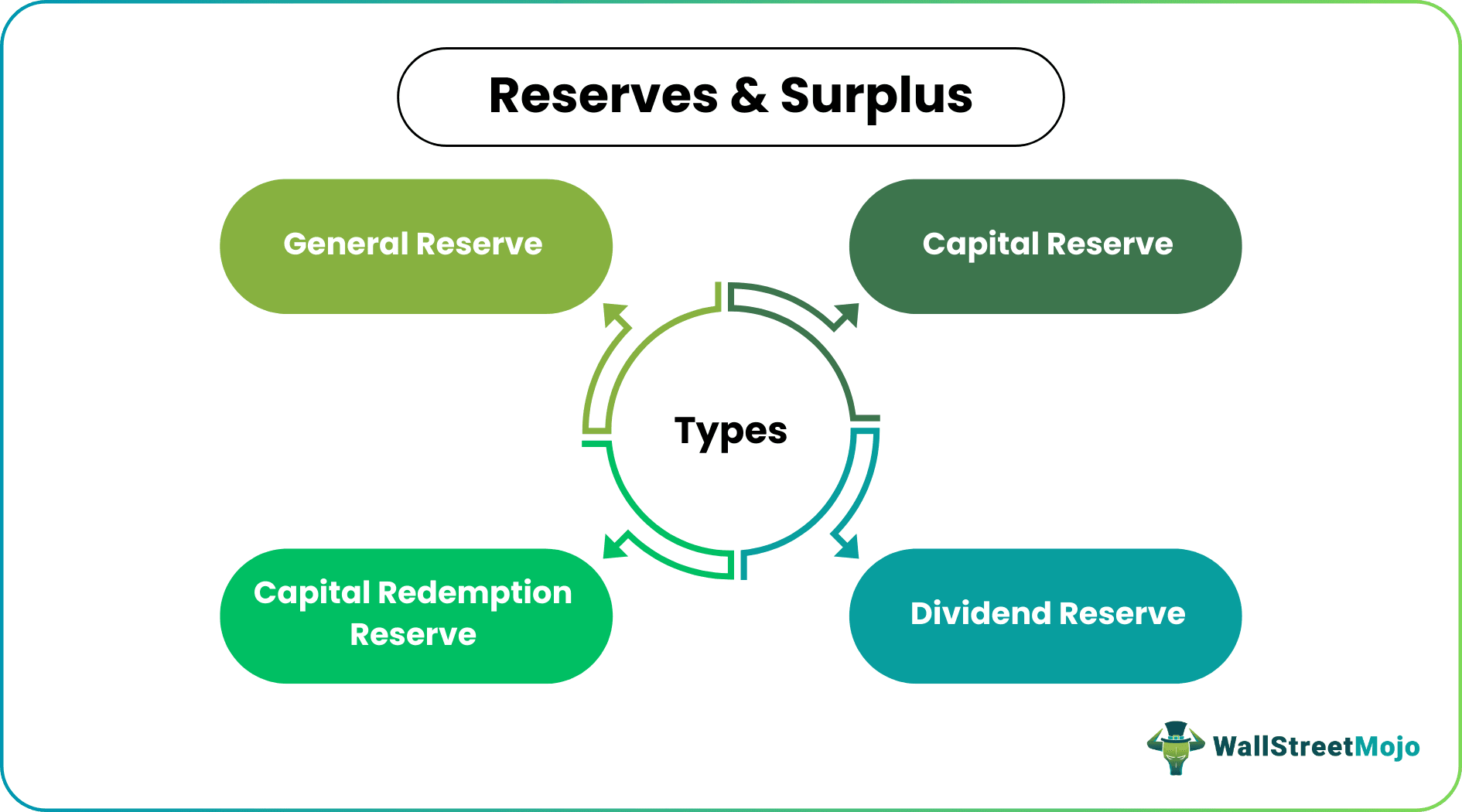

Reserves and surplus exist in multiple forms. The most common ones are as follows:

#1 – General Reserve

A general reserve is also known as a revenue reserve. The amount kept separately by an entity from its profits for future purposes is known as revenue reserves. It is simply the retained earnings of an entity kept aside from its profits for meeting certain or uncertain obligations.

#2 – Capital Reserve

Capital Reserve refers to a part of the profit kept by an entity for a specific purpose, like financing long-term projects or writing off any capital expenses. This reserve is created from any capital profit of an entity that is earned from profit other than the company’s core operations.

#3 – Capital Redemption Reserve

Capital Redemption Reserve is created out of the undistributed profits that are general reserve or the Profit and loss account on the redemption of preference shares or during buyback of own shares to reduce the share capital.

#4 – Dividend Reserve

Dividend reserve is the amount kept in a separate account to ensure that a similar amount of the dividend is declared every year.

Examples

Let us consider the following instances to understand what is reserves and surplus:

Example #1

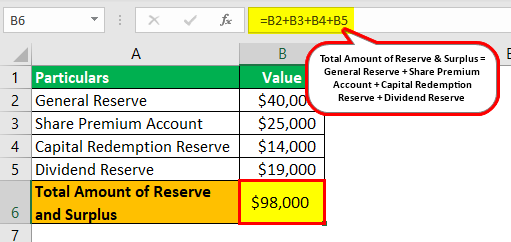

Let us take the example of a Corporation named Computer Web Inc., which is doing the business of computers and laptops. The corporation’s earnings from its normal course of operation during the financial year 2017–18 were $ 500,000. It is decided by the management of the company to keep aside 8 % of the profits earned during the financial year for meeting future liabilities, i.e., General Reserve and the corporation has issued shares for which they have received a premium amounting to $ 25,000.

Also, the amount in capital redemption reserve and dividend reserve amounted to $ 14,000 and $ 19,000, respectively, during the same period. So now we need to calculate the total amount of reserves and surplus, which is the sum of the general reserve, share premium account, capital redemption reserve, and dividend reserve.

Solution:

Total Amount of Reserves and Surplus = $40,000 ($500,000 * 8%) +$25,000 +$14000 + $19,000 = $98,000

Example #2

Reserves and surplus has an important role to play in the event of financial crisis or deteriorating financial state of a nation. In July 2023, Russia announced decreasing the forex sales on a daily basis, which came as a shocking move for the market. It stated that the authorities would sell foreign currencies worth 1.7 billion roubles, which was expected to 74.6 roubles as announced in the previous period almost around the same time.

This is because it was assumed that the revenue generated from the forex market will be used to build reserves and surplus figures to help the country cover up for the lowered oil and gas revenues. Russia made the announcement following the witness of the impact of the Russian-Ukrainian war that has affected the oil and gas transactions to a great extent.

Advantages

Reserves and surplus in accounting is an item in the balance sheet that allows businesses keep funds accumulated for future use. This amount ensures availability of their own funds when they need, thereby preventing them from raising their financial obligations by borrowing from some other sources.

Having this amount is beneficial to many. Some of the advantages include the following:

- Reserves are considered to be the vital source of financing by internal means. So when the company needs funds for its business activities and for meeting its obligations, the first and easiest way to get funds is from the accumulated general reserves of the company.

- With the help of reserves, the company can maintain its working capital requirements as the reserves can be used to contribute towards working capital at the time of the insufficiency of funds in the company’s working capital.

- One of the main advantages of having reserves and surplus is overcoming the companies’ future losses. At the time of losses, reserves can be used to pay off the existing liabilities.

- Reserves are the main source of the amount required for dividend distribution available. It helps maintain uniformity in the dividend distribution rate by providing the amount required for maintaining the uniform rate of the dividend when there is a shortage of amount available for distribution.

Disadvantages

Reserves and surplus funds have numerous benefits, but they also have some limitations at the same time. Let us have a look at the disadvantages of these finances below:

- Finding accurate detail or exact figures is difficult. Suppose the company incurs the losses, which are adjusted/set off with the company’s reserves. In that case, this will somehow lead to the manipulation of accounts as the correct picture of the company’s profitability will not be shown to the users of the financial statements.

- The general reserves that constitute the major part of reserves and surplus are not created for any specific purpose. Still, the general use, so there are chances that there can be a misappropriation of funds accumulated in general reserves by the management of the company, and there is a possibility that the funds will not be used properly for business expansion.

- The Creation of more reserves may lead to a reduction in the distribution of dividends to the shareholders.

Recommended Articles

This article has been a guide to Reserves and Surplus & its definition. Here, we explain the concept along with its examples, types, advantages, and disadvantages. We also discuss the advantages and disadvantages. You can learn more from the following articles –