Part of our Shareholder Equity guide

What Is Additional Paid-in Capital?

Additional Paid-in Capital, also known as capital surplus, is the excess amount the company receives over and above the par value of shares (equity or preferred) from the investors during the time of an IPO; it can be seen as the profit which a company receives when it issues the stock for the first time in the open market.

Additional paid-in capital on the Balance Sheet has nothing to do with the market price per share. It is entirely dependent on the issue price. If an investor purchases shares from the company and sells them off to another investor at a higher price, it would not affect the company’s capital.

Additional Paid-in Capital Explained

Additional paid-in capital, as the name suggests, is the extra amount that one pays for a share. This amount is above the par value of the asset. The par value of a stock is the minimum amount that must be paid to own a share. It means that to acquire a share, this base amount has to be paid.

- For example, if a share is issued at $50 per share and its par value is $5 per share, we will conclude that $5 per share is the minimum amount that must be paid to acquire the share. This base amount is also called the legal capital of the company.

- Here the APIC comes in. Since each company investor pays the whole amount (i.e., the issue price) to acquire one share, anything above par value is APIC.

- Therefore, Additional Paid-in Capital Formula = (Issue Price – Par Value) x number of shares issued.

- If 100 shares are issued, then, APIC = ($50 – $5) x 100 = $4,500

There’s another thing you need to consider to understand the additional paid-in capital meaning properly. If the shares are purchased directly from the company (during IPO or FPO, etc.), there would be APIC above par value. However, if the shares are purchased from the secondary market, it would not affect the company’s APIC.

Additional Paid-in Capital on Balance Sheet Video Explanation

→ Explore all 93 Balance Sheet articles

Formula

The additional paid-in capital formula is:

APIC = (Issue Price – Par Value)*Number of shares investors acquire

Examples

Let us consider the following examples to understand how to calculate additional paid-in capital:

Example #1

Let’s take an example to understand APIC on the balance sheet better.

Let’s say that Company Infinite Inc. has issued equity shares of 10,000 at $50 per share. The par value of each share is $1 per share. Find out the APIC.

This is an easy-to-understand example illustrating how to approach additional paid-in capital on the balance sheet.

Infinite Inc. has issued 10,000 equity shares at $50. That means the total equity capital would be = (10,000 * $10) = $500,000.

- The catch is par value per share is just $1. That means we must attribute the corresponding amount to par value (stock). Here the par value would be = (10,000 * 1) = $10,000.

- And the rest would be additional paid-in capital on the balance sheet as it is over and above the par value. That means the APIC formula = ($50 – $1)/share = $49 per share. Then, the total APIC would be = (10,000 * $49) = $490,000.

Example #2

Let’s say that Company Eight Nest Ltd. has the following information.

Eight Nest Ltd. has issued 10,000 shares at $50 per share. However, they’ve kept the par value (stock) at $5 per share. So we need to pass the accounting entry for additional paid-in capital on the balance sheet.

- Here, we know that the issued number of equity shares is 10,000, and the issue price per share is $50. That means the total equity capital is = (10,000 * $50) = $500,000.

- The par value is also mentioned i.e. $5 per share. That means the total amount par value is = (10,000 * $5) = $50,000.

- The rest would be attributed to APIC. The total APIC would be = [10,000 * ($50 – $5)] = [10,000 * $45] = $450,000.

Now, we will pass the accounting entry –

Journal Entry

How would we pass the accounting entry?

First, we need to think about the legal capital, i.e., par value (stock) amount. Since that’s the legal capital, we will attribute the amount to the common stock account. Then, the remaining amount (issue price – par value per share) would be attributed to APIC.

So, the entry would be –

- The cash account would be debited since cash is an asset, and the company’s asset cash is increasing by receiving the whole amount (total equity capital).

- We would credit the common stock accountand APIC accounts in their respective proportions.

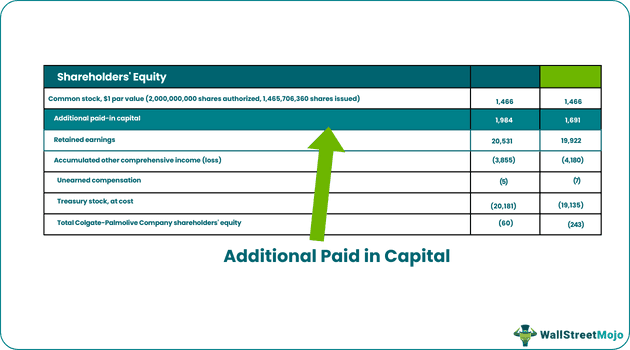

Additional Paid-in Capital on Balance Sheet

Please see below the snapshot. We note that APIC has been changing each year.

We note that the changes in the APIC of Colgate are due to three reasons.

- Share-based compensation expense of $127 million

- Shares issued for stock options of $197 million

- Share issued for restricted stock awards

Share-based compensation expense is reported in the income statement. This lowers the net income, thereby reducing the shareholder’s equity through the retained earnings section. The contra entry for this is by increasing the additional paid-up capital.

Recommended Articles

This has been a guide to what is Additional Paid-in capital. We explain its formula, journal entry, examples & reasons for the changes on the balance sheet. You may also go through the following recommended posts on basic accounting –