Written byAshish Kumar SrivastavAshish Kumar SrivastavEditorial HeadAshish, a seasoned finance professional, content editor, and blogger, brings over a decade of expertise. As Editorial Head at WallStreetMojo, he mentors writers and ensures quality. A self-published author and with a passion for financial literacy, Ashish's extensive knowledge covers investment banking,12+ years of experienceM.Sc.Investment bankingView Full Profile

Reviewed byDheeraj Vaidya, CFA, FRMDheeraj Vaidya, CFA, FRMContent Reviewer & Course DirectorDheeraj is a former J.P. Morgan and CLSA Equity Analyst with nearly two decades of experience in financial modeling, valuation, equity research, and corporate finance. He specializes in helping students and professionals develop practical and in-demand finance skills through structured and AI-powered,20+ Years of experienceCFA, FRM, IIT Delhi, IIM LucknowFinancial ModelingView Full Profile

Sales credit journal entry refers to the journal entry recorded by the company in its sales journal when the company makes any sale of the inventory to a third party on credit. In this case, the debtor’s account or account receivable account is debited with the corresponding credit to the sales account.

Credit sales boost the buyer’s inventory and also give them enough time to sell the product and repay their supplier. This credit period is usually decided well in advance and can vary from industry to industry. Default on the due date can also lead to penalties or legal proceedings against the defaulter.

Sales credit journal entry means recording the journal entry by the company in its sales journal if the company makes any inventory sale to a third party on credit.

It is vital for companies that sell their goods on credit.

During sales on credit, accounts receivable accounts are debited and shown in the company’s balance sheet as an asset until the amount is received against such sales and the sales account is credited. It is displayed as revenue in the company’s income statement.

It helps to track the transaction engaging the goods sale on credit by the company appropriately.

Sales Credit Journal Entries Explained

Sales credit journal entry is vital for companies that sell their goods on credit. At the time of sales on credit, accounts receivable accounts will be debited, which will be shown in the balance sheet of the company as an asset unless the amount is received against such sales, and the sales account will be credited, which will be shown as revenue in the income statement of the company.

It helps record the transaction involving the sale of goods on credit by the company appropriately, keeping track of every credit sale involved.

When the goods are sold on credit to the buyer, the account receivable account will be debited, which will lead to an increase in the company’s assets as the amount is received from the third party in the future. Therefore, it leads to the asset creation of the company and is shown in company’s balance sheet unless settled.

When the goods are sold on credit to the buyer of the goods, the sales account will be credited to the company’s books of accounts. Therefore, it will increase the revenue and reflect in the company’s income statement during the sale period.

How To Record Entry?

A sales credit journal entry record helps companies credit the respective account with the amount receivable with the details about the transaction. The method of documentation is decided before the commencement of a financial or assessment period and they stick to the method to ensure there is no confusion in the recordkeeping structure of the organization.

When the goods are sold on credit to a buyer, the account receivable account debits, increasing the company’s assets as the amount is receivable from the third party. The corresponding credit will be in the sales account, increasing the company’s revenue. The entry to record the sales on credit is as follows:

Particulars

Dr ($)

Cr ($)

Account Receivables A/C …..Dr

XXX

To Sales A/C

XXX

When the company receives the cash against the goods sold on credit, the cash accounts will be credited as there is the receipt of the money against the goods sold on credit. There will be corresponding credit in the accounts receivable accounts as the account was initially debited at the time of sales of goods and thus will be credited once the amount is received. The entry to record the receipt against the sales on credit is as follows:

Particulars

Dr ($)

Cr ($)

Cash A/C …..Dr

XXX

To Accounts Receivable A/C

XXX

Examples

Let us understand how organizations maintain sales credit journal entry records with the help of a few of examples.

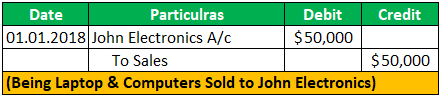

Example #1

Apple Inc is a laptop and computer dealer, and it sold goods to John Electronics on January 1, 2018, worth $50,000 on credit. Its credit period is 15 days. It means John Electronics must make the payment on or before January 30, 2018.

Below are the journal entries in the books of Apple Inc:

At the time of sale of laptop & Computer:

At the time of Receipt of Payment:

Example #2

Apple Inc gives cash discounts or early payment discounts. In the above example, Apple Inc is offering a 10% discount if John Electronics makes the payment on or before January 10, 2018. Accordingly, John Electronics made the payment on January 10, 2018.

Below are the journal entries in the books of Apple Inc:

Example #3

In the above example, John Electronics could not make payment by January 30, 2018, and it went bankrupt. And Apple Inc believes that outstanding debt is unrecoverable and is a bad debt now.

Below are the journal entries in the books of Apple Inc:

John Electronics will pass access for bad debt at the end of the financial year.

Example #4

ABC Inc sold goods worth $1,000 to XYZ Inc on January 1, 2019, on which 10% tax is applicable. XYZ Inc will make payment in two equal installments to ABC Inc.

Below entries will be passed in the books of ABC Inc:

At the time of credit sales:

In the above example, we assume the basis value of goods is $1,000. Therefore, we have charged 10% of tax on that value, which ABC Inc will collect from XYZ Inc and pay to the government, and ABC Inc can take input credit of the same amount and claim a refund from the government.

At the time of receiving of 1 Payment:

Example #5

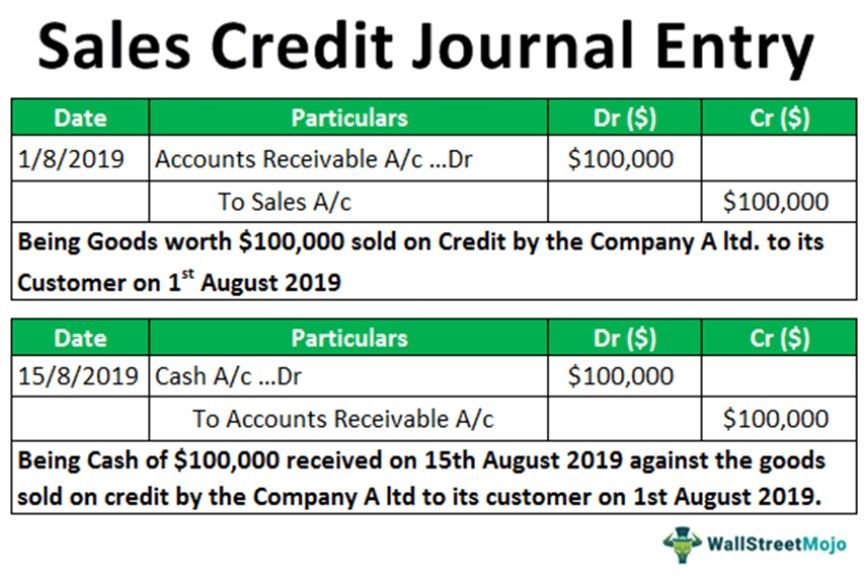

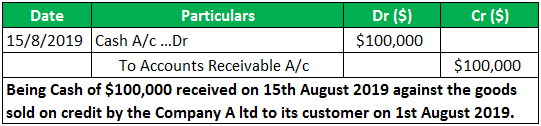

For example, there is company A Ltd. which deals in selling the different products in the market. On August 1, 2019, it sold some goods to one of its customers on credit, amounting to $100,000. When selling the goods, the customer decided to pay full against the goods received after 15 days. On August 15, 2019, the customer paid the whole amount to the company. Now, how will the firm pass the journal entry to record the sales of the goods on credit and the receipt of cash against the sales of goods?

Solution

On August 1, 2019, when the company sells the goods on credit to the buyer, they will debit the account receivable account with the corresponding credit to the sales account. Therefore, the entry to record the sales on credit is as follows:

On August 15, 2019, when the customer paid the whole amount in cash to the company against the goods sold on credit on August 1, 2019, the cash accounts will be credited with the corresponding credit in the accounts receivable accounts. The entry to record the receipt against the sales on credit is as follows:

Now we will understand how to show all the above entries in financial statements.

Credit Sales: Sales, whether cash or credit, will come in profit & loss a/c under the income side with the sale value of goods.

Debtors: Debtors are current assets and will come under the assets side of the balance sheet under existing assets.

Bank: Bank balance is also a current asset. Therefore, it will show under the assets side of the balance sheet under existing assets. On the receipt of customer payment, the bank amount will increase, whereas debtors will decrease. Thus, the total balance of current assets will not remain the same.

Discount: Any discount given to the dealer comes under the expenditure side of the profit & loss account, decreasing the company’s profitability.

Advantages

Let us discuss the advantages of organizations delaying their inflow of money through credit sales and how the journal entries help them maintain a record of their amount receivables.

They help record the transaction involving the sale of goods on credit by the company appropriately, keeping track of every credit sale involved.

With the help of a sales credit journal entry, the company can check the balance due to its customer on any date. In addition, it will help the company monitor the balance outstanding of the customer in case the customer approaches again for credit sales.

Limitations

Despite the advantages discussed above, there are a few factors from the other end of the spectrum that prove to be a hassle or hurdle for organizations. Let us understand by discussing the disadvantages from the explanation below.

If the person recording the transaction commits any mistake, it will show the wrong trade in the company’s books of accounts.

When many transactions are involved in the company, recording the sales credit journal entry for every company transaction becomes problematic and time-consuming. It also increases the chances of mistakes by the person involved in such a matter.

Frequently Asked Questions (FAQs)

What is the double entry for credit sales?

Double-entry bookkeeping tracks credit sales. The debit value in a company’s accounts must equal the value of the credits. In addition, one must keep track of five types of accounts when doing double-entry bookkeeping.

What is the credit sales journal entry with GST?

The journal entry for GST has several entries such as purchase transactions, sale transactions, set off of input credit against out tax liability of GST, reverse charge transaction, refunds (export of goods and services), and imports.

What is the journal entry for credit sales with discount?

The credit sales with discounts are directly deducted from the gross sales in the income statement. It means that the value of sales recorded in the income statement is the net of sales discount, cash, or trade discount.

How to pass journal entry for credit sales?

The sales credit journal entry must have the sale date, the customer’s name, the sale amount, and the accounts receivable amount.

Recommended Articles

This article has been a guide to what is Sales Credit Journal Entry. Here we explain its examples, how to record them, and its advantages, & limitations. You can learn more about accounting from the following articles –