Part of our Profitability Ratios guide

What is Adjusted EBITDA?

Adjusted EBITDA is the measurement of a company’s recurring earnings before deducting interest expense, tax expense, depreciation & amortization expenses and further adjusting extraordinary and non-recurring items are adjusted from the amount of EBITDA like legal expenses, gain/loss on the sale of a capital asset, impairment of assets, etc.

It is a valuable financial metric that arises after removing one-time and nonrecurring items from EBITDA (earnings before interest, taxes, depreciation, and amortization). It is also referred to as Normalized EBITDA. Normalization is systematizing cash flows and removing anomalies or deviations from a financial metric, say standard EBITDA. This amount has to be separately calculated for valuation and analytical purposes. Public companies are required to report only the figures of standard EBITDA under GAAP rules.

Adjusted EBITDA Formula

Let us look at the adjusted EBITDA formula.

Adjusted EBITDA = EBITDA +/- Adjustments

Where EBITDA = Net Income + Interest + Taxes + Depreciation and Amortization

Explanation of EBITDA in Video

List of Items excluded in Adjusted EBITDA

- Non-Operating Revenue

- One time gain or sale of Property, business, etc

- Restructuring and Reorganization charges

- Unrealized gains and losses

- Legal Expenses

- Impairment of Goodwill

- Impairment of Assets

- Forex Gains/Losses

How to Calculate Adjusted EBITDA?

Follow the below steps:

- First, calculate standard EBITDA using the net income from the company’s income statement. Net income includes expenses of interest, taxation and depreciation, and amortization. Add these expenses to the net income figure to get the EBITDA value.

- Now add all those one-time non-recurring expenses that do not occur regularly like Excess owner’s salary, litigation expenses, special donations, etc. Also, add all those expenses unique to the company and usually do not incur by peer companies.

Examples

Let us look at a few adjusted EBITDA examples to understand the concept better.

Example #1

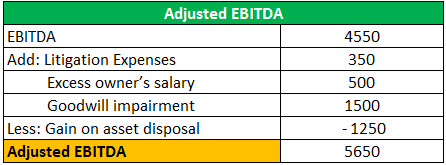

ABC investments advisory gave a task to Mr. Unreal to find the adjusted EBIT of Banana Inc for the previous year and provide the data of the income statement of the company. Mr. Unreal first calculates EBITDA and then makes necessary adjustments to arrive at the adjusted EBITDA figure. As follows:

Example #2

According to a report published in July 2026, Prosus reported that its India ecosystem achieved adjusted EBITDA profitability for the first time. The company recorded an adjusted EBITDA profit of $18 million in FY26, whereas it reported a loss of $25 million in the previous fiscal year.

The improvement was primarily driven by the strong performance of its fintech platform PayU. The platform’s payments business generated an EBITDA of $12 million, while its credit business reported an adjusted EBITDA profit of $6 million.

Importance

EBITDA is an important valuation tool because it is used as a proxy for operating cash flows to calculate the company’s enterprise value. However, adjustments to EBITDA should not be overlooked as they can significantly impact business valuation. E.g., in the above example, after calculating EBITDA and adjusted EBITDA, Mr. Unreal is further given a task to calculate the enterprise value. An industry multiple of 5-times has been provided.

Enterprise value = EBITDA * Multiple

The enterprise value with a given multiple of 5 becomes $ 22,750,000 for EBITDA of $ 4,550,000. Now let’s calculate the enterprise value using the adjusted EBITDA of $ 5,650,000. We get Enterprise value of $ 28,250,000 ($ 5,650,000 * 5).

The enterprise value of Banana Inc boosted by a tremendous amount of $ 5,500,000 ($ 28,250,000 – $ 22,750,000). Hence Mr. Unreal must consider the adjusted EBITDA while calculating the value of the business.

Note: Adjustments made to EBITDA generally are one-time expenses that will not incur soon or after the business gets sold. Thus such expenses must be true and fair because the management of the buying company strictly scrutinizes these.

Adjustments to EBITDA and its Impact on Enterprise Value

- Excess Owner Salaries: If the owner’s salary, including bonuses and commissions, is $ 500,000 per annum but the market rate to replace the owner is $ 350,000. i.e., the owner is taking an excess salary of $ 150,000. It can be charged as an adjustment. The value of the enterprise increased by $ 750,000, considering the industry multiple of 5 times. i.e. $ (500,000 – 350,000) * 5

- Litigation Expenses: Litigation expenses in the form of a lawsuit settlement and legal and consultancy fees are non recurring expenses and can be charged as legitimate adjustments.

- Disposal of Assets: Assets are not meant to be sold. However, there are situations like technology upgrades, lower performance of existing assets, etc. These are one-time, nonrecurring expenses or gains that can be positively or negatively adjusted as a legitimate adjustment. E.g., the number of profits for the property sold must be deducted from EBITDA. In contrast, the number of losses on sales of some old machinery can be added to EBITDA as legitimate adjustments.

- Rent of the facilities: The difference would be negative if the rent charges are above fair market value. Rent profits must be deducted as negative adjustments and vice-versa for the opposite situation.

Advantages and Applications

- It removes nonrecurring items and anomalies that distort EBITDA

- It can be used to evaluate a company’s overall income and determine its annual cash generation.

- It is usually required when a company is being valued for acquisitions and mergers (M&A)

- It can more accurately represent a company’s future earnings capacity that an investor would expect.

- It can be used to make easy and meaningful comparisons across various companies since different companies charge various expenses that are unique or do not incur by companies with similar businesses.

- Adjusted EBITDA is used to analyze companies to value them for potential acquisitions properly.

Disadvantages

The rules of GAAP do not apply to adjusted EBITDA values. The companies thus can manipulate these EBITDA figures and publish the misleading values by adding a variety of unnecessary expenses, to artificially inflate margins and distract the investor from ugly-looking net income figures.

Thus investors and analysts should properly scrutinize the adjustments. Remember, the EBITDA margins of a company will always remain higher than its Net profit margin, and the Adjusted EBITDA margins are generally higher than its standard EBITDA margins.

Conclusion

Adjusted EBITDA normalizes the EBITDA value that represents the company’s financial health more accurately. It is mainly used to value the enterprise during mergers and acquisitions. The adjustments can inflate the value of the company, sometimes dramatically. But adjustments must be made with full care and due diligence so the buyer can accept those adjustments to be fair and legitimate.

Recommended Articles

This article has been a guide to what is Adjusted EBITDA. Here we discuss how to calculate Adjusted EBITDA using its formula along with practical examples & explanations. We also discussed its advantages and disadvantages. You can learn more about financing from the following articles –