Part of our Income Statement guide

What Are Unrealized Gains & Losses?

Unrealized Gains or Losses refer to the increase or decrease in the paper value of the different assets of the company which have not yet been sold. Once such assets are sold, the company will realize the gains or losses.

It is also called “paper profit” or “paper loss.” It can be thought of as money on paper, which the company expects to realize by selling the asset in the future. When the company sells the asset, it realizes the gains (losses) and pays taxes on such profit.

Portfolio valuations, mutual funds NAV, and some tax policies depend on Unrealized gains/losses, also called marked to market.

Calculate Unrealized Gain & Losses with Example

Example #1

A Company XYZ has an investment of $ 10000 in stocks, which it holds for trading purposes. The value of these stocks has increased to $ 25000. The company could record $ 15000 as an Unrealized gain on these positions without selling the securities. It will only be paper profit, and the company will not be liable to pay taxes for such recorded Unrealized gains.

However, say he sells these positions for $ 30000 later in the year or next year, it would record a realized gain of $ 20000 in the net income, and he is liable to pay taxes on such gains.

From the above example, we can say that Unrealized gain is a difference between the value of investment now and the investment done in the past.

Example #2

Let us take another example. ABC bought 500 stocks for $3, each with an original investment of $ 1500. He paid a brokerage of $10 on the purchase of these stocks, and the current value of each stock is $7. Here, the total value of the investment is $ 3500. Thus, the Unrealized gain is (3500 – 1500 = $ 2000). However, to be precise, the person can subtract the brokerage paid on these stocks and say the Unrealized gain is 2000 – 10 = $ 1900.

Let us take another example:

The Dot-com bubble created a lot of Unrealized wealth, which evaporated as the crash happened. During the dot-com boom, many stock options and RSUs were given to the employees as rewards and incentives. It saw many employees turning into millionaires in no time, but they could not realize their gains due to restrictions holding them for some time. Thus, the dot-com bubble crashed, and all the Unrealized wealth evaporated.

Video On Unrealized Gains & Losses

Unrealized Gains & Losses Accounting

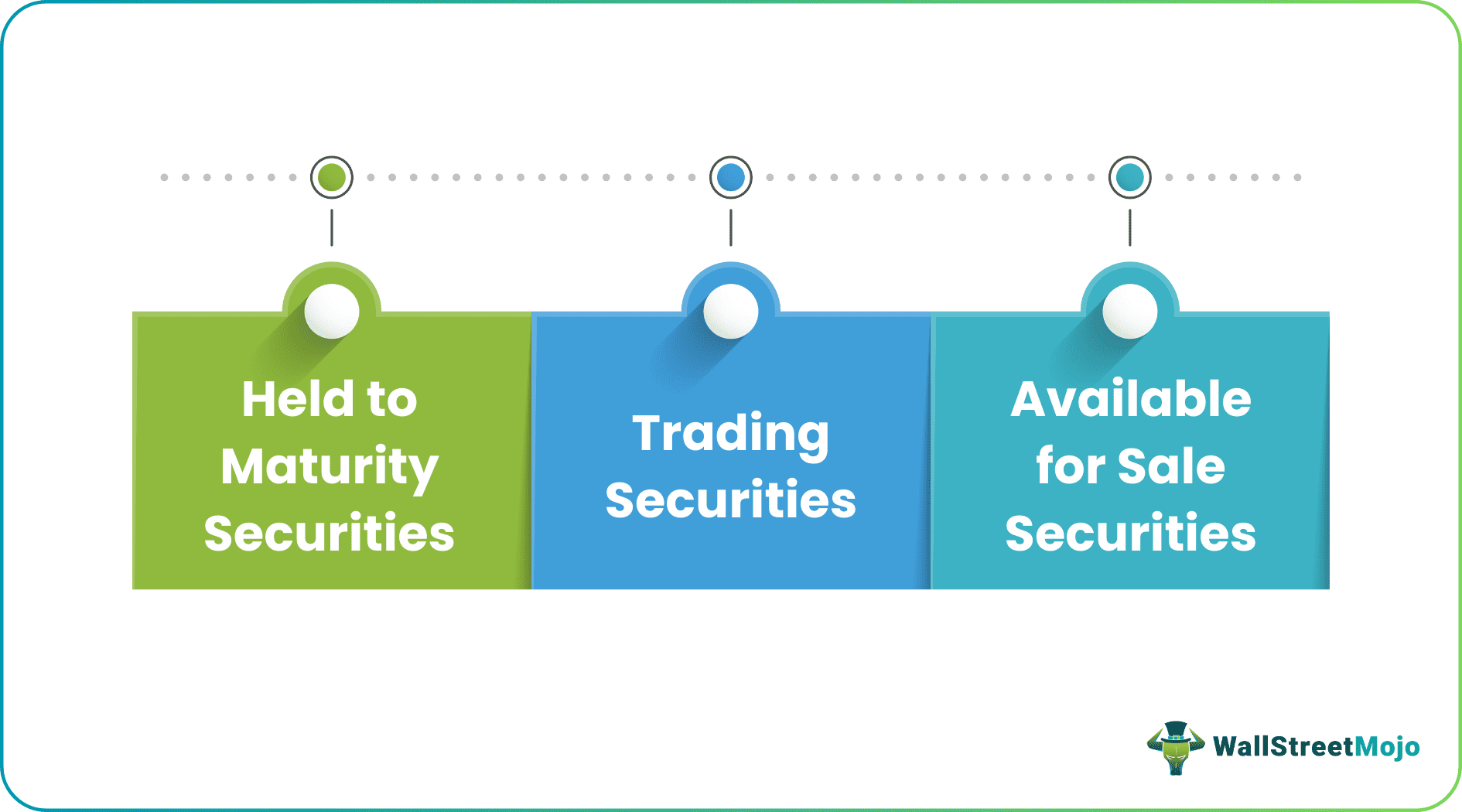

The accounting treatment depends on whether the securities are classified into three types, which are given below.

#1 – Held to Maturity Securities

Unrealized Gain and losses on securities held to maturity are not recognized in the financial statements. Therefore, such securities do not impact the financial statements – balance sheet, income statement, and cash flow statement. Many Companies may value these securities at market value and may choose to disclose it in the footnotes of the financial statements. However, securities are reported at amortized cost if the market value is not disclosed to maturity.

#2 – Trading Securities

Securities held as ‘trading securities‘ are reported at fair value in the financial statements. Unrealized gains or unrealized losses are recognized on the PnL statement and impact the company’s net income, although these securities have not been sold to realize the profits. The gains increase the net income and, thus, the increase in earnings per share and retained earnings. There is no impact of such gains on the cash flow statement.

#3- Available for Sale Securities

Available for sale securities are also reported at fair value. However, accounting for such securities differs from ‘trading securities.’ Due to fair value treatment for “available for sale” securities, Unrealized gains or losses are included in the balance sheet on the asset side. However, such gains do not impact the net income of the company. The Unrealized gains on such securities are not recognized in net income until they are sold and profit is realized. They are reported under shareholders equity as “accumulated other comprehensive income” on the balance sheet. The cash flow statement is also not affected by such securities.

Unrealized Gains & Losses on Income Statement/Balance Sheet

→ Explore all 93 Balance Sheet articles

The accounting treatment for various types of securities and their impact on financial statements is tabulated below:

| Type of security | Valued at? | Impact on Balance sheet | Impact on Income Statement | Impact on Cash flow |

|---|---|---|---|---|

| Held to maturity | Generally Amortized to cost | No Impact | No Impact | No Impact |

| Trading securities | Fair Value | Unrealized gain/losses recognized on the Balance sheet | Unrealized gains/losses recognized on PnL statement and impacted net income | No impact |

| Available for sale | Fair Value | Unrealized gains or losses recognized on Balance sheet | Unrealized gains or losses not recognized on PnL | No Impact |

Importance

- It is good to know the unrealized gain on the portfolio. It helps to track the performance of the portfolio. However, these are only “on paper” profits but give a good estimate of what actual profits could be short if the positions are sold.

- They help in tax planning. Taxes are paid only on realized gains; thus, by knowing the Unrealized Gain, the company can forecast the amount of tax to be paid if they sell the securities.

- The investor can plan when to sell the security and realize his gains. Holding security for a long time may reduce the tax implication as it will be treated as long-term capital gains tax. Thus, the investor can plan and sell the security after one year of its purchase than selling in the same year to reduce the tax implication.

Conclusion

An Unrealized gain is an increase in the value of the investment due to the increase in its market value and calculated as (Fair Value or market value – purchase cost). Such a gain is recorded in the balance sheet before the asset has been sold, and thus the gains are called Unrealized because no cash transaction happened. Except for trading securities, the Unrealized gains do not impact the net income. The gains are realized only after selling the asset for cash because it is only when the transaction has materialized.

Recommended Articles

This article has been a guide to what are Unrealized Gains and Losses. Here we discuss how to account for unrealized gains or losses depending on the type of securities with examples. You may also have a look at these articles below to learn more about accounting –