Part of our Efficiency Ratios guide

What Is A Combined Ratio?

A combined ratio, which is generally used in the insurance sector (especially in property and casualty sectors), is the measure of profitability to understand how an insurance company is performing in its daily operations and is by the addition of two ratios, i.e., underwriting loss ratio and expense ratio.

Calculating the combined ratio in insurance is easy once one knows where to get the numbers from. The biggest hint is knowing the meaning and discovering where to locate the numbers in the financial reports. It can be challenging if one doesn’t know what and where to look for it.

- The combined ratio is a measure used in the insurance industry to assess the profitability of an insurance company.

- It is calculated by adding two ratios: the underwriting loss ratio and the expense ratio.

- The combined ratio in insurance comprises two components: the calendar year loss ratio and the statutory basis expense ratio.

- If it is greater than 100%, the company pays out more than it earns in premiums. If it is less than 100%, the company earns more premiums than it spends on claims and expenses.

Combined Ratio Explained

A combined ratio, as the name suggests, is the combination of two figures, which include the incurred losses and expenses. When this figure is known and is divided by the earned premium. As a result, it assesses the profitability of an insurance company. In short, one can identify which insurance companies are profitable and those that are not good enough. It is a ratio that applies to mostly property-casualty insurance companies.

It is used to measure the profitability of an insurance company, specifically property and casualty-based insurance companies. The combined ratio measures the losses made and expenses about the total premium collected by the business. It is the most effective and most straightforward way to measure how profitable the company is

It is a way to measure if premiums collected as revenue are more than the claim-related payment it has to pay. It is the easiest way to measure if the business or company is financially healthy or not. It is determined by summing up the loss ratio and expense ratio.

In trade-based combined ratio cases, the insurance company pays less than its premiums. Alternatively, when we consider the financial basis combined ratio, the insurance company pays the equivalent amount to the premiums it receives.

A healthy combined ratio in insurance sectors is generally considered to be in the range of 75% to 90%. It indicates that a large part of the premium earned is used to cover the actual risk.

Formula

The formula used for combined ratio calculation is represented as below:

where,

- Underwriting Loss Ratio = (Claims paid + Net loss reserves) /Net premium earned

- Expense Ratio = Underwriting expenses including commissions /net premium written

Underwriting Expenses are expenses linked to underwriting and comprise agents’ sales commissions, insurance staff salaries, marketing expenses, and other overhead expenses.

How To Calculate?

The combined ratios comprise the sum of two ratios, which are separately calculated. Let us see how the step-wise calculation is carried out:

- The first is calculated by dividing loss incurred plus loss adjustment expense (LAE) by premiums earned, i.e., the calendar year loss ratio).

- The second one is calculated by dividing all other expenses by the written or earned premiums, i.e., statutory basis expense ratio.

When the resultant is applied towards the final result of a company, the combined ratio is also termed a composite ratio. Both insurance and reinsurance companies use it.

The combined ratio is usually considered as a measure of the profitability of an insurance company; It is indicated in a %, and if it is more than 100%, it means that the company is paying more than it is earning, while if it is less than 100%, it means that it is earning more than what it is paying.

Example

Let us consider the following examples to understand the combined ratio definition and see how a combined ratio is calculated;

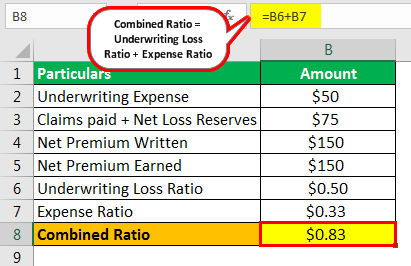

ABZ Ltd. is an insurance company. The company’s overall underwriting expense is calculated to be $50 million. It has incurred a loss, and also adjustment made towards it is $75.The company’s net premium written stands at $200 million, and in the year, it has earned an overall premium of $150 million.

Solution

ABZ Ltd.’s combined ratio is calculated by summing up the losses incurred and adjustments made towards it and dividing the resultant with the premium earned. Thus the financial basis combined ratio is 0.83, or 83% (i.e. $50 million + $75 million)/$150 million.

To calculate the combined ratio on a trade basis, sum up the adjustment ratio of losses by premium earned and the ratio of underwriting expenses by net premium written.

Calculation of Combined Ratio

- =$0.50+$0.33

- =$0.83

The trade basis combined ratio of ABZ Ltd. thus stands to be 0.83, or 83%, i.e., $75 million/$150 million + $50 million/$150 million.

Advantages

When combined ratios are calculated and exact figures are known, they help both insurance companies and insurance seekers be aware of how fruitful the insurance deal is for them:

- It gives a better picture of how efficiently premium levels were set.

- It indicates the company’s management where the company is making a profit or not, i.e., if the earnings is more /less than payments.

- It is the best way to calculate the profit since it does not consider the investment income and only concentrates on underwriting operations.

- Both the components of the combined ratio can be explained separately. The underwriting loss ratio measures the company’s efficiency on the standard of its underwriting methodology. In contrast, the expense ratio measures how well proper the company’s overall operation is.

Disadvantages

Besides having the benefits, combined ratio calculation also has some limitations, which include the following:

- It does not give the entire picture about the profitability of the company because it excludes the investment income. These companies earn a good source of income from investments in bonds, stocks, and other financial instruments that are outside their core business.

- It is made up of many components. We tend to focus just on the CR number and miss analyzing the components it is made up of.

- We cannot tell if the CR is more significant than 100%, which means a company is not profitable because it may happen the company is making a fair amount of profit from other investment income.

- The firm can make specific changes to its financial statements to improve the components of the combined ratio, and thus this ratio ends up nothing but window dressing.

- It only considers the monetary aspects of the firm and ignores the qualitative aspects.

- Having many advantages, it also has certain limitations. The various elements that make up the combined ratio (losses, expenses, and earned premium) each act as a benchmark of the potential for profitability or the risk of loss.

- Thus, it is necessary to understand these components individually and together to accurately determine the company’s financial performance.

Combined Ratio vs Loss Ratio

Though both these ratios help assess the profitability of the insurance companies, they share multiple dissimilarities. Let us have a look at the differences between combined and loss ratios:

- While the loss ratio is the measure of the total losses incurred with respect to the total insurance premiums collected, the combined ratio obtains the measure of incurred losses as well as expenses, both with respect to the total insurance premiums that an insurance company collects.

- The lower the loss ratio, the more profitable an insurance company is. On the contrary, when the combined ratio is above 100%, it signifies that the insurance companies are paying off claims that are higher than the premiums they collect.

Frequently Asked Questions (FAQs)

1. How to achieve a lower combined ratio?

Insurance companies that consistently maintain a lower combined ratio are generally considered more financially stable and more likely to remain profitable over the long term. A lower combined ratio may be achieved through various means, such as improving risk selection, increasing premiums, reducing expenses, or increasing investment income.

2. What is the combined ratio vs. compound gear ratio?

The combined ratio is a measure used in the insurance industry to assess an insurer’s profitability by comparing the amount of money it pays out in claims and expenses to the premiums it receives. On the other hand, the compound gear ratio is a measure used in mechanics to describe the relationship between the number of teeth on two interlocking gears.

3. What isthe break-even combined ratio?

The break-even combined ratio is when an insurance company’s premium income equals its losses and expenses. At this point, the insurer is not making a profit but is not losing money either.

Recommended Articles

This article has been a guide to what is a Combined Ratio. We explain it with formula, vs loss ratio, example, how to calculate it, advantages, and disadvantages. You may also have a look at these articles below to learn more about financial analysis –