Reinsurance Meaning

Reinsurance is a deal wherein the insurer shares a part of the risk portfolio with another insurance firm. It helps spread the risk to avoid an enormous unmanageable financial strain on a single entity. Reinsurance companies are of two types: facultative and treaty.

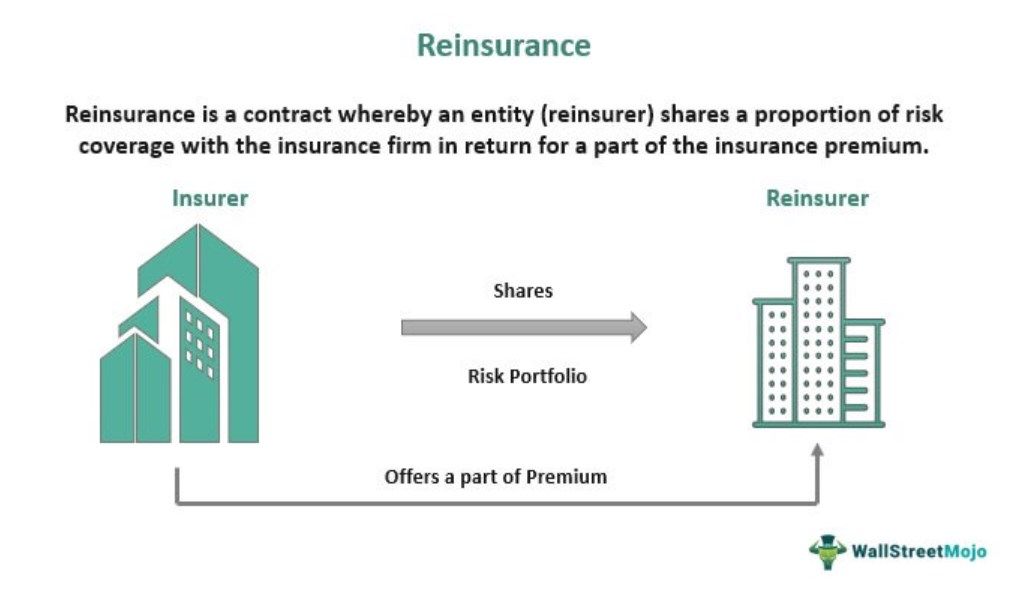

The insured entity is called a ceding insurer, while the organization reinsuring it in return for a portion of the insurance premium is labeled a reinsurer. Moreover, the ceding insurer can promptly buy it from the reinsurer or by a mediator or liaison.

Key Takeaways

- Reinsurance refers to insurance carriers’ (ceding insurers) insurance to divide their credit risk with another insurance firm (reinsurers).

- It helps share the risk between two parties (insurers and reinsurers) and avoids the immense fiscal burden on a single entity.

- The primary insurer can reinsure itself directly through a reinsurer or via a negotiator or broker.

- It is categorized into two fundamental types: facultative and treaty reinsurance.

- Its benefits include enhanced capacity, loss stabilization, decreased risk, and security against massive catastrophes.

Reinsurance Explained

Reinsurance can be an unfamiliar feature of the insurance business for several people, but its origin stems from the 14th century. Initially utilized for fire and marine insurance, reinsurance companies have grown through the past century to include almost all facets of the insurance sector.

Please note that insurers can buy it from three different sources. Moreover, these incorporate reinsurance divisions of US primary insurance firms, reinsurance firms situated in the US, and alien (non-US resident) reinsurers with a non-native license.

Recording of reinsurance may occur on an excess of loss or proportional basis. To clarify, the former splits every loss, insurance claim, and installment between insurer and reinsurer beforehand. At the same time, the latter requires the insurer to bear loss compensation until a prearranged retention level and transfer extra charges to the reinsurer until the contract limits.

This pursuit is always developing since insurers and reinsurers sell different risk types (especially natural disasters) to institutional investors. So, it comprises catastrophe bonds and other alternate risk-spreading systems. The new utilities increasingly display an eventual blending of investment banking and reinsurance.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Types Of Reinsurance

To clarify, reinsurance companies offer two major types of services:

1. Facultative Reinsurance

It is called facultative as the reinsurer possesses the “faculty” or power to accept or reject the entire or a proportion of the provided policy. Here, the insurer utilizes it to cover single or multiple risks registered in the insurer’s business book.

Facultative reinsurance usually covers a single deal and is a one-time agreement with the insurance firm. Most importantly, the primary insurer and reinsurer design a facultative certificate displaying the reinsurer’s absorption of a particular risk in the contract.

2. Treaty Reinsurance

The treaty reinsurance demonstrates insurance obtained from another insurer through the insurance firm. Additionally, this offers extra security for the equity of ceding insurers and increases safety in relevant or extraordinary situations. Therefore, it is further categorized into two categories, namely, proportional and non-proportional.

This coverage type is effective for a specific period instead of a contract or per-risk basis.

Examples

For better understanding, the following are some pieces of the reinsurance news.

Example#1

Say, an insurance firm ABC Co. (ceding insurer), signs the contract for portfolio risk division with XYZ Co. (reinsurer). The expenses, losses, and premiums are now shared between firms to the specified limit.

XYZ Co. is liable to share the loss with ABC Co., in return for which the latter will pay the mutually-agreed premium amount to the former. Moreover, this assists both entities in maintaining healthy (individual and collaborative) financial health.

Example#2

Russia’s state-controlled Russian National Reinsurance Company (RNRC) is now the major reinsurer of the state ships, covering Sovcomflot’s fleet. However, before the sanctions on Russia due to the Ukraine invasion, it relied on a global pool of reinsurers providing extensive coverage.

In March 2022, Russia’s central bank reportedly claimed to raise RNRC’s capitalization from 71 billion to 300 billion rubles. Additionally, the guaranteed capital surged to 750 billion rubles to offer enough resources to reinsure.

Benefits Of Reinsurance

As per the information based on reinsurance news, here are its advantages:

1. Enhanced Capacity

As it decreases the insolvency risk, the reinsurer has more policyholders. Moreover, this is similar to using a special purpose vehicle for liabilities removal from the balance sheet. As a result, the company is considered fully capable of successful claim payment in a disaster.

2. Loss Stabilization

A huge amount of claim disbursements in a short period might make the insurer financially unstable. In such situations, risk portfolio division with another party confirms fiscal stability even during the tough times (like hedging.)

3. Decreased Risk

Insuring residential or commercial property is risky, especially if vulnerable to natural disasters like blizzards or storms. So, spreading risk between two parties reduces the debt burden on a sole entity.

4. Safeguarding Against Massive Catastrophes

Reinsurers are typically required in case innumerable claims are recorded at a given time. Usually, this occurs after a natural disaster like a tornado, flood, or hurricane. Reinsurers are ultimate saviors when several policyholders demand instant damage repairment claims.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What Is Reinsurance in Insurance?

Reinsurance in insurance is an agreement between the insurance firm and the reinsurer for risk portfolio transferral. Furthermore, the original policy-issuing firm is called the primary insurer, while the company accepting obligations from the primary insurer is named the reinsurer. Initial companies supposedly cede transactions to the reinsurer.

What Are Reinsurance Companies?

Reinsurance companies are firms that insure the primary (or ceding) insurers. Here are some famous examples in the global context,

1. Munich Reinsurance Company

2. Swiss Re Ltd.

3. Lloyd’s

4. General Insurance Corporation of India

5. African Reinsurance Corporation

How Reinsurance Works?

Reinsurance is a vital risk management mechanism employed by insurance firms to safeguard themselves from huge monetary losses. To clarify, it implicates insurance for insurance firms and is divided into two categories: treaty and facultative reinsurance.

Insurance enterprises submit premiums to reinsurers and the latter, in return, provides coverage for losses imposed by insurance firms till a mutually-decided amount.

Recommended Articles

This has been a guide to Reinsurance and its Meaning. Here we discuss reinsurance companies, news, types (facultative and treaty), and benefits. You can more about finance from the following articles –