Part of our Efficiency Ratios guide

What Is The Inventory Conversion Period?

→ Explore all 82 Inventory articles

The inventory conversion period determines how much time it takes to convert the inventory into sales, i.e., the time from purchasing the new stock to the actual product sale. It is calculated as inventory divided by average sales or cost of sales and multiplied by 365 to know the exact days of inventory conversion into sales.

The high conversion period determines the slow cash conversion cycle and block of money in inventory. In contrast, a decreased conversion period reduces cash conversion cycles and unnecessary money blockage. It takes into account the average amount invested in the stock.

- The inventory conversion period estimates the time that it takes to convert the inventory into sales, which is the time from purchasing the new stock to the actual product sale.

- One may calculate it as inventory divided by average sales or cost of sales and multiply by 365 to understand the inventory conversion into sales exact days.

- The high conversion duration estimates the delayed cash conversion cycle and money block in inventory. A shorter conversion period, on the other hand, reduces cash conversion cycles and unneeded money blockage and takes into account the average amount invested in the stock.

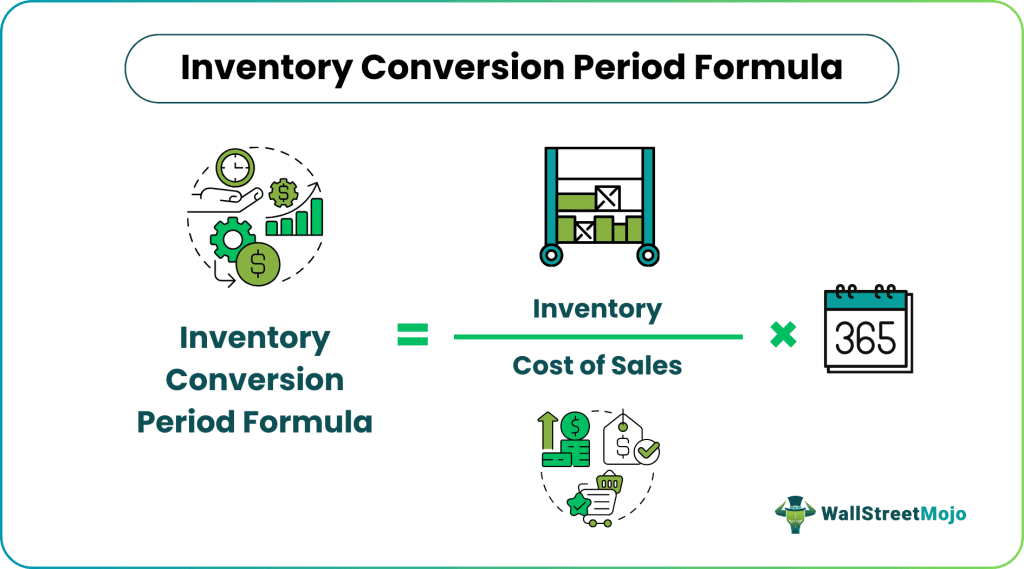

Inventory Conversion Period Formula

The number of days or months the inventory converts into sales determines the cash conversion cycle and improves the conversion period through efficient management and working on loopholes.

The formula is as under:-

Formula = Inventory / Cost of Sales * 365

OR

Formula = Inventory / Sales * 365

OR

Formula = Inventory / Average Daily Sales

Inventory is taken as on the balance sheet date. The cost of sales and average daily sales would be taken as a base for internal calculation purposes to know the exact conversion period. Whereas, for presentation in the financial statement, the net sales for the year would be taken into account so that every reader could understand the analysis and compare it with the industry conversion ratio.

As sales price, less cost of sales is the gross profit margin of the organization. Hence, some organizations do not take the average sales while calculating this period to determine the exact conversion period. In comparison, it is also a fact that the analyst calculates this period by considering sales. It is because it helps readers of financial statements to understand better. Ultimately, the company has to convert inventory into sales; hence, sales are the base for calculating the conversion cycle.

Example

The organization’s inventory, as on the balance sheet date, is $3 million, and average daily sales are $30,000. To calculate the inventory conversion period and determine how one can reduce it?

Solution:

Calculation of Yearly sale:

= $30,000 * 365

= $10,950,000

= 10.95 million

Formula = Inventory/ Sales * 365

- = 3 / 10.95 * 365 = 100 days

i.e. one can convert inventory into sales in 100 days

OR

- Average daily sales : $30,000 / $10,00,000 = 0.03 million

Formula = Inventory/ Average Daily Sales

- = 3 million / 0.03 million = 100 days

One can reduce it by adopting incentives to employees for faster production or just a time approach for inventory.

How To Interpret?

We can interpret the inventory conversion period as determining the number of days one can convert the inventory into sales to assess the average cash cycle and manage it better.

It helps the organization better inventory and purchase management and decides whether inventory is to be purchased or manufactured. And to determine the need for more investment and the return on the same.

Issues

There are two issues involved here: –

- One may calculate the period the inventory converts into sales and cash. But, it ignores that there is a credit period to be allowed to debtors, and that credit period is not included. i.e., its conversion into cash takes longer than determined by calculating the inventory conversion period. It only calculates the time of inventory conversion into sales, not the inventory into cash. The inventory into cash conversion may require more extensive time than sales because of the credit period allowed to debtors.

- While calculating this period assumes that all items are purchased or manufactured in the company. Therefore, the whole inventory management and conversion period can be controlled and reduced drastically if the company goes for outsourcing production.

Frequently Asked Questions (FAQs)

What is a reasonable inventory conversion period?

Most industries’ ideal inventory turnover ratio will be between 5 and 10. The company may sell and restock inventory approximately every one to two months.

How do you find the inventory conversion period?

One may calculate it as inventory divided by average sales or cost of sales and multiplied by 365 to obtain the inventory conversion into sales exact days.

Why is the inventory conversion period critical?

The inventory conversion period is when a company should invest cash when it converts materials into a sale. In addition, closely regulating the conversion period may result in a reduced cash requirement by a business.

What makes up the inventory conversion period?

The inventory conversion period refers to the time needed to get materials, manufacture, and sell the product. Moreover, a company may invest cash while converting materials into a sale.

Recommended Articles

This article is a guide to the Inventory Conversion Period. Here, we discuss the inventory conversion period formula, examples, and interpretations. You may learn more about financing from the following articles: –