What Is The Conservatism Principle?

Conservatism Principle is a concept in accounting under GAAP that recognizes and records expenses and liabilities- uncertain, as soon as possible but recognizes revenues and assets when they are assured of being received. It gives clear guidance in documenting cases of uncertainty and estimates.

The principle of Conservatism is one of the major accounting principles and guidelines listed under UK GAAP, which is a regulatory body of policies and standards of accounting that all accountants across the globe need to follow while reporting the business’s financial activity. The principle of Conservatism is mostly concerned with the reliability of the financial statements of a business entity.

Conservatism Principle Example

Conservatism Principle Example #1

Let us assume that a company XYZ Ltd. is embroiled in a patent lawsuit. XYZ Ltd. is suing ABC Ltd for patent infringement and is expecting to win a substantial settlement. Since the settlement is not a surety, XYZ Ltd. does not record the gain in the financial statements. Now the question is, why does it not record this in the financial statement?

XYZ Ltd. may win, or it may not win the amount it is expecting by winning the settlement. Since a sizable winning settlement amount may lead to complexities in financial statements and mislead users, this gain is not recorded in the books. Again taking the same example, if ABC Ltd. expects to lose the suit, it must record the losses in the footnotes of the financial statements. It will be the most conservative approach because the users will want to know that the company will have to pay out a large sum for settlement in the coming days.

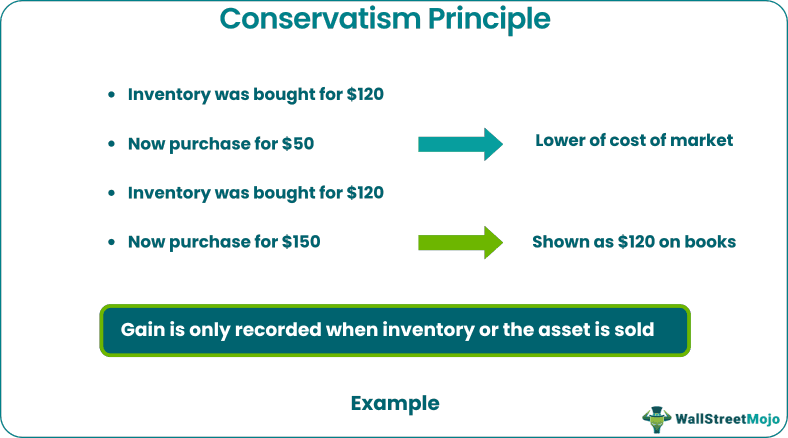

Conservatism Principle Example #2

Suppose an asset owned by an entity like inventory was bought for $120 but can now be bought for $50. Then the company must immediately write down the value of the asset to $50, i.e., the lower the market cost. But if the inventory was bought for $120 and now costs the company $150, it must still be shown as $120 on the books. The gain is only recorded when the inventory or the asset is sold.

Conservatism Principle of Accounting Video

Impact of Conservatism Principle on Financial Statements

- The conservative accounting principle always says that one should always err on the most conservative side of any financial transaction.

- It is done by minimizing profits by stating uncertain losses or expenses and not mentioning unknown or estimated gains. It always indicates that a more conservative estimate should always be followed.

- While doing an estimate for allowance regarding doubtful accounts, casualty losses, or other unknown future events, one should always err on the side of conservatism. Alternatively, we can say that an accountant should record the most expenses and the least income. This principle of conservatism forms the main backbone of the lower cost or market concept for inventory recording.

The conservatism principle of accounting states that the accountants must choose the most conservative outcome when two outcomes are available. The main logic behind this principle of conservatism is that when two reasonable possibilities for recording a transaction are available, one must err on the conservative side. It means one has to record uncertain losses while staying away from recording uncertain gains. So when the conservatism principle of accounting is followed, a lower asset amount is recorded on the balance sheet, and lower net income is recorded on the income statement. So, adhering to this principle will record lower profits in the statements.

Why Follow the Principle of Conservatism?

Why do we use conservatism while recording a business entity’s gains and losses? We must keep in mind that the principle of conservatism does not mean making the recorded earnings as low as possible. This principle helps break a tie when an accountant has to deal with equally probable outcomes for a transaction. When interested users or investors are going through the company’s financial statements, they must get an assurance that the profit of the business coming in is not overestimated. If overestimated, it will be misleading for the company stakeholders. When it follows the conservatism principle of accounting, people like tax prep pros or potential business investors or partners get a more transparent and realistic picture of the company’s financial standing and the company’s future trajectory.

The two main aspects of the conservatism principle of accounting are – recognizing revenue only if they are confident and recognizing expenses as soon as possible.

Why is the Conservative Principle of Accounting called the “Concept of Prudence”

The concept of conservatism is also known as the concept of prudence.

- It is always stated that “anticipate no profit, provide for all losses.” It implies that an accountant must always be cautious and record the lowest possible value for assets and revenues and the highest values for liabilities and expenses. As per this concept, revenues or profits should only be recorded if they are realized with reasonable certainty.

- Provisions must also be made for all liabilities, expenses, and losses- certain or uncertain. Probable losses in respect of all contingencies should also be recorded. So we can safely say that the concept of conservatism helps a business entity to stay safe in the coming days.

- In other words, prudence, which means acting with or showing care for the future, can be synonymous with the conservatism principle of accounting. We can say that the Concept of Conservatism is also known as the Concept of Prudence.

Conclusion

The principle of conservatism is the primary basis for lower of cost or market rule, which says that inventory should be recorded lower than its acquisition cost or the current market value. Following this process leads to lower taxable income and lower tax receipts. The conservatism principle of accounting is only a guideline that an accountant needs to follow to maintain a clear picture of the financial standing of a business entity.

Recommended Articles

This article has been a guide to the Conservatism Principle of Accounting. Here we discuss the conservatism principle in detail, practical examples, and its impact on the financial statements.