Contra Asset Account Definition

A Contra Asset Account is an asset account having a credit balance that is related to one of the assets with a debit balance. When we add the balances of two of these assets together, it reflects the net book value or carrying value of the debit balance assets.

Contra asset account is an important element of the balance sheet or the books of accounts. This is because it tallies two respective debit-credit entry pairs, thereby figuring out the net balance of the asset account.

Key Takeaways

Contra Asset Account Explained

Contra asset account is the asset account with a negative or no balance. This is the reason they are categorized as a contra account as the normal asset accounts have positive or debit balance. These contra assets in the balance sheet are reflected with the asset accounts they are paired with to equalize the balance.

With increasing globalization and companies operating in many countries, the books of accounts must be compatible with a global platform. They are also the result of globally accepted accounting principles for accurately reporting financial numbers. As we have seen in the above discussion, how reporting contra assets accounts helps in a better understanding of the financial statements of any organization. So, an organization looking for a robust accounting process must move to this reporting for better understanding.

Nowadays, with the development of a computerized accounting system, it is easy and quick to prepare the contra asset accounts as the system does all the calculations, and hardly anything is pushed manually. However, an accountant or person in charge must ensure that any change in the value of the assets due to revaluation or impairment must be considered. Accordingly, the value of the contra asset account will change. Also, with IFRS (International Financial Reporting Standards) asking to report it in a particular way, the accountants must be updated with recent changes to how the contra assets account should appear in the books of accounts.

List of Accounts

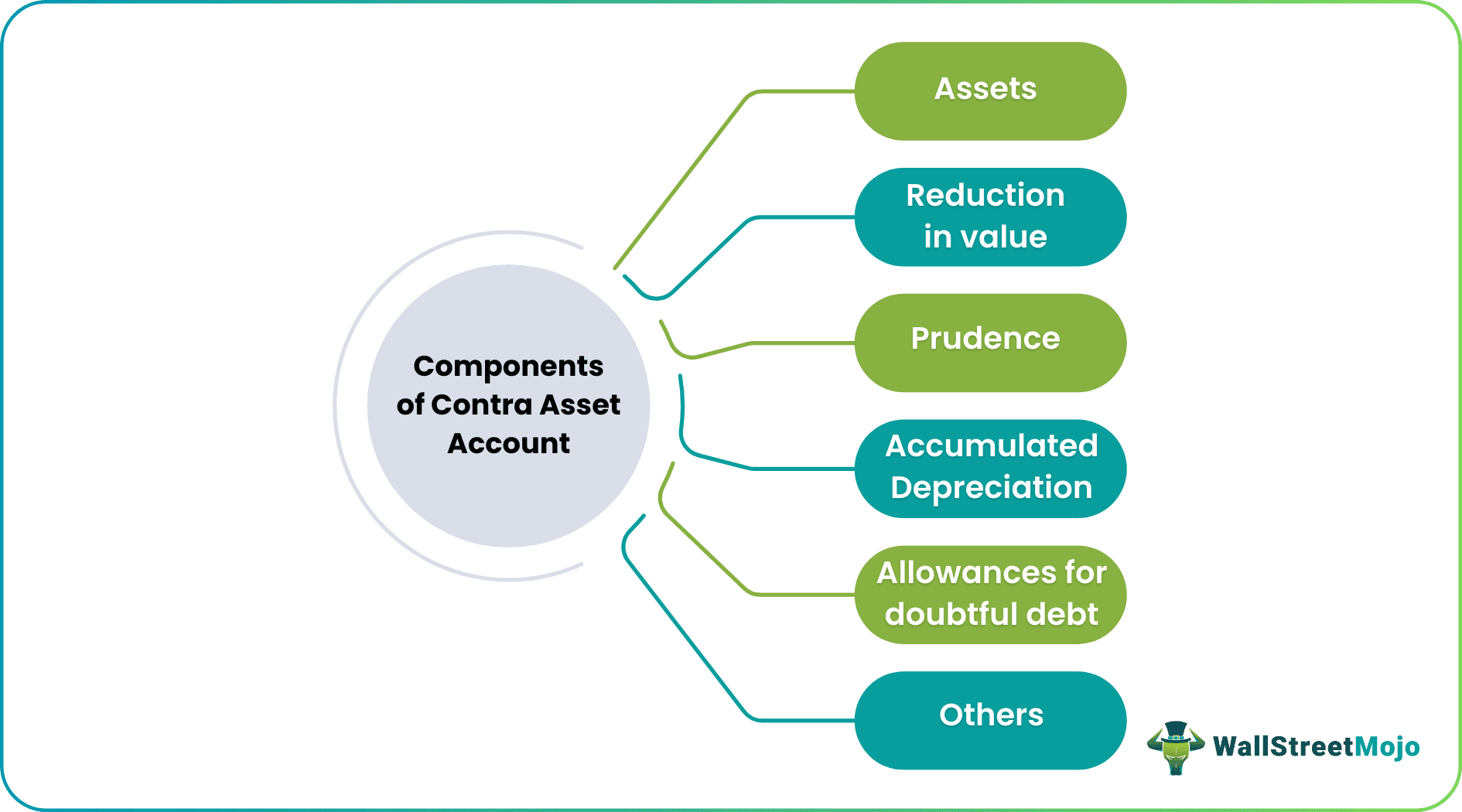

There are various components that constitute these accounts. The contra asset account list includes:

#1 – Assets

It is prepared when there is a reduction in the value of assets due to wear and tear continuous use or when we expect that a certain percentage of accounts receivable will not be received. Fixed assets like plants & equipment are depreciated every year, and this balance is transferred to the accumulated depreciation account. So, in this case, accumulated depreciation is a contra asset account related to plant & equipment.

#2 – Reduction in Value

We know that assets have a debit balance; however, the contra assets account has credit balances. This account shows the balance, which is a reduction in the value of assets. We expect 2% of our total receivable of $100,000 has gone bad. So we show $2,000 ($100,000*2%) as a provision for doubtful debts, which reduces the debtors value and means that only $98,000 is expected to be received from debtors.

#3 – Prudence

It is only prudent to show the reduction or reserve in a separate account, and at any point, it gives us the netbook value explaining what the actual cost was and how much of that has been depreciated. It also helps create reserves, and later any change in the expected number can be adjusted through allowances and reserves.

#4 – Accumulated Depreciation

Whenever an organization buys an asset and depreciates it over the asset’s useful economic life, the reduction in value accumulates over the year, which is called accumulated depreciation. The accumulated depreciation balance cannot exceed the book value of the asset. We get the remaining value of assets by deducting the accumulated depreciation balances from the book value of the asset.

#5 – Allowances for Doubtful Debts

When a good is sold on credit, the amount receivable from customers is shown under the debtor’s balance sheet balance. It is a standard business practice to prepare an estimate for the amount likely to go bad. This amount is shown as a provision or reserve for doubtful debts. The provision for doubtful debts is a contra asset account related to debtors.

#6 – Others

Provision for a discount from creditors and discount on bills receivable are other widely used examples.

Examples

Let us consider the following instances to understand what is a contra asset account and how its entry is accounted for:

Example 1

Suppose a firm has a packaging machine worth $9,000 to pack delicate artifacts. This machine is expected to last for three years. As it is a machinery, the firm knows that its condition would deteriorate with every use. In this case, the total cost of the machine is divided by the possible durability span. This returns the figure – $3,000, which is the accumulated depreciation for the first year. Subtracting the latter from the total cost of the packaging machine, i.e., $9,000-$3,000 = $6,000, which is them the net value.

The accumulated depreciation of $3000 is the contra account as it gets subtracted from the value of the asset. If the accounts receivable is $25,000 and the allowance for doubtful obligations is $3,000. While the accounts receivables is shown in the balance sheet as $25,000, the net value obtained after deducting the doubtful obligation is $25,000-$3,000 = $22,000. Here, the obligation figure is the contra account as it gets subtracted from the asset accounts receivable.

The example above shows how contra asset accounts work for account receivables.

Example 2

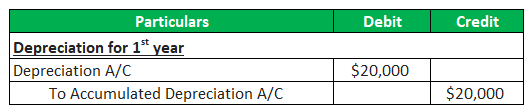

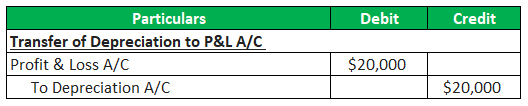

Let us understand how the accounting entry is posted for the contra asset account and how it is shown in the books. Let us consider that ABC Ltd. recently bought machinery for $100,000, and it plans to depreciate the machinery over five years by using the straight-line method. In this case, the depreciation each year for this machinery will be $100,000/5 = $20,000.

Accounting Entry

By the end of the first-year machinery, the balance will be $100,000, and accumulated depreciation will show $20,000. By the end of 2nd-year, the machinery balance will still be $100,000, and accumulated depreciation will show $40,000. The netbook value of the machinery by the end of the first year will be $80,000 ($100,000-$20,000) and $60,000 ($100,000-$40,000) by the end of the second year. This method helps a third person identify what the book value was at the time of purchase and the remaining value of an asset. If we show $60,000 as an asset in the third year, it will be challenging to understand whether $60,000 is all new purchases or the remaining value of an asset. This account helps all the stakeholders understand the financial numbers accurately.

Advantages

Some of the advantages are a follows:

- It helps in the quick calculation of net book value.

- The annual reports are prepared for various parties; some of them might not be accounting versed; they help identify the reduction in total value.

- It helps in audit facilitation and annual filings.

- It is a globally accepted policy.

Disadvantages

Some of the disadvantages are a follows:

- It is a time-consuming process.

- Many organizations find it challenging to implement.

- Need a robust accounting system; else, operational difficulties may arise.

Recommended Articles

This article has been a guide to Contra Asset Account and its definition. Here, we explain it along with examples, list of accounts, advantages & disadvantages. You can learn more about accounting from the following articles –