Bad Debts Provision Meaning

Provision for bad debts is the estimated percentage of total doubtful debt that must be written off during the next year. It is done because the amount of loss is impossible to ascertain until it is proven bad. It is nothing but a loss to the company, which needs to be charged to the profit and loss account in the form of a provision.

Bad debt accounting is a practice of estimating the default from debtors or customers and the potential loss arising due to the same. By creating a provision, lenders can manage the risk by covering losses from doubtful or bad debts. The quantum of this provision depends highly on the lender’s risk appetite and their ability to recover doubtful debts.

Bad Debts Provision Explained

A bad debt provision is a reserve made to show the estimated percentage of the total bad and doubtful debts that need to be written off in the next year. It is simply a loss because it is charged to the profit & loss account of the company in the name of provision.

It is important to understand that debts are categorized into three categories. Understanding them shall act as a basis for our understanding of why passing a bad debt provision entry is vital to curtail potential losses in the business. The categories are:

- Bad Debts: These means which are uncollectable or irrecoverable debts.

- Doubtful debts: These means which will be receivable or cannot be ascertainable at the date of preparing the financial statements; in simple words, those debts are doubtful to realize.

- Good debts: These means which are not bad, i.e., neither there is the possibility of bad debts nor any doubt about their realization is known as good debts.

Provision for bad debts can have a major impact on the financial statement of the company because it directly affects the profit and loss statement of the company, which is always required to give a true and fair view of the financial statements. Therefore, the estimation of the same should be made based on the company’s past performance.

Journal Entries

Let us understand the journal entries passed for different scenarios where the debt from a potential defaulting customer is identified. The bad debt provision accounting process allows the management to prepare for potential losses.

In the First Year

- For Bad debts

- For provision for bad debts journal entries

In the Second/Subsequent Year

- For Bad Debts

- For Provision for Bad Debts Journal entries (If a new provision is more than the old)

How To Calculate?

Now that we understand the basics and the formula relating to bad debt provision accounting, let us understand how to calculate the same through the discussion below.

There are two major ways through which the expenses relate to bad debt provision. They are- 1. Direct Write-off Method, and 2. Allowance Method.

- Direct Write-off Method: Under this method, the bad debts are directly debited from the bad debts account and credited to the account receivables. However, it is vital to understand that this method does not follow the balancing principle which affects the accrual accounting of the company. Following this formula does not require any formula as the amount defaulted will directly be accounted for in the respective account.

- Allowance Method: It is an appropriate method when a large volume of bad debt is involved. Under this method, a company forecasts the incurrence of bad debt from clients and prepares appropriate measures for the same.

A provision account is created to have a pool of money ready to be transferred to trade/account payables in case of default. It is a contra-asset account that reduces the loans receivable on the balance sheet.

Examples

Let us understand the concept of passing bad debt provision entry with the help of a few examples. These examples shall give us a practical overview of the concept and its related factors.

Example #1

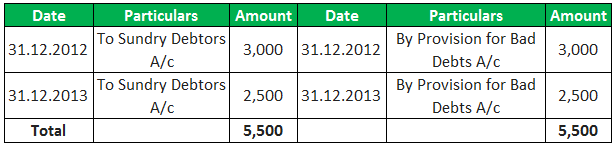

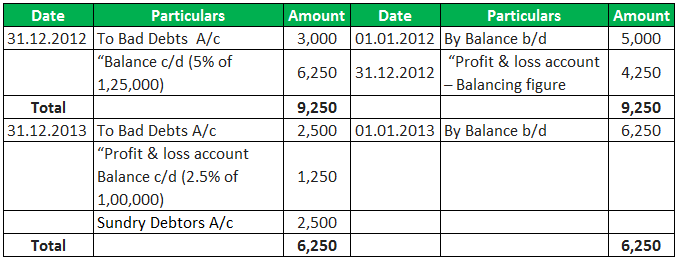

- As on 01.01.2012 Provision for Bad Debts is 5,000 ;

- As on 31.12.2012 Bad Debts written off is 3,000 & Sundry Debtors are 1,25,000;

- As on 12.2013 Bad Debts written off is 2,500 & Sundry Debtors are 1,00,000 ;

- Provision for doubtful debts to be provided for 5% for 2012 & 2.5% for 2013;

- Prepare Bad debts account and provision for bad debts account.

Bad debts Account

Provision for Bad debts Account

Example #2

M/s X Ltd. has a trade receivable of Rs. 10000 from M/s KBC as of 31.12.2018. Recently, a receivable owing to Rs. 1,000 to M/s X Ltd has been wound up. Consequently, M/s X Ltd. does not expect an amount to be recovered from M/s KBC.

Based on experience, M/s X Ltd. estimates that 3% of its receivables will do the default in making the payments. M/s X should write off Rs. 1,000 from M/s KBC as bad debts. Please provide the journal entries to be made for bad debt. Note that the provision for bad debts on 31.12.2017 is Rs. 100.

The entries shall be made as under:-

(An allowance of Rs. 270 (i.e. (Rs. 10,000 – Rs. 1000) * 3%) should be made. A provision of Rs. 100 has already been created earlier. Therefore, only Rs. 170 shall be charged to the income statement.)

Example #3

Let’s assume that, in 2017, we need to create the provision for bad debts @ 15% of the sundry debtors, i.e., $ 1,00,000, as we expect that these debtors will not pay their dues.

So, in the first year, i.e., 2017, we shall pass the following journal entry for provisions of bad debt as under:-

At the end of 2018, we reviewed our sundry debtors, who were $ 1,10,000, and decided to provide the provision again at 15%. Accordingly, this year the provision will increase by $ 1,500 [($ 1,10,000 * 15%) – $ 15,000], and it shall be recorded in the books of accounts as under:-

At the end of 2019, we again reviewed our sundry debtors, who were $ 90,000, and decided to provide the provision again at 15%. Accordingly, this year the provision will decrease by $ 1,500 [($ 90,000 * 15%) – $ 15,000], and it shall record in the books of accounts as under:-

Based on the above, the following are the effects on the income statement:-

- At the end of year 1:- Profit shall be lowered by $ 15,000

- At the end of year 2:- Profit shall be lowered by $ 1,500

- At the end of year 3:- Profit shall be increased by $ 1,500

Recommended Articles

This article has been a guide to what is Bad Debt Provision & its meaning. Here we explain its journal entry, how to calculate its expenses, and examples in detail. Here are the other articles in accounting that you may like –