Part of our Budgeting and Planning guide

Overhead Budget Meaning

Overhead Budget is prepared to forecast and present all the expected costs concerning manufacturing the goods that the company expects to incur in the next year. It excludes the direct material and the direct labor cost, and the information, which becomes part of the cost of the goods sold in the master budget.

Thus, it gives the necessary targets to employees related to expenses. With the budget, employees know the limit of expenditure they could incur on specific activities in a predetermined period, thereby keeping control of the business expenses and getting the desired results set by the management for the business.

Overhead Budget Explained

An overhead budget is plan that helps in outlining the various expenses of the business that are expected to occur in future but are not related directy to the production of goods.

They are recurring in nature, which means they are incurred regularly like rent, insurance, salary, etc. The business has to make a forecast of the expenses in advance so that they can estimate and keep aside the required funds that might be required to meet the expenses. This facilitates financial planning and avoid any unnecessary cash mismanagement.

However, it is to be noted that the business, which has been working for many years, can effectively and accurately prepare an Overhead budget. Then a new business can only prepare a budget using the Overhead forecasting strategies and not by following the past trend.

The preparation of the Overhead budget in the small business is more cumbersome.

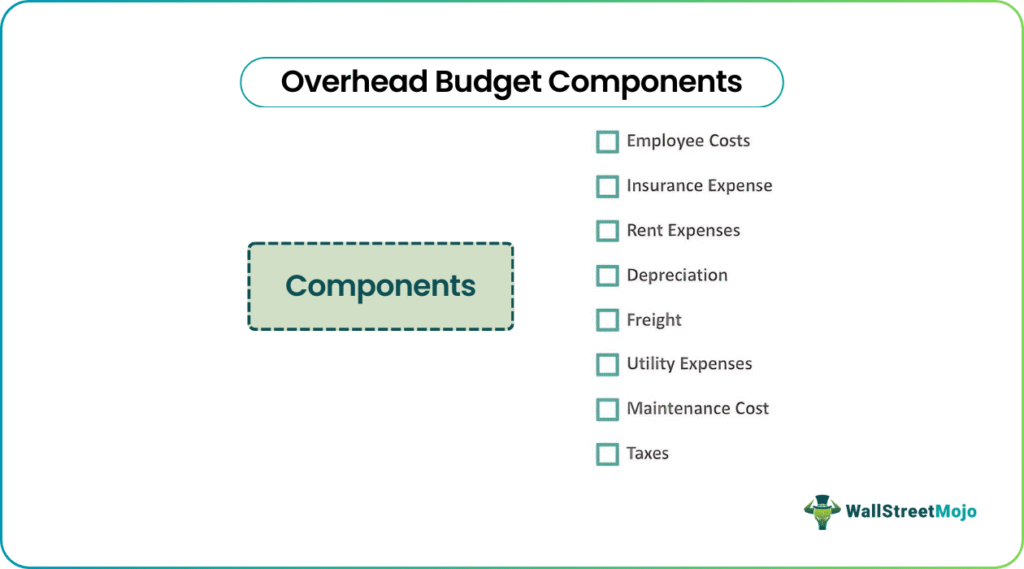

Components

The following are the components of the overhead budget.

#1 – Employee Costs

Employee cost refers to the amount paid to the employee for their work. Overhead budget considers the cost that the company expects to incur on its employees in the next year, like salary, etc.

#2 – Insurance Expense

Insurance expense is the expense incurred by the company for insuring the various things and has to regularly make the payment of its premium. So, these costs that the company expects to incur on insurance premiums in the next year are considered overhead and shown in the overhead budget.

#3 – Rent Expenses

Property used for production is generally taken on the rent by the company, so this rent has to be paid, which becomes part of the company’s overhead. So, these costs that the company expects to incur for paying rent in the next year are considered overhead and will be shown in the overhead budget.

#4 – Depreciation

Depreciation refers to the reduction in the value of fixed assets due to the normal wear and tear, technological changes, etc., which are charged as an expense in the company’s income statement. So, depreciation costs that the company expects to incur in the next year are considered overhead and will be shown in the overhead budget.

#5 – Freight

Freight refers to the charge paid by the companies to transport the goods using any means of transport. It is one of the essential expenses that many companies have to incur, and such freight costs that the company expects will incur in the next year are considered overhead and shown in the overhead budget.

#6 – Utility Expenses

Utility Expenses refers to the cost that the company incurs for availing of the services or facilities provided by public utility companies and include facilities like telephone facility, water, sewer, electricity, gas, etc. These costs are essential for the operation of the business, and all these costs which the company expects it will incur in the next year are considered overhead and will be shown in the overhead budget.

#7 – Maintenance Cost

Maintenance Costs refer to those costs that the company incurs to keep the items in good working condition. These costs are essential for the operation of the business, and all these costs which the company expects it will incur in the next year are considered overhead and will be shown in the overhead budget.

#8 – Taxes

Taxes refer to the compulsory financial charge imposed by the country’s government on the individuals and organizations working there. The company has to pay these expenses compulsorily and is thus considered the company’s overhead expenses. Therefore, all these costs that the company expects to incur in the next year are considered overhead and shown in the overhead budget.

Apart from these costs, all the expected costs regarding manufacturing the goods that the company expects to incur in the next year, except the cost of direct material and the direct labor cost, will be considered while preparing the overhead budget.

How To Calculate?

There are some important steps to calculate the budget, as given below:

- Identify overhead expense – The first step in making the budget is to understand and identify all overhead expenses that the business may incur during a period.

- Estimate the amount – It is crucial to estimate the amount of all the overhead expenses at best and as accurately as possible. This may be done using the market trends, the past data, etc.

- Allignment with goals – Then the business should review whether the amount estimation is aligned with the objective of the entity.

Thus, the above steps will lead to a successful creation of an overhead budget which should be followed strictly to maintain the proper financial planning.

Example

XYZ ltd manufactures different products and makes the forecast related to the overhead expenses for the upcoming year, which ends in December 2020. It forecasted that the employee costs in the next year would be $ 10,000 in quarter 1, $ 12,000 in quarter 2, $ 12,000 in quarter 3, and $ 14,000 in quarter 4. In addition, Insurance expense, rent expenses, and depreciation expenses are expected to remain fixed for all four quarters at $ 6,000, $ 9,000, and $ 10,000 per quarter.

Utility expenses forecasted for the next year would be $ 5,000 in quarter 1, $ 7,000 in quarter 2, $ 6,000 in quarter 3, and $ 7,000 in quarter 4, and the income tax expenses forecasted for the next year would be $ 3,000 in quarter 1, $ 3,000 in quarter 2, $ 4,000 in quarter three and $ 4,000 in quarter 4

Prepare the necessary Overhead Budget of the company XYZ ltd for the coming year ending in December 2020.

Solution

Following is the Overhead budget of XYZ ltd for the year ended on December 31, 2020.

Advantages

Thus in the above example, the Overhead budget prepared shows calculations regarding the various expenses forecasted by the company.

The different advantages related to the Overhead Budget are as follows:

- With the budget, employees know the limit of expenditure that they could incur on specific activities in a predetermined period, thereby keeping the control of the business expenses and getting the desired results set by the management for the business.

- It helps allocate the business resources to different goods and services efficiently and effectively.

Disadvantages

The disadvantages related to the Overhead Budget are as follows:

- Preparation of the Overhead budget is a time-consuming process that needs time management and effort.

- It is based on management judgment and estimations, so the effective and accurate forecast of the overhead and expense is generally impossible in today’s scenario and this competitive and sometimes unpredictable market.

So, it is necessary to be informed about the procedure’s pros and cons so that it can be taken care of and put to use in an optimum way.

Recommended Articles

This article is a guide to Overhead Budget and its meaning. Here we discuss components of the manufacturing overhead budget and examples, advantages, and disadvantages. You can learn more about finance from the following articles –