What Is A Budget Committee?

A Budget Committee is an internal group of an organization that ensures responsible spending and resource allocation. Its purpose is to ensure the organization’s financial sustainability and success by managing resources effectively and responsibly.

The Committee ensures that budget allocations align with the organization’s overall vision and mission, directing resources toward activities that drive strategic goals. It provides a platform for different departments to communicate their financial needs and priorities, fostering understanding and collaboration.

- The budget committee serves as a pivotal entity within an organization, entrusted with the creation, oversight, and management of financial matters.

- Its purpose revolves around formulating, evaluating, and approving budgets across various departments or divisions. It entails establishing guidelines and frameworks that align with the organization’s objectives while considering fiscal constraints and priorities.

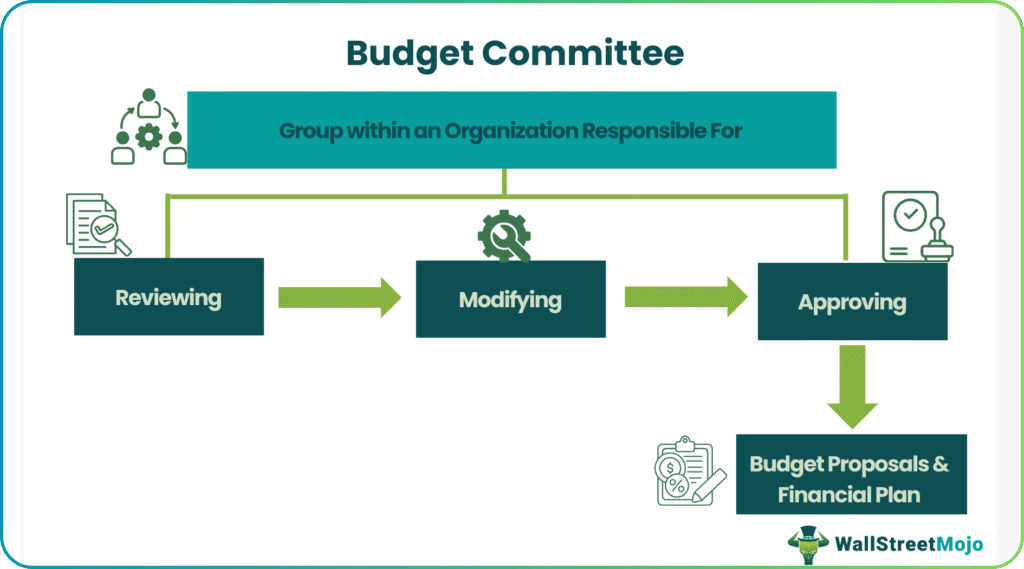

- One of its fundamental functions involves assessing budget proposals submitted by different segments of the organization.

- It ensures that the allocated resources align with strategic goals and financial boundaries, fostering prudent allocation and utilization of funds.

Budget Committee Explained

The Budget Committee assumes a critical role as a guardian of fiscal responsibility. Composed of key decision-makers, they meticulously analyze and adjudicate departmental budget proposals, ensuring alignment with strategic objectives and prudent resource allocation.

Their purview extends to evaluating capital expenditure requests, guaranteeing optimal utilization of investment capital. Upon finalizing the budget, the Committee transitions to a monitoring role, meticulously comparing actual financial performance against established benchmarks. Their proactive intervention ensures deviations from planned outcomes are swiftly addressed, safeguarding organizational stability and fostering sustainable growth.

The Committee holds a distinct viewpoint as they possess comprehensive knowledge of an organization’s financial activities. They have an overarching understanding of the entirety of financial operations, unlike individuals within specific departments who are limited to their departmental scope.

Their purview extends beyond siloed departmental views, offering a comprehensive understanding of the organization’s financial dynamics. This consolidated perspective allows them to analyze overarching patterns, assess resource allocations across diverse sectors, and effectively guide decision-making processes toward fiscal prudence and optimal resource utilization. As custodians of the complete financial narrative, the Committee and allied financial departments play a pivotal role in steering the company toward sustained financial health and strategic stability.

Functions

The functions of the budget committee are listed below-

#1-Assisting Line Mangers for Forecasting

By providing historical data, the budget committee aids line managers in making informed projections and forecasts. This historical perspective serves as a valuable reference point for anticipating future financial trends and requirements.

#2-Reviewing Budget Estimates

The Committee receives and meticulously assesses the budget estimates submitted by various departments to make further recommendations on resource allocation and improve overall effectiveness.

#3-Approving Revised Budgets

Upon necessary revisions and adjustments, the Committee approves the finalized budgets, ensuring they adhere to organizational goals and guidelines.

#4-Identifying Responsibilities and Recommending Corrective Actions

In cases of poor performance, the Committee identifies responsible parties and recommends corrective actions to rectify deviations and ensure adherence to budgetary goals.

Roles And Responsibilities

The roles and responsibilities of the budget committee are as follows-

#1-Estabilishing Budget Guidelines and Policies

One of the foundational roles involves setting up the framework and regulations governing budget formulation. These guidelines are designed to reflect the organization’s objectives, priorities, and financial limitations, ensuring a cohesive approach to budget development.

#2-Assessing and Evaluating Budget Proposals

The Committee diligently scrutinizes and evaluates budget requests originating from diverse departments or teams. This rigorous assessment aims to ascertain alignment with the organization’s overarching strategic objectives and financial boundaries.

#3-Oversight, Monitoring, and Reporting

Throughout the budget duration, the Committee remains vigilant in monitoring budgetary performance. They meticulously track variances, analyze deviations, and generate detailed reports for senior management or the board of directors. When necessary, they propose adjustments or corrective measures to ensure the organization stays on course to meet its financial goals.

#4-Driving Continuous Enhancement

A vital aspect of the Committee’s role involves the constant refinement of the budgeting process. They actively seek out inefficiencies and opportunities for improvement, implementing best practices to elevate the organization’s financial planning and management practices.

Examples

Let us look at some examples to understand the concept better –

Example #1

Consider a company named Evergreen Electronics, where the budget committee oversees budget formulation and allocation across its departments. At the onset of the fiscal year, the Committee evaluates financial projections and decides to allocate $2 million across various divisions.

The research and development (R&D) department proposes an innovative project to develop cutting-edge technology for a new product line. Following the guidelines in the budget manual, the Committee earmarks $800,000 for R&D initiatives, with $500,000 specifically designated for new product development.

The Manufacturing Division requests $600,000 to optimize production efficiency and upgrade equipment. The Committee allocates $400,000 to support these enhancement efforts, ensuring steady operational advancements.

The Sales and Marketing Division seeks $400,000 to launch an aggressive marketing campaign aimed at expanding market reach. The Committee grants $300,000 to bolster marketing strategies and penetrate new customer segments effectively.

Meanwhile, the Administrative Division requires $200,000 to cover overhead expenses and administrative functions. The Committee allocates the requested amount, ensuring smooth administrative operations company-wide.

Throughout the fiscal year, the budget committee diligently monitors expenditure patterns, regularly comparing them against allocated budgets. Observing that the R&D department’s expenses for the new product development are surpassing projections, the Committee reviews the situation. They engage with the R&D head to analyze cost overruns and recommend adjustments to ensure the project’s financial feasibility without compromising the company’s overall fiscal health.

Example #2

The Bellows Falls Union High School budget committee has approved a 3.5% increase, slashing the initial 7.7% proposal in half. This reduction, commended by committee members Clark and Stack, was achieved by Principal Kelly O’Ryan’s responsiveness to suggestions, retaining the dean of students while cutting the assistant principal role and consolidating staff positions in programs like dropout prevention.

Their aim for fiscal responsibility didn’t involve any layoffs, and the committee unanimously endorsed this 3.5% budget, emphasizing its alignment with inflation rates and its careful consideration amidst financial challenges faced by the community.

This real-world example demonstrates how a budget committee strategically allocates funds, monitors expenditures, and navigates unforeseen financial challenges to uphold fiscal responsibility and support departmental objectives within the organization.

Frequently Asked Questions (FAQs)

1. How many members are in the budget committee?

The composition of a budget committee can vary significantly based on the legislative body or organization it is part of. For instance, in the United States Congress, the House Budget Committee is generally made up of a larger group of members representing various congressional districts and political affiliations. In contrast, the Senate Budget Committee typically has a smaller membership. The precise number of members and the Committee’s makeup is determined by the rules and procedures of the governing body or institution to which the Committee belongs.

2. When was the budget committee created?

The Budget Committee was established to oversee and manage the federal budget process. The exact date of its creation varies depending on the legislative context, but in the U.S., it was formed as part of the Congressional Budget and Impoundment Control Act of 1974.

3. What are the subcommittees of the budget committee?

The budget committee has various subcommittees, each focusing on different aspects of budgetary oversight. These subcommittees can include areas such as revenue and taxation, government expenditure, and fiscal policy, but their specific titles and functions can vary depending on the governing body.

Recommended Articles

This has been a guide to what is a Budget Committee. Here, we explain the concept along with its roles & responsibilities, functions, and examples. You can learn more about financing from the following articles –