Part of our Budgeting and Planning guide

Zero-Based Budgeting Definition

Zero-based budgeting starts from zero and does not consider historical data. The income is categorized into fixed costs, variable costs, and savings in such a manner that the balance results in a zero.

Each expense item is evaluated from scratch and is taken only when its impact is justified—based on current requirements and activities. Since there is no reference point if managers want to invest more in marketing, for example, they can. They are starting from a zero, after all.

Key Takeaways

- Zero-based budgeting (ZBB) can be used for monthly, quarterly, semi-annual, and annual budgets. Managers start from a nil balance and do not take the previous year’s budget into account.

- Individuals, families, and companies can formulate zero based budgets.

- ZBB aims at cost-effectiveness. Every budget item becomes the direct result of profit generation. For example, if the human resources department doesn’t make much profit for the last few years, it will get less funding for the next year.

How Zero-Based Budgeting Works?

Zero-based budgeting (ZBB) identifies irrelevant costs incurred by a business. The ZBB method is applied along with other costing techniques—process costing, unit costing, etc.

In the 1960s, Peter Pyhrr was hired by Dallas-based; Texas Instruments where he proposed zero-based budgeting. In 1970, he presented the concept at Harvard Business Review, and In 1977, he published Zero Based Budgeting.

The steps of Zero-based budgeting process are as follows:

- Begin budgeting with zero balance.

- Decide the objective of budgeting.

- Analyze business activities.

- Study the budget components to determine the relevance of expenses, cost reduction, and the scope for saving.

- Prioritize the activities that need cost reduction.

- Finalize a budget plan.

- Prepare a report and convey roles, responsibilities, and activities to relevant parties.

Features

The prominent characteristics of zero-based budgeting that differentiates it from the other budgeting methods are mentioned below:

- Every zero based budget starts afresh, i.e., with a zero balance.

- All the departments of a business entity together take the budgeting decisions.

- It focuses on cost reduction.

- Such a budget can be modified or adjusted with time.

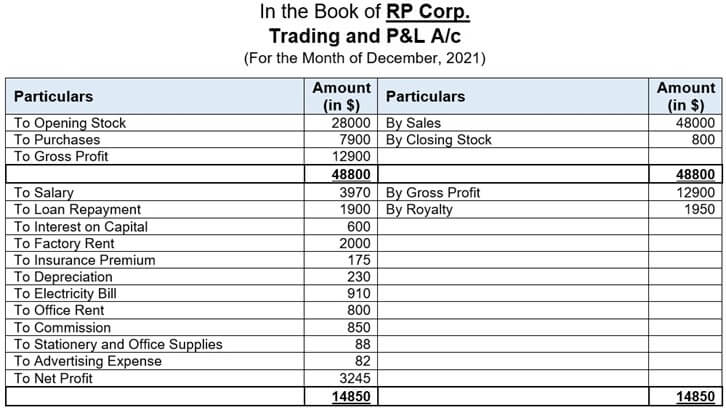

Zero-Based Budgeting Example

RP Corp. is a bag manufacturing company. RP Corp’s monthly Trading and P&L A/c is as follows:

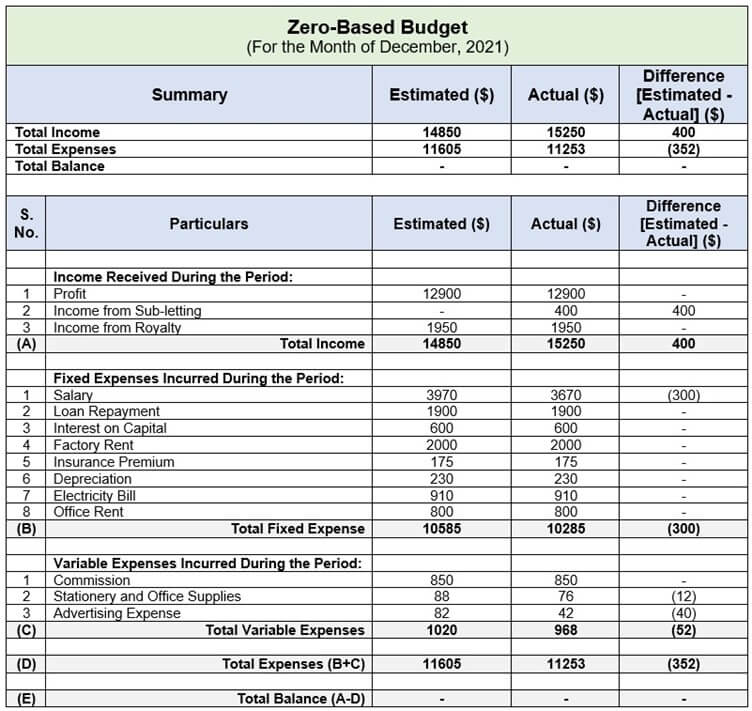

To improve the budget, the manager strategized the following:

- The company doesn’t require two people to work on a machine—salary costs can be reduced by $300.

- An unoccupied factory space can be sub-let to a zip manufacturing partner—saving $400.

- Social media advertising can replace banner ads to save another $40.

- Many records can be maintained electronically to reduce the stationery expenses by $12.

Now, using the given information, prepare a zero-based budget of RP Corp. for December 2021.

Solution:

You can make use of the following, excel template:

The zero-based budget template

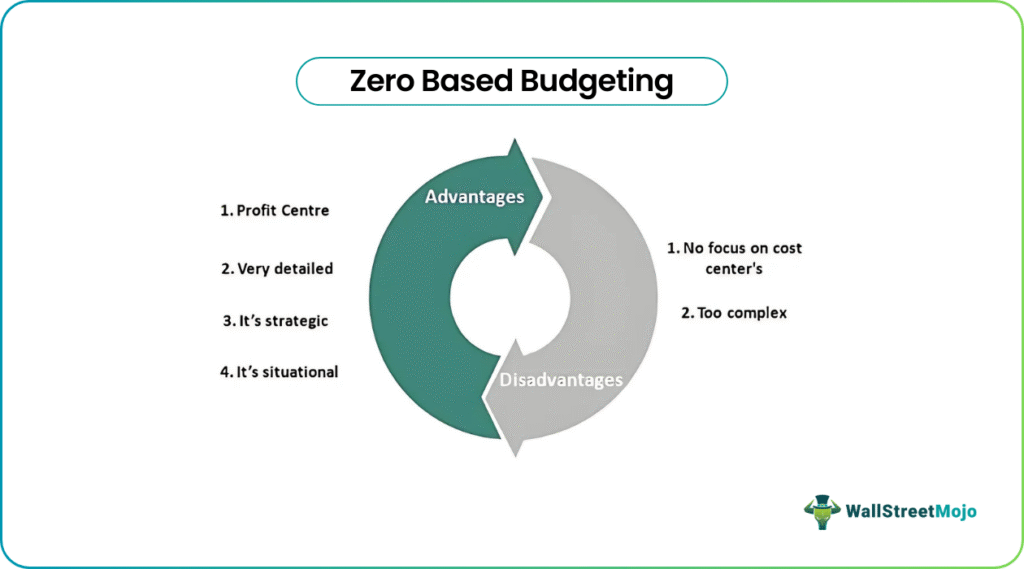

Zero-Based Budgeting Advantages

It has the following advantages:

- Profit Centric: This budgeting technique focuses on cost efficiency and proper allocation of its resources. Moreover, it emphasizes eliminating irrelevant costs or expenses.

- Brings Efficiency: The zero-based approach reduces errors—managers check for unnecessary expenses and activities. Businesses review processes and replace existing SOPs with more effective methods, if and when required.

- Tackles Budget Inflation: It doesn’t consider historical data for preparing the current budget. Instead, it accounts for real-time data and avoids incremental budgeting.

- Improves Coordination: In ZBB, every department plays a role. Collaborative decision-making facilitates transparent communication and better coordination among departments.

Disadvantages

The following disadvantages of ZBB cannot be overlooked:

- Profits Overemphasized: Every budgeting item becomes the direct result of whether it generates profits or not. For example, if the human resources department doesn’t make much profit for a few years, it will get less funding in the ZBB method.

- Consumes Time and Manpower: ZBB requires a lot of effort—managers and employees from different departments are involved. It is, therefore, very labor-intensive. In addition, the collection and interpretation of data take a lot of time.

- Requires Expertise: The budgeting method demands a lot of mathematical, accounting, and analytical knowledge.

- Centralizes Cost: Since it focuses on the cost factor and its reduction, essential objectives like product quality and customer service get compromised.

- Doesn’t Consider Sudden Expenses: This method fails to estimate immediate or emergency expenses.

- Confusion: When too many departments and individuals are involved, the inputs are often contradictory.

Frequently Asked Questions (FAQs)

How to do zero-based budgeting?

First, the budget planner needs to identify the purpose of budgeting. Consequently, a new budget is created from zero. Next, managers analyze fixed costs and variable costs for relevance, effectiveness, and the scope for saving. Finally, a budget report is sent to relevant parties.

Why is the zero-based budget the most effective type of budget?

ZBB is more realistic than other approaches. It ensures real-time income allocation to various business expenses and savings. Most other methods use outdated historical information. Therefore, ZBB is the most efficient form of budget preparation.

How does zero-based budgeting differ from traditional budgeting?

Zero-based budgeting is the creation of a budget from scratch, without considering the previous year’s budget. Traditional budgets, on the other hand, rely on historical data and perform incremental budgeting.

Recommended Articles

This article has been a guide to zero-based budgeting & its meaning. We discuss its features, process, examples, steps, advantages & disadvantages. You may have a look at the following articles to learn more about budgeting –