Part of our Budgeting and Planning guide

What Is Strategic Budgeting?

Strategic Budgeting is a budget prepared by the companies that consider long-term objectives and costs that take more than one year to achieve. It involves preparing multiple budgets and forecasts for short-term costs aligned with the long term. And after that, allocating and categorizing funds depending on the activities.

Since it is related to the long term, which is more than a year, there are lots of criteria to be taken into consideration, and it also involves a very planned approach towards the allocation of suitable resources. The management has to maintain strict supervision regarding monitoring any deviations for the planned structure and value so that the required objective is attained within the planned time.

Strategic Budgeting Explained

The concept of strategic budgeting explains the process of allocation of resources in a strategic, productive, and planned manner, along with focus on the attainment of the required objective of the organization that will be aligned with overall growth and development.

Such a process of strategic planning and budgeting requires professionals with skill, knowledge, and technical experiences who have the ability to chalk out plans and procedures to lead the organization toward a bright future. The resources should be allocated in such a way that they are effectively utilized for the betterment of the business and at the same time, implement methods to control cost and risk, which are some of the main elements of framing an effective strategy. In the process of strategic budgeting, the flowing steps or ideas are implemented.

- There are annual operating short-term plans to achieve a long-term goal eventually. A long-term strategic plan usually spreads out the 5-year plan to set goals. Similarly, Strategic Budgeting manifests the annual plan details and allocates funds to specific areas.

- Spending and the areas have to be in sync. Otherwise, the company might spend on short-term projects without results or unaligned with long-term goals.

- If the company modifies the long-term strategic plan, it can change the strategic budget accordingly to meet the needs.

- It can be very crucial to the company for effective planning and prioritizing. The costs have to be prioritized to satisfy the stakeholders. Usually, the areas with the highest dollar allocation come in high-priority tasks.

Methods

Here are some important methods that are followed to implement the concept of strategic planning and budgeting. Let us study them in detail.

- Incremental budgeting – Just as the name suggests, this approach is incremental in nature, or takes into consideration the various increase in financial figures related to overall cost, inflation, inflow and outflow of cash, etc. In this process, the value of the previous year’s budget is taken into account and then they are edited or adjusted to get the budgetary figures of the current year’s situation. This process is comparatively simple to frame and implement within the financial system of the company. However, this sometimes may miss accounting for any new opportunities, short-term issues, and expenditures, or other changing financial landscapes.

- Activity based budgeting – This helps in designing and tracking the organizational activities that help in achieving the aim of the business. This is a great process that can be successfully used to identify loopholes, deviations and inefficiencies and correct them on time. This improves the business performance for long term. But this method requires time and cost because it need collection of data relate to the past and present and also a detailed analysis of the same.

However, in both of them, a long term objective comes into play, so that attainment of goal related to strategic budget and audit will involve innovation, growth, expansion and proper financial stability through clear and transparent strategies which should be communicated to all individuals concerned so that everyone get the chance to contribute their best in the form of idea and effort.

Examples

Here are some common examples to understand the concept of strategic budget planning.

- Product Development – This is the department that works on years of research and development to design and launch a product. So having a long-term budget helps the product team allocate their resources wisely.

- Programs – As discussed earlier short-term programs and stepping stones to achieve the long-term goals, a strategic budget planning plays a vital role here for both. For instance, an aeronautics company takes ten years to develop a rocket. So in this long tenure, this budget helps them achieve their end goal.

- Infrastructure Budgets – These projects can develop a nation, city, or any organization. If the projects are long-term and may take several years to complete, like railways or national highways, a long-term budget always helps to function.

- Productivity and Capability – Most of the organizational goals are long-term. However, if there are any process-centric changes like an adaptation of new technology, risk management, and many more, the strategic budget allocates for such needs too.

Process

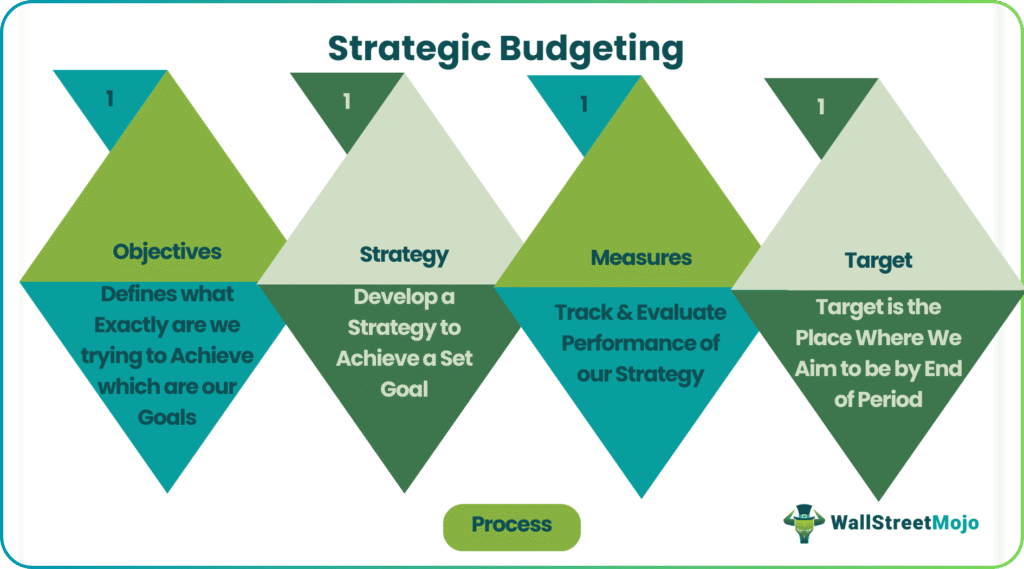

There are four dimensions of strategic budget and audit we need to look for when we are converting the goals into a budget. That is Objectives, Strategies, Measures, and Targets. Let us define these step by step, which helps design the strategic budget.

- Objectives – This defines what we are trying to achieve, which are our goals.

- Strategy – The second step would be to develop a strategy to achieve a set goal.

- Measures – After implementing the strategy, we need to track and evaluate its performance using relevant standards.

- Target – Finally, the goal is where we aim to be by the end of the period.

In the process, we need to allocate funds to all the functional departments and help them achieve their objective to achieve the final target. Significant steps in designing the budget would be as follows –

- Forecast the short-term cost and factorize them into the budget

- Allocate categorized funds depending on the activities

- Make multiple budgets for the short term, which align with the long term ones.

This concept, no doubt, has a lot of importance or benefits for the business. It is an effective path to channelize effort and resource towards the most useful and productive initiative so that resource allocation takes place for the most efficient objective. It also lead to investment prioritization, where the management will use strategy to select the best possible option to invest the funds so that the business gets lucrative returns that can be reinvested for many other purposes.

Such strategies also help in identifying new opportunities and using them. In this way, it is possible for any company to not only sustain, but also evolve, flourish and stay competitive in the market and gain the faith and trust of customers in the process. While framing strategy regarding budgetary plans, it is important that the management has good decision-making skill, are they are the ones who keep the interest of the organization above their own. This will ensure correct decision making that will result in creation of a sustainable future for the company.

A Strategic budget is an essential element for any organization. It provides a long-term road map for the success of the company. A company with a long-term vision and goals must be very constructive and accurate in designing such a budget.

Strategic Budgeting Vs Strategic Planning

The above are important concepts related to planning and budgeting within the organization. However, there are some differences between the two concepts, as given below:

- The strategic budgeting process is particularly related to financial planning and allocation of financial resources in a tactical or calculated manner so as to achieve the desired results. But the latter is related to framing steps and generating ideas related to not only finance, but every area of the organization, for attainment of objective.

- The former will ensure smooth cash inflow and outflow along with keeping track of the sources and uses of funds within the business, whereas the latter ensures generation and implementation of ideas that will help the business to develop from all areas.

- The former looks after the financial efficiency and effectiveness in the use of funds, but the latter looks after the operational efficiency of the company.

- The strategic budgeting process will take into consideration the income, expenses, project funding and return, profitability, debts and liabilities and so on, but the latter will consider the political, social and economic atmosphere outside the organization, efficiency of labor, technological development, investor relation, customer satisfaction, etc.

Thus, the above are some important differences between the two concepts.

Recommended Articles

This article has been a guide to what is Strategic Budgeting. We explain it with examples, process, methods & differences with strategic planning. You may learn more about financing from the following articles –