Part of our Budgeting and Planning guide

What Is A Budget Cycle?

A budget cycle represents the timeframe covered by an entire budget, and its structure varies between corporations and governments. Corporations utilize monthly, quarterly, or annual budget cycles to oversee business operations, costs, and administrative functions. Government agencies employ budget cycles to manage the broader economic structure.

Budget cycles are not rigid; their periodic formulation allows organizations to adapt to changing economic landscapes and market dynamics. This flexibility ensures that budgetary decisions align with the current financial climate, enabling businesses and governments to stay responsive and strategic in resource allocations.

- The budget cycle represents the time frame for preparing, approving, and executing corporate and government budgets.

- Budgets contain critical information about cash inflows and outflows, income sources, revenue generation, and fund allocation.

- The difference between a budget cycle and a budget period is that the former involves planning, approval, and execution, while the latter is the actual timeframe the budget applies to.

- The cycle typically starts before the accounting period and extends beyond it, making it longer than the company’s accounting period.

Budget Cycle Explained

The budget cycle denotes the duration during which a specific budget is devised, encompassing funds, revenue sources, projects, planning, and objectives. Economists and analysts typically focus on two types of budgets: corporate budgets for businesses and political budgets created by governments to govern a country. No budget is permanent; each follows its budget cycle. The extent of planning and the frequency of budget cycles depend on a business’s size and financial health.

Defined by its cyclical nature, the budget cycle facilitates operational processes, fund allocation, and growth tracking, ensuring overall efficiency and accountability. It involves research, historical data, estimations, revenue considerations, project requirements, and infrastructure needs- all managed through comprehensive accounting. The effectiveness of a budget cycle process is subjective, relying on weeks of planning, execution, and continuous revision to gain approval from the board of directors.

The cycles remain dynamic, with companies and governments consistently engaged in either revising the existing cycle or preparing for the next one. The process involves all phases of establishing the budget, creating a continuous cycle of refinement and adaptation.

Phases

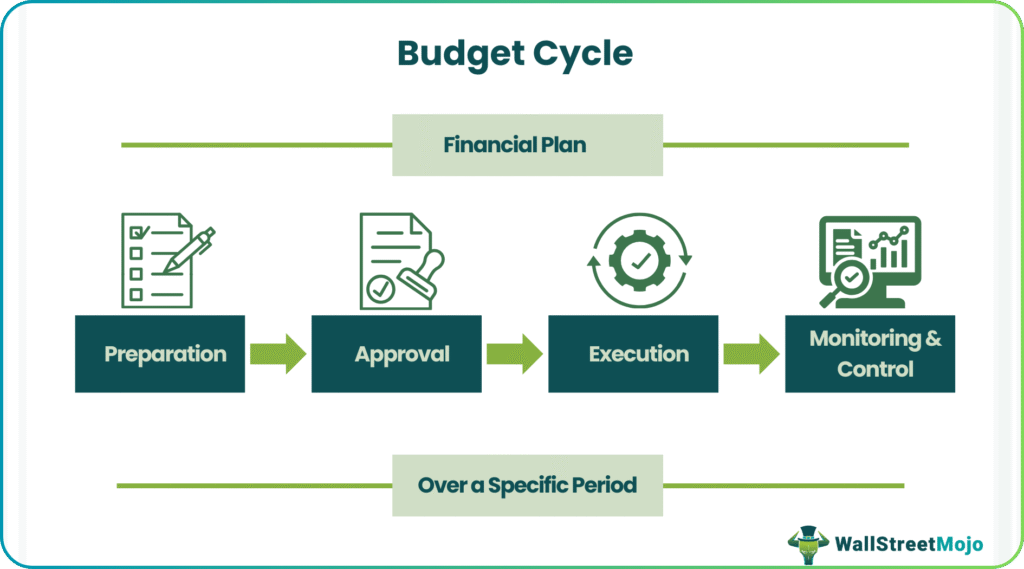

In both corporate and government administration, the budget cycle unfolds in four distinct phases:

- Preparation: The initial step involves crafting a budget for the upcoming period, usually annually, though companies may tailor it based on short-term goals. This phase includes determining fund requirements, strategically allocating resources to different departments, and evaluating the outcomes of the preceding cycle.

- Approval: The formulated budget undergoes scrutiny by board members, executive directors, and chief business officers for corporate budgets. In the case of government budgets, the finance ministry presents them for approval. Corporate budgets typically receive a straightforward yes or no, while political budgets often involve extensive debates.

- Execution: Following approval, funds are released, initiating the allocation and circulation process. Despite meticulous planning, there’s room for revenue adjustments and final implementation. This phase, more complex in government budget periods, involves the gradual flow of funds into designated departments. Small businesses handle all four phases independently to minimize interference and streamline operations.

- Monitoring & Control: Post-execution, the process endures, necessitating revisions even for simpler budgets. Corporate and government audits occur periodically, with management overseeing and guiding the entire process. The monitoring and control phase, crucial in ensuring effective fund utilization, verifies that allocated resources have reached their intended destinations and are being appropriately utilized.

Examples

Let’s look into a few budget cycle examples:

Example #1:

Suppose ABC is a tech startup envisioning rapid growth and product innovation. In the budget cycle’s preparation phase, the startup meticulously plans for development and marketing needs, estimating the funds required. Upon board approval, funds are allocated, marking the execution phase where the startup actively implements its outlined strategies. Through continuous monitoring and control, the startup ensures efficient fund utilization, paving the way for sustained innovation, growth, and adaptability in a fiercely competitive market.

Example #2:

Suppose a city municipality is gearing up for its annual budget cycle. In the preparation phase, the municipality thoroughly assesses community needs, estimating funds required for essential projects such as road repairs, waste management, and public services. Post-approval, the budget guides the execution phase, releasing funds for these crucial initiatives. The monitoring and control phase diligently oversees fund usage, ensuring transparency, preventing misuse, and fostering a well-managed community where taxpayer funds contribute to sustained development.

Importance

Budget cycles are vital for effective planning, financial control, and optimized resource utilization in government and corporate sectors. Let’s look into some points explaining budget cycle importance:

- They are crucial for planning and executing projects, operations, and infrastructure development in designated areas.

- Federal budget periods enable governments to comprehend and regulate revenue sources for potential increases.

- Continuous improvement and revision of budgets over time ensure optimal fund utilization.

- Both government and private corporations use it for cost control and system establishment.

- It aids companies in achieving targets, tracking expenses, and allocating funds for accounting purposes.

- Every budget cycle has specific objectives, whether for companies or government systems.

- It elucidates why a particular department or region requires funds and how allocations meet those needs.

- Governments often introduce new policies within budget cycles to address market problems, inflation, etc.

Frequently Asked Questions (FAQs)

1. What are the common types of budget cycles?

Common types of budget cycles include annual, biennial, and rolling budgets. Annual budgets cover one fiscal year, biennial budgets span two years, and rolling budgets continuously update over a set period, typically involving ongoing forecasting and adjustments.

2. How does the budget cycle in the hotel industry work?

In the hotel industry, the budget cycle involves meticulous planning for operational expenses, capital investments, and revenue projections. It includes preparing budgets for various departments, gaining approval, executing plans, and constant monitoring to ensure financial goals align with the dynamic hospitality landscape.

3. How to reduce budget cycle time?

To reduce it, businesses can leverage technology for streamlined processes, adopt agile budgeting methodologies, automate data collection and analysis, and encourage collaboration among departments. Streamlining workflows and embracing efficient tools can lead to quicker and more responsive budgeting cycles.

Recommended Articles

This has been a guide to what is a Budget Cycle. Here, we explain the topic in detail, including its phases, examples, and importance. You can learn more about financing from the following articles –