Part of our Budgeting and Planning guide

What Is Incremental Budgeting?

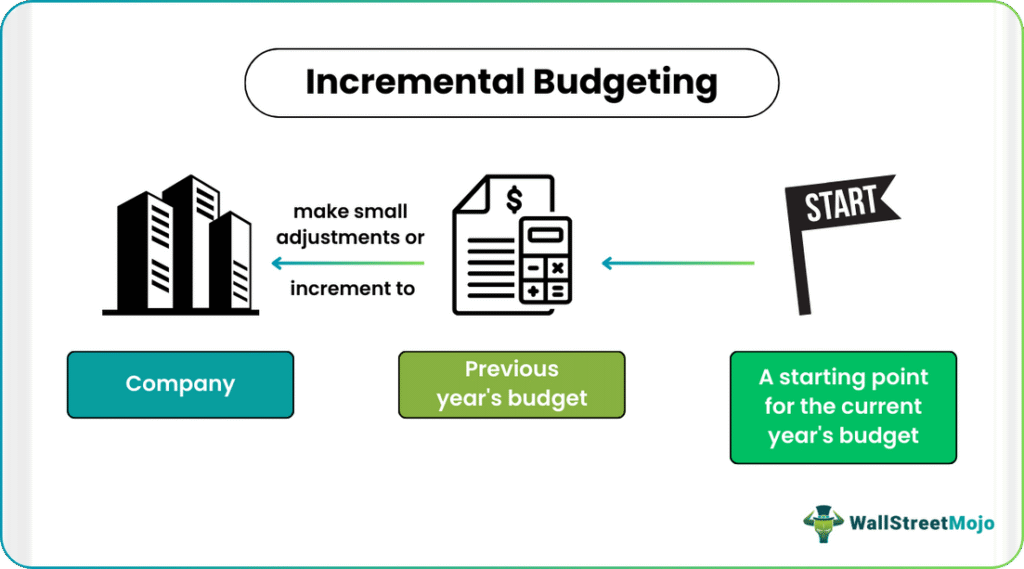

Incremental budgeting is a method where the budget for the upcoming period is based on the budget from the previous period, with adjustments made for changes in costs, revenues, and other factors. The budget is incrementally increased or decreased from the previous period’s budget based on the expected changes.

This approach is typically utilized in organizations with relatively stable budgeting processes and few major year-to-year changes. Furthermore, it is also commonly employed in public sector organizations, where budgets often build upon the previous year’s budget, incorporating adjustments for changes in funding, policy priorities, and operational needs.

- Incremental budgeting involves starting with the previous year’s budget and making incremental changes for the upcoming year.

- This approach is known for its simplicity, stability, and predictability in budgeting.

- The primary advantage is its simplicity and ease of implementation, as it doesn’t necessitate a complete overhaul of the budgeting process each year.

- This method is particularly suitable for organizations with relatively stable operations and minimal year-to-year changes, as it builds on established budgetary foundations, making it easier to track and manage finances.

Incremental Budgeting Explained

Incremental budgeting involves setting the budget for the next year based on the previous year’s budget, with adjustments made to accommodate expected changes. The budget is incrementally adjusted from the prior budget to reflect various factors.

Several key factors should be taken into consideration when making adjustments to the previous year’s budget. These factors include:

- Inflation: Adjustments for inflation should be considered to account for changes in the costs of goods and services.

- Changes in Revenue: Budgeting should be adjusted to reflect changes in revenue projections, which may be influenced by shifts in sales, pricing, or other relevant factors.

- Cost Changes: The costs of goods and services, which may be influenced by market conditions, supplier prices, or other variables, should be considered.

- Staffing Levels: Changes in the number of staff members, which may be driven by variations in workload, organizational goals, or other factors, should be considered.

- Organizational Goals: Adjustments may also be made to align the budget with changes in organizational goals or priorities. These changes can be influenced by shifts in the competitive landscape, introducing new products or services, or other relevant factors.

Examples

Let us look at some examples to understand the concept better:

Example #1

Let’s consider an example in the context of small business budgeting. Imagine Sarah runs a small retail store and has been using incremental budgeting for her financial planning. Last year’s budget served as her starting point, and she made phased adjustments based on factors like inflation and expected changes in revenue. This approach provided stability and predictability, making it easier for Sarah to plan for the upcoming year. As a result, she was able to track her performance, set financial goals, and efficiently allocate resources to meet her objectives, ensuring the smooth operation of her store.

Example #2

Suppose Tech Innovations, a tech manufacturing company, uses incremental budgeting for its end-of-year budget process. They begin by comparing their current year’s budget to actual figures identifying variances. They opt for incremental budgeting, adjusting last year’s numbers to align with expected changes. Cautiously, they forecast next year’s revenue and expenses, considering inflation and leaving room for savings.

Their budget isn’t just numbers; it’s a strategic plan with short-term benchmarks. Tech Innovations creates multiple scenarios, from worst-case to best-case, and aligns its budget with its values, including employee engagement and social responsibility. This approach helps them navigate the upcoming year while staying true to their goals and values.

Advantages And Disadvantages

The advantages are the following:

- Stability: It offers a level of stability by using the previous year’s budget as a starting point. This stability aids in long-term planning and decision-making.

- Accountability: Organizations can hold individual departments or managers accountable for their spending because the budget is based on the previous year’s spending. Any changes in spending point to specific areas, facilitating responsibility tracking.

- Historical Data: Relying on historical data for budgeting allows organizations to make informed decisions based on past performance and trends.

The disadvantages are the following:

- Lack of Flexibility: Incremental budgeting may not account for new projects or initiatives that require funding, potentially stifling innovation and hindering the pursuit of new opportunities.

- Budgetary Slack: There’s a risk of budgetary slack, where departments or managers intentionally overestimate their expenses to secure sufficient funding. This can lead to resource wastage and inefficiencies.

- Resistance to Change: This budgeting technique can foster resistance to change, as departments or programs may be reluctant to deviate from their previous year’s budget. This resistance can limit innovation, hinder growth, and impede organizational improvement.

Incremental Budgeting vs Zero-Based Budgeting

The differences are as follows:

- Approach: Incremental budgeting starts with the assumption that the previous year’s budget is a suitable starting point and makes adjustments incrementally. In contrast, zero-based budgeting requires a thorough review of each budget item, regardless of its inclusion in the previous year’s budget.

- Resource Intensity: Incremental budgeting is typically quicker and requires fewer resources than zero-based budgeting, necessitating a comprehensive review of every budget item.

- Scope: Incremental budgeting tends to be more limited in scope, primarily focusing on incremental changes to the budget from year to year. Conversely, zero-based budgeting offers a more comprehensive analysis of each budget item, assessing its alignment with the organization’s goals and objectives.

Frequently Asked Questions (FAQs)

1. Why do we need incremental budgeting?

Incremental budgeting provides a stable framework for organizations to plan and make decisions, building upon the previous year’s budget. It simplifies budgeting processes, ensures accountability, and utilizes historical data for informed decision-making. It is particularly useful when an organization’s operations are relatively stable and major changes from year to year are minimal.

2. What are the features of incremental budgeting?

Incremental budgeting features incremental adjustments to the previous year’s budget, assuming it as a baseline. It’s a conservative approach, quick to implement, and less resource-intensive than other budgeting methods. It holds departments accountable for their spending, relying on historical data to guide budget decisions.

3. What are the risks of incremental budgeting?

The risks of incremental budgeting include potential inflexibility, as it may not adequately accommodate new projects or initiatives. There’s a risk of budgetary slack, where departments overestimate expenses to secure funding, leading to inefficiencies. Incremental budgeting can also foster resistance to change, hindering innovation and organizational growth.

Recommended Articles

This article has been a guide to what is Incremental Budgeting. Here we explain its examples, advantages, disadvantages, and comparison with zero-based budgeting. You may also find some useful articles here –