Part of our Budgeting and Planning guide

What Is Participative Budgeting?

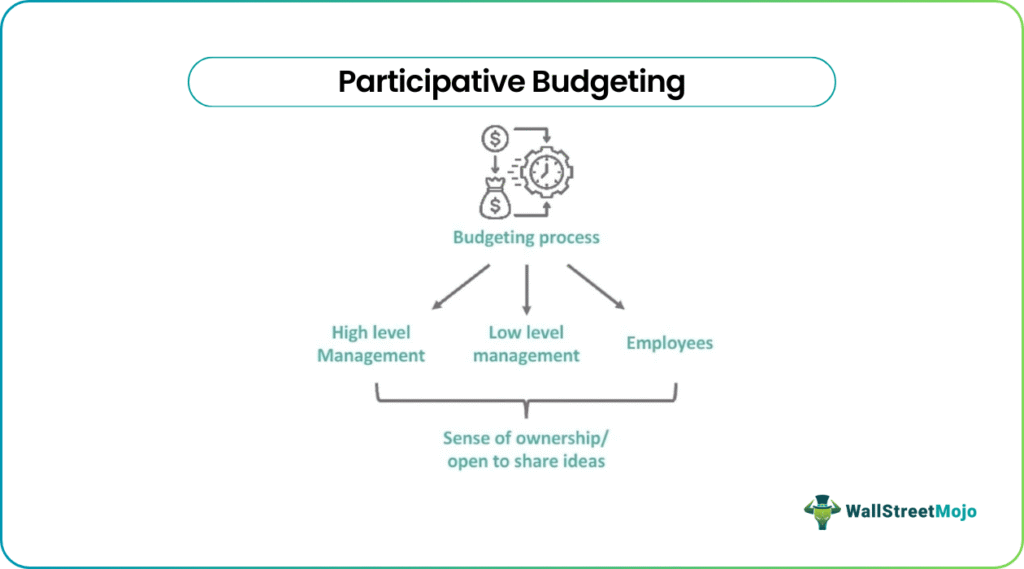

Participative budgeting is the kind of budgeting process that involves the lower level management in decision-making and budget preparation, along with taking all the responsibilities for the project undertaken so that the employees can also be associated with the budgeting process.

As a result, they can get a sense of ownership and a better stake in the firm to openly share their ideas and participation in budget creation. Participative budgeting is a new-age budgeting technique. It allows participation so that whosoever has a stake in the Company can get involved and brainstorm their ideas so that the budget is more realistic and achievable in real life.

Participative Budgeting Explained

Participative budgeting is that method of budgeting wherein the top-level management shares the responsibility of the budget creation with the bottom level management because lower-level managers are more capable of giving the real picture at the field level like availability of resources, the time needed to prepare the budget, hindrances related to different aspects, etc. than the top-level managers.

Here in the participative budgeting process both the parties are affected by which one is preparing the budget and who will imply the budget. It involves the participation of all the employees so that a fair and reality-driven budget can be accomplished.

Participative budgeting works well when there is a perfect synergy between higher and lower-level management. It is needless to say that top-level managers are very less known about the departmental costs and expenses of the Organization. On the other hand, the lower-level managers are well aware of their respective departments’ costs and deemed expenses. Therefore, delegating duties should be realistic to achieve a perfect budget preparation, which can be effective for the future course of action.

The managers should share the facts, whomever is best concerned for the department, and it would be useful if the Organization adopted the system for the checks and balances method. This system allows the filtration of data at every level. Whenever any statement of expenses/cost is shared by the lower-level management and will be passed in a hierarchy, the data should be checked by the concerned departments and further passed on. In this way, all the irrelevant costs can be avoided. The two favorite ways to adopt Participative Budgeting are Pure Participative Budgeting and Top-Down cum Participative Budgeting.

Examples

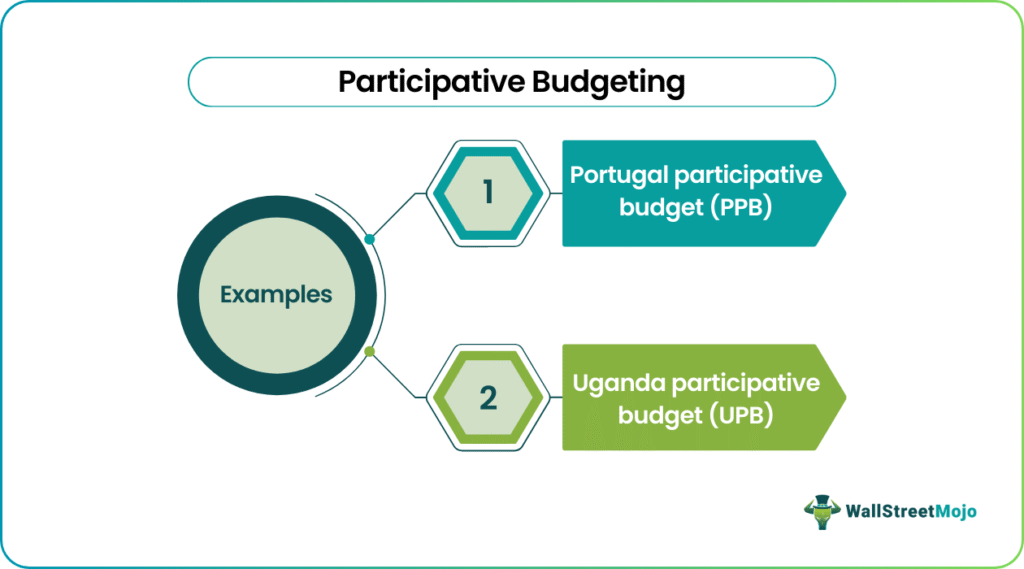

Let us understand the concept of participative budgeting process with the help of some suitable examples.

Example #1

Here, we learn about the Portugal Participative Budget (PPB). This kind of budgeting allows the country’s residents to make investment decisions and choose the project in which they want to invest their money. Initially, the policymakers did not allow the people to interfere in the decision-making process. Still, the public gathering and unity of people made the participation open to the market, and people started taking open voting schemes, which made PPB successful in the country.

Example #2

There is also Uganda Participative Budget (UPB), where the budgeting invites budget suggestions from all the stakeholders and looks upon the various priority sectors of the country. Therefore, the budget preparation system is transparent as everyone is taken along to draft the final blueprint, and UPB has been praised globally for its budgeting technique.

Why Is Participative Budgeting An Effective Management Tool?

This is an effective management tool in a company because of the following reasons.

- The top-level management gets to know the problems/issues faced by the lower/middle-level management.

- The transparency in the firm increases as the higher authorities show interest in the lower management. In return, their faith in the firm gets restored, lower/middle-level management gets motivated, and organizational goals can be achieved easily.

Advantages

This process of budgeting also has its own advantages and disadvantages. Let us study the advantages first, as given below.

- Participative budgeting allows the useful exchange of information from lower-level management to top-level management. There can be an easy flow of information and timely reports presented by the concerned department.

- As the concerned department delivers the information, there is very little chance of over/under budget preparation as the correct data have been shared.

- The subordinate level is also involved in the decision-making process, and everyone gets an open forum to give their input for the betterment of the budget. This leads to boosting the morale of the employees and, in return, achieving Organizational goals.

- The confidence in both superior and lower level management gets reinstated because both the parties have revalidated their work and shown interest in them.

- Through this participation, the efficient allocation of resources can be done; there would be minimum wastage and a correct, realistic budget.

Disadvantages

The disadvantage so the process are elaborated below.

- A negative remark about this budgeting would be that it is time-consuming because every management level is involved in this. Hence, the time is taken to deliver the cost statement, and the expense chart can hinder the budget in a short period.

- Moreover, due to involvement of a larger group off people, there is a possibility of delay in decision making, due to varied opinions and ideas from different groups.

- More information and agreement of all parties are really important in the process, which may not always help. There is a possibility of the process getting diverted from the actual objective.

- There is also a possibility of conflict and mismanagement leading to higher cost, lack of decision making and commitment towards a common objective.

- There is also the risk of information misuse and manipulation. Managers or employees may have some of their own personal interest in the budget of the company and they may be more eager to get it approved earlier.

- If a business is used to budgeting in the traditional manner, there may be opposition or resistance if the business suddenly wants to adopt the new participative system, creating tension and friction in the workplace.

- In case of sudden crisis and any unforeseen contingencies of the business, this method of budgeting may not be suitable because it is time consuming and and costly. Sudden crisis requires immediate action and implementation through cost control.

Participative Budgeting Vs Traditional Budgeting

Both the above are two different approaches for preparing budget in an entity. The entity can adopt any of the two approach depending on the type or business of the company, the objecting of the budget and resources available. But it is necessary to understand the differences between them, as follows:

- Participative budgeting is a very modern approach and is popularly implemented in organizations these days because it is a very collaborative approach.

- On the other hand, Traditional Budgeting is now a backdated system of budgeting, but still, many companies are using it.

- The former makes everyone around responsible and accountable for the work done so that every work can be well delegated. The concerned department can figure out costs. But for the latter there are constraints in the participation, and only the top-level managers make decisions regarding the future costs/expenses and investments without looking into the reality check, which may sometimes lead to a faulty over or under-budget preparation.

- The former makes everyone around responsible and accountable for the work done so that every work can be well delegated. The concerned department can figure out costs. But for the latter, there are constraints in the participation, and only the top-level managers make decisions regarding the future costs/expenses and investments without looking into the reality check, which may sometimes lead to a faulty over or under-budget preparation.

- From the above two points, we can derive that the former is a method of budgeting that gives every participant a sense of belongingness and ownership whereas the later does not allow this. However, since in case of the former, there are many levels participating in the process, there is a huge possibility of more time consumption, which in case of the latter will be faster because of limited involvement of people.

- The former will also require more consensus and information or inputs that also lead to increase the cost. But for the latter, the cost as well as the information and consensus requirement are less.

- In case of the former, a wider range of experience, knowledge and ideas can make the process better and of higher quality, but for the latter, this may not be possible because of limited minds contributing their knowledge and skill.

Thus, from the above points we can conclude that both have their own pros and cons. But it is up to the organization to select the best option so as to achieve the desired results.

Recommended Articles

This has been a guide to what is Participative Budgeting. We explain its advantages, disadvantages, with examples, & differences with traditional budgeting. You can learn more about budgeting from the following articles –