Part of our Business Finance guide

What is the Pecking Order Theory?

Pecking order theory refers to the model that guides a company in determining the means of financing that should be prioritized over the other to ensure company growth without or with least increase in its financial liabilities further. It helps only analyze a decision but not in actually making it.

It is the method that lets managers follow a specified hierarchy while choosing the sources of finance for the company. Here, the first preference is given to internal financing, then external sources, and then finally, equity. Maintaining this hierarchy of sources of financing not only lets companies limit their external financial liabilities but also helps them to have a good market image.

Key Takeaways

- The pecking order theory outlines a hierarchy of financing sources companies typically follow when raising capital.

- This hierarchy prioritizes internal financing first, then external financing if internal sources are insufficient. If external financing is necessary, debt is typically favored over equity.

- The components of the pecking order theory include internal funding, external funding, debt, and equity.

- While the pecking order theory provides a useful framework for choosing financing sources, it does not offer a quantitative metric for determining the optimal financing mix.

Pecking Order Theory Explained

The pecking order theory of capital structure states that companies must take into consideration the most available resources to finance their needs in the first place. According to this theory, the first source of financing should be the funds that are internally available. Normally, these are the retained earnings, which are left with the companies and carried forward to the next fiscal year, after all their liabilities for the current year are taken care of.

This theory suggests that only when the companies are unable to raise enough funds through internal financing, they should consider the next option, ie., debt financing, and if they still require funds, the third option should be equity financing. In short, using equity as a source of finance must be the last resort for firms.

The theory, believed to be introduced by Donaldson in 1961, was made popular by Stewart Myers and Nicolas Majluf in 1984. It runs on an assumption that managers know more than investors and hence they deliver information about the prospects of the company from their point of view.

The pecking order theory suggests managers use internal funding to meet the financial requirements of the company. This is because, as put forth by Meyers, if the companies approach the investors for financing, they might develop a misconception of the companies approaching them for sharing losses.

This, in turn, is likely to create a bad impression about the entity among investors. Thus, the companies must try their best to handle the losses or immediate requirements of the firm themselves using available resources before reaching out to outside sources.

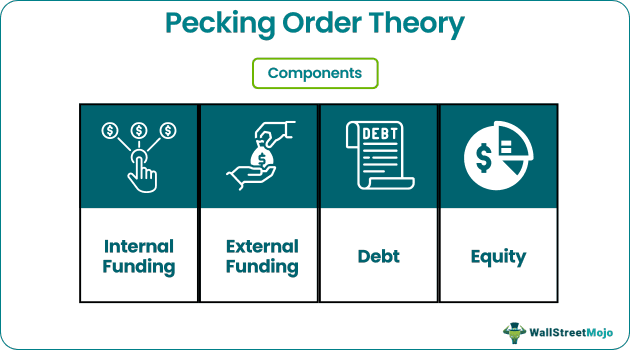

Components

Pecking order theory in finance segments the methods of raising funds for a project or a company into internal and external funding.

#1 – Internal Funding

Internal funding/ financing comes from retained earnings a company has. Why do the CFOs prefer internal funding? Because it is easier to raise funding, the initial funding setup costs are almost zero – because no bankers are involved. Even though internal financing is pretty easy and simple, there are reasons why it might not be preferred. One is that the risk transfer of losses still stays with the company.

If the company is taking up a risky project with low-risk preferences, then internal financing is not the optimum way to finance the project. The second reason is taxation. By taking debt, the company can reduce their taxes based on their interest on the debt. Internal Financing has more stringent regulations on how the funds can be invested without tax. Above all, to finance the project budget internally, the company must have enough funds, limiting the other ways that capital can be utilized.

#2 – External Funding

External financing can be of two types. By taking the requisite budget as a loan or selling a part of the company’s share as equity. There is an entire discussion on choosing an optimum capital structure that can help the company minimize the cost of capital and maximize the risk transfer. However, that discussion is out of scope for this article, which will be discussed separately in another article. Now, let us dwell on details about each type of funding.

#3 – Debt

As the name says, debt funding is where the company raises the required amount through a loan – either by selling bonds if the company wants to raise loans in a tradeable market or by pledging assets if the company wants to raise loans through the banking system. Each of these ways has its own merits and demerits on how to raise a loan. Raising through markets will give the company to choose their interest rates and price their bonds accordingly.

The company will also have the flexibility to buy back the bonds if it wants to or create a bond structure that supports its operational structure. However, bonds are not ideal if the company wants to ensure the funding. Many things could go against the company while raising money from bonds. However, even though it is a bit expensive and the company has to pledge assets, raising money through bank loans guarantees that the money will be raised.

#4 – Equity

No chief of a company would want to sell a part of their company unless deemed necessary. However, there are cases where the only way to raise money is by selling the company. Be it a failure of the company to raise money through debt, or be it the inability of a company to maintain enough portfolio to raise money through bank loans, the company can always sell a part of itself to raise money.

One great advantage of equity financing is that it is not risky. It is completely dependent on the buyer to own a share of the company, and the risk transfer is a hundred percent in this case. The company has no obligation to pay the shareholder anything.

POT says that the order in which the company tries to raise funding is:

Internal Financing -> Debt -> Equity.

The basic nature of POT arises around the information asymmetry – where one party, the company, holds better information than the other (in case of external financing). External financing is generally more expensive than internal financing to compensate for the information asymmetry and risk transfer. In general, equity holders, who hold the highest risk, demand more returns than debt holders, though the company has no obligation to hold those returns.

Examples

Let us consider the following examples, which define pecking order theory and its application, in detail for a better understanding:

Example 1 – Concept-based

Consider the following situation. A company has to raise 100 million USD to expand their product to different countries. In addition, the following is the financial structure of the company.

- The company has net earnings, cash, and other equity of 210 million USD on their balance sheets

- The bank agreed to lend the company money at a rate of 8.5% because of the company’s debt rating.

- The company can raise equity, but at a discount of 7.5%, i.e., if the company issues further rounds of funding, the company’s share price would fall by 7.5%, which is the rate at which the company can raise the funding.

If the company has to raise funds for the project, it can combine the above methods. The pecking order theory says that the cost of funding will be in ascending order in the above case. Let us calculate it for ourselves and try to verify the same.

- Case 1: If the company uses its cash and other equivalents to fund the project, the cost of financing would be 100 million USD. There will not be any additional costs, except for the opportunity cost of money. Valuing opportunity cost is a different subject in its entirety.

- Case 2: If the company uses debt to raise its funds, it will return its profit by 8.5 million dollars – which will be paid as interest. However, the company will have tax benefits in using debt financing. The interest will be tax-deductible so that the effective interest rate will be less than the actual interest paid. Therefore, the total one-year cost would be less than 108.5 million USD, but greater than 100 million USD.

- Case 3: If the company raises funds through equity, it will cost the company 108.12 million USD (100 million divided by 92.5% – 7.5% discount on raising additional equity)

Now, depending on the risk preference of the company, the CFO can decide how to raise the capital accordingly.

Example 2 – #2. Real-Life Scenario (Uber)

To see if, and how, the Pecking Order Theory holds in real life, let us consider a couple of companies and how they raised financing. Since these are real companies, the order in which they raised the funding will have a lot of other variables that take a role in decision-making. For example, when the theory was developed, the concept of venture capital was at a very nascent stage. It isn’t easy to see where venture capital holds in the pecking order theory. It is a sort of private equity and has similarities to internal financing as nothing is pledged. It also has characteristics towards equity – since the venture capitalists expect more than the general equity – because they hold the risk.

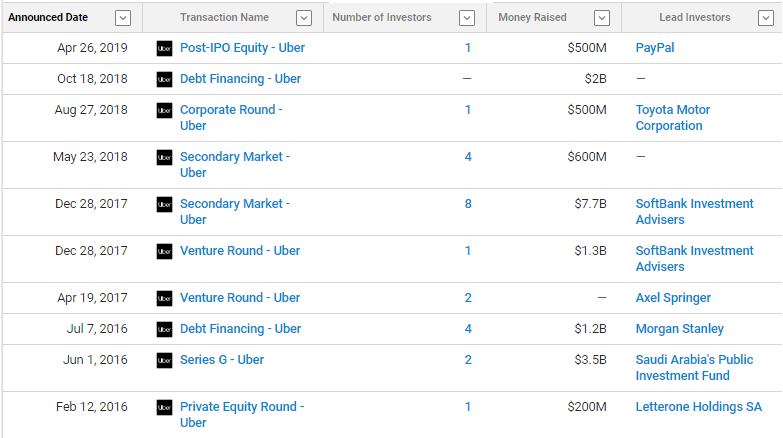

The following image shows how Uber’s funding rounds have gone through. Let us only use a couple of examples to prove POT and a couple to disprove POT.

Where POT holds: The first round of funding, as expected, is raised by the founders of Uber – Letter one Holdings SA. They used 200,000 USD of their own money in 2016, without any obligations. The first debt round for Uber came around in 2016, where it raised 1.2 billion USD, a post that Uber had another debt round where it raised 2 billion USD. Most recently, Uber raised about 500 million USD via an Initial Public Offering. It is a classic scenario where POT holds, and the company follows a specific hierarchy to raise money for expansion.

Where POT fails: However, before the company raised its first debt round in 2016 and after the first internal financing round in 2016, it had over six financing rounds. It raised about 2 billion USD through selling equity – privately. This is a limitation of the pecking order theory. Pecking order theory is based on information asymmetry, and such cases are not covered.

Advantages and Disadvantages

The theory describes what and how financing should be raised without providing a quantitative metric to measure how it has to be done. It is used as a guide in selecting financing rounds, but there are a lot of other metrics. Using this theory in a mixture of other metrics will provide a useful way to finance.

Though the theory is of great use in multiple ways, there are certain limitations as well that restricts the companies in certain situations. Thus, along with the benefits, firms must also know the points where this theory doesn’t work or fails.

Let us have a look at the list of both merits and demerits of the pecking order theory below:

Pros

- POT is valid and useful guidance to verify how information asymmetry affects the cost of financing.

- It provides valuable direction on how to raise funding for a new project.

- It can explain how information can change the cost of financing.

Cons

- The theory is very limited in determining the number of variables that affect the cost of financing.

- It does not provide any quantitative measure of how information flow affects the cost of financing.

- The theory seems to have relevance to the paper, but it might be quite struggling for companies to follow it in all scenarios.

- It cannot make practical applications because of its theoretical nature.

- It limits the types of funding. New types of funding cannot be included in the theory.

- It is a very old theory and has not been updated with newer financial fundraising methods.

- The no-risk vs. reward measure lacks inclusion in the cost of financing.

Frequently Asked Questions (FAQs)

What is modified pecking order theory?

Modified pecking order theory is a financial theory that suggests firms prefer internal financing over external financing but may issue external debt if internal funds are insufficient. It also suggests that firms may issue equity as a last resort to avoid financial distress.

What is the pecking order theory vs. trade-off theory?

Pecking order theory suggests that firms prefer internal financing over external financing. In contrast, trade-off theory suggests that firms weigh the benefits and costs of each financing option to determine the optimal mix of debt and equity. In addition, the pecking order theory implies that firms may only issue debt when insufficient internal funds exist. In contrast, trade-off theory suggests that firms may issue debt to take advantage of tax benefits.

What are the assumptions of the pecking order theory?

The assumptions of pecking order theory include the idea that asymmetric information exists between management and outside investors, external financing is more expensive than internal financing, and firms prioritize financial stability over shareholder wealth maximization. The theory also assumes that firms have limited access to external financing and that the firm’s current financial position influences financing decisions.

Recommended Articles

This has been a guide to what is Pecking Order Theory. Here, we explain the concept along with examples, advantages, disadvantages, and components. You can learn more about financing from the following articles –