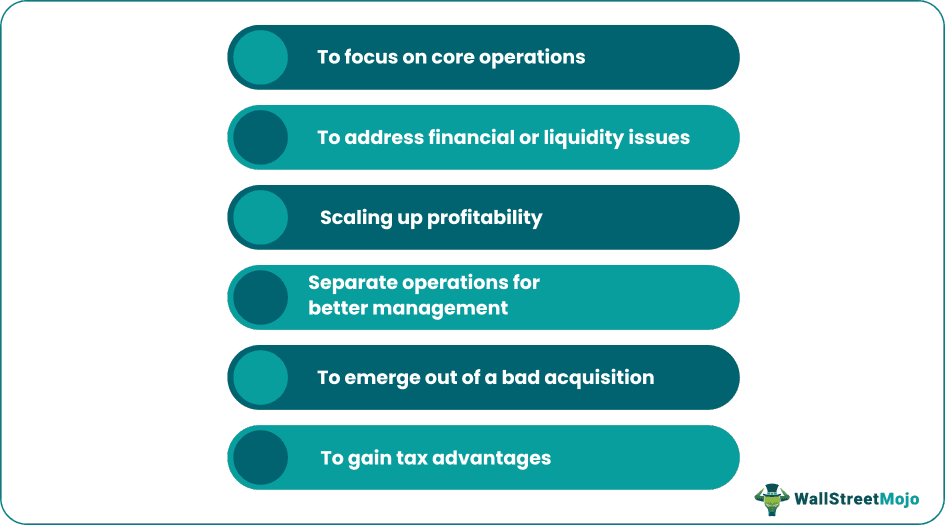

Reasons for Divestiture

Divestment or Divestiture is a phenomenon in the corporate landscape that entails partial or full disposal of the business unit to focus on the more profitable or core models. Managing diverse business lines becomes quite challenging as companies climb up the growth trajectory, so pruning the portfolio becomes an obvious choice. Other reasons that justify divestiture are financial issues or exploiting each entity’s full potential instead of the consolidated entity.

Divestitures can take various forms like a spin-off, split-off, and equity carve-out; however, it all depends on the reason for corporate restructuring. Usually, the divested business lines have the least synergies with the parent company.

What is Spin-Off?

In a spin-off, the shares of the subsidiary company of the spun-off company are distributed as special dividends by the parent company on a pro-rata basis. The parent company usually does not receive any cash consideration for undertaking the spin-off. Existing shareholders enjoy the benefit of holding shares of two companies instead of just one company. The hidden motive is to allow the spin-off to have distinct identities from the parent company’s management. Sometimes the parent company spins off 100% of its shares in the subsidiary. In contrast, at times, it may just spin off 80% to its shareholders and retain a minority interest of the holding. One pre-requisites of a spin-off is that the parent company must renounce control of the subsidiary by distributing a minimum of 80% of its voting shares and non-voting shares.

Salient Features of Spin-off

- A parent company distributes the shares of a subsidiary in the form of a special dividend.

- Stockholders hold shares in both companies.

- Two independent companies come into existence.

- Effective removal of the parent company from the management and decision-making of the subsidiary.

source: Spin-Off Research

Once the subsidiaries are freed from the parent company’s control, one can see fresh streaks of entrepreneurship at play. In addition, the independent new company usually operates with more accountability and responsibility.

Examples of Spin-off:

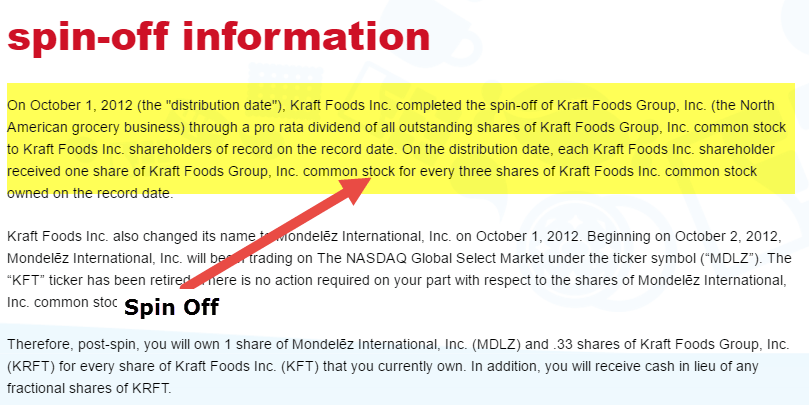

Kraft Foods.: Mondelez Spin-Off

In October 2012, Kraft Foods Inc. spun off its North American grocery business, Kraft Foods Group. A corporate action entailed the distribution of the ratio of 1 share of Kraft Foods Group common stock for every three shares of the parent company’s common stock. Kraft Foods Group then renamed its snacks division Mondelez International, which houses Oreos, Cadbury, Wheat Thins, Ritz, and Trident. Next, the grocery company renamed Kraft Foods Group, focusing on grocery brands like Oscar Meyer, Nabisco, and Planters in North America.

source: mondelezinternational.com

Possible Reasons: The snacks and confectionery business had a wider exposure to high-growth emerging markets, while the grocery business was more North America oriented and stagnating. Therefore, this spin-off undertook to exploit the best of both worlds and manage two different segments in a focused way.

Baxter-Baxalta Spin-Off

In 2014, the leading healthcare company Baxter International, Inc. (BAX) spun off its bio-science arm, Baxalta Incorporated (BXLT). As per the terms of the deal, Baxter distributed 80.5% of the outstanding shares of Baxalta common stock and retained a 19.5% ownership stake in the company. For each share of Baxter common stock held, shareholders received one share of Baxalta common stock.

source: genengnews.com

Possible Reasons: Both businesses operate in distinct markets with different risk profiles. Baxter primarily specialized as a medical supplies company. The combination with bioscience, a completely different portfolio, made operations and valuation difficult. Therefore, the management saw it in the company’s best interest to spin off the non-core arm.

Spin-Off vs. Split-Off Video

Number of Completed Spin-Offs by Year

source: Spin-Off Research

source: Spin-Off Research

Types of Spin-offs

Due to various reasons for restructuring and many reasons behind doing so, spin-offs manifest themselves in multiple forms. Some of the common ones are: –

Pure Play

Pure play is the most original form of a spin-off. It involves shareholders distributing shares of the subsidiary as a special dividend. As a result, both companies have a common shareholder base. This method starkly contrasts with an Initial Public Offering (IPO). The parent company offloads some or all of ownership in a division rather than divesting without any cash consideration. As a result, it has gained momentum post-1990. Moreover, the emerging competitive landscape motivates management to enhance operational efficiency and hone strategic decision-making skills.

Equity Carve-out

Many people confuse carve-out with pure play. However, there are minor differences between the two. In carve-out, the parent company sells an interest of less than 20% in the new subsidiary, the public in a registered Initial Public Offering (IPO) for cash proceeds instead of existing shareholders. It is also known as a partial spin-off. When a corporation needs to raise capital, selling off a portion of a division while holding control proves a win-win situation. There are other motivating factors also behind a carve-out as well. Sometimes a company might feel that a particular division has hidden potential and might perform well once spun off. In addition, a specific stock garners more attention and enables investors to value the business independently.

Tracking Stocks

Unlike a spin-off where a division goes separate from the parent and establishes itself as a financially and managerial independent company, tracking stocks represent shares that are still a part of the parent (i.e., no legal split of the assets or liabilities). The parent and tracking stock have a common management team, and Board of Directors. However, the tracking stocks represent separate financial reporting and analysis from their parent company.

The tracking stocks score some advantages (to the issuer) over spin-offs. First, issuing them is a tax-free procedure, and if one of the two units undergoes a financial loss, the earnings from one will make good the losses of the other for tax purposes. If the parent company enjoys a higher credit rating, the tracking stocks can reap the advantage of lower borrowing costs. The more the synergies between the parent and tracker, the higher the benefits. Finally, issues stocks with the sole purpose of gaining from the high stock prices of the parent.

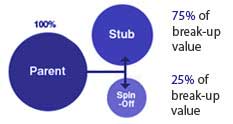

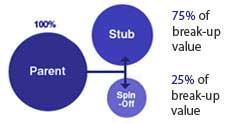

Stubs

When a company distributes shares in a subsidiary to the public while retaining ownership to some extent, it is known as a partial spin-off. Once the spun-off unit or the subsidiary becomes publicly traded, we can determine the market value of the parent company’s investment in the subsidiary.

If we subtract the subsidiary’s intrinsic value from the shares’ inherent value, we can arrive at the value of the core operations of the parent, also known as the stub.

source: Spin-Off Research

Split-offs: A distant cousin of Spin-off

We spoke enough about spin-offs, so now let us shed some light on split-offs, a distant cousin of a spin-off. Conceptually, both are forms of divestiture, but there are differences between the corporate structures that reorganize themselves. Split-off means restructuring an existing corporate system. For example, the stock of a business unit or a subsidiary is transferred to the parent company shareholders instead of stock in the latter. While on the other hand, spin-off stocks in a subsidiary are distributed to all existing shareholders, just like the dividend.

Source: investmentbank.com

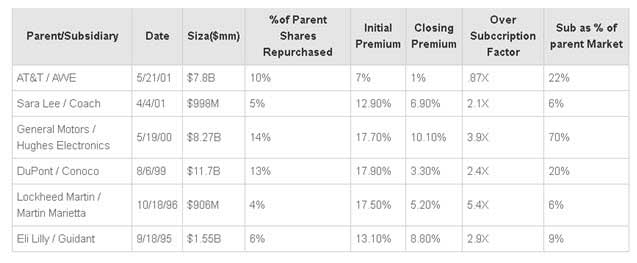

In a split-off, the parent company gives a tender offer to its shareholders to exchange their shares for new shares of a subsidiary. The tender offer usually gives a premium to encourage existing shareholders to go for the offer. This privilege of “premium” tells why split-offs typically end up being oversubscribed.

If the offer is oversubscribed, more parent shares are tendered than the subsidiaries because the exchange happens on a pro-rata basis. On the flip side, if the tender offer is under-subscribed, it means that too few parent company shareholders have accepted it. As a result, the parent company will usually distribute the remaining unsubscribed shares of the subsidiary on pro-rata through a spin-off.

source: Spin-Off Research

Split-off Examples

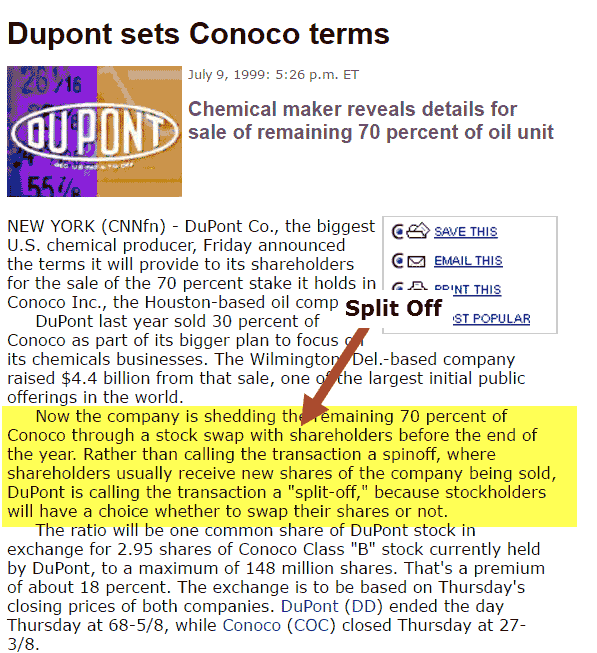

Du Pont-Conoco Split Off

In October 1998, Du Pont generated $4.4 billion from an initial public offering of 30% of the shares of its Conoco unit. DuPont planned to divest itself of its remaining stake of 70% in Conoco Inc. through this proposed stock swap. In 1999, the former then designed plans for a final split from its Conoco Inc. oil unit, offering to swap Conoco’s stock worth $11.65 billion for about 13% of DuPont’s shares outstanding. At that time, this IPO was one of the largest in history.

Source: money.cnn.com

Possible Reasons: Conoco Inc. was a strong and steady contributor to DuPont’s revenue, and cash flow. Still, Dupont felt it was in the companies’ best interests to operate as separate entities and scale new heights. DuPont wanted to concentrate on its materials and life sciences business, while Conoco wished to explore the imminent growth in energy markets.

Lockheed Martin-Martin Marietta Split-Off

Lockheed Martin Corp. announced plans to split off the 81% interest in Martin Marietta Materials Inc., a highway construction material producing company. This split-off aimed to provide Martin Marietta Materials with immense opportunity to pursue its growth strategy and finance the acquisitions. As per the terms of the split-off deal, the latter distributed 4.72 shares of materials common stock for each share of Lockheed Martin common stock.

Possible Reasons: Lockheed was into a substantial debt pile, estimated at around $13 million, and the move would generate enough cash to service the debt. Similarly, Martin Marietta Materials would plan more inorganic growth through acquisitions and mergers.

Tax Treatment for Spin-offs

Spin-offs have earned brownie points for being tax-free options. However, this is not always the case. Whether a split-off will be tax-free or taxable is decided so that the parent company divests the subsidiary or a part of itself. The tax perspective is governed by Internal Revenue Code (IRC) Section 355. While financial viability is the key driving force behind split-offs, it is also imperative that shareholders’ interest is taken care of. Usually, divestiture attracts long-term capital gains, so the split-off has to be designed to be tax-free.

One method ensures that the distribution of shares in the new spin-off to existing shareholders is indirectly proportional to their equity interest in the parent. E.g., If a stockholder has a 3% holding in the parent company, his shareholding in the spin-off company will also be exact 3%.

In the second method, the parent company offers an option to the existing shareholders to exchange their shares in the parent company for an equal proportion of shares in the spin-off company or continue maintaining their holding in the company. Some also exercise the option of holding both stocks. It is something along the lines of a split-off.

Conclusion

A spin-off, split-off, or equity carve-out are three varied methods of divestiture with the same objectives-Enhancing shareholder value, tax benefits, and improved profitability. However, the goal of all these three methods is the same. The selection amongst them is based on the broader corporate strategies of the parent company. As a result, exit strategies pepper with various challenges.

Carving out a company that is different from the company’s core operations requires thorough due diligence. A well-etched strategy analysis can build confidence in the process, get perfectly aligned operations, and drive the entire transaction to realize its highest potential.

Separation complexities are demanding and involve negotiations at each step. A preconceived transition plan which spells out the entire process and the work involved at each stage would go a long way in keeping things streamlined.

Next is focusing on the compliance perspective. The spun-off company should adhere to the prevalent financial reporting norms and comply with internal and external controls and regulations like Sarbanes Oxley, SEC filings, etc.

The company’s understanding of identifying these challenges and underlying risk factors at the right time in the planning phase while considering the key value drivers behind the divestiture will lead to increased value generation from the chosen exit strategy.