What Is Residual Value?

Residual value is the estimated scrap value of an asset at the end of its lease or its economic or useful life. It represents the amount of value that the owner of that particular asset will obtain or expect to get eventually when the asset is dispositioned.

Also known as salvage value, it is calculated for the firms to be aware of the existing value of the asset when it is of no use anymore. This value is inversely proportional to the length of the useful life of the asset and helps businesses know how much they will receive if they sell the fully used assets.

Residual Value Explained

Residual value, as the name implies, indicates the value of the residue form of an asset, which remains of no use to owners any more. This figure is calculated when businesses are willing to know what their existing assets are worth post their useful life or lease period. If the value obtained is considerable, they have an option to sell it and earn profits in return.

The residual value formula used for the calculation differs from one company to another. However, the companies know the parameters based on which they require assessing the worth of their asset. Let us understand the concept this way – Suppose you lease out a car for the next five years. Then the residual value is the value of the car after five years. It is often fixed by the bank, which issues the lease, and is entirely estimated based on past models and future predictions. Interest rates and relevant taxes are crucial factors determining the car’s monthly lease payments.

This concept is used regularly to calculate an asset’s depreciation expense. Since this value is the ending value of an asset, it must be subtracted from the purchase amount to get the total amount, which gives us the depreciation amount. In the straight-line method, this amount is then divided by the asset’s useful life in years to get the annual depreciation expense for each year. This method is also used in valuation processes.

In finance, the salvage value or the scrap value is used to find out the value of cash flows generated by a company after the time frame used for the forecast. If there is a forecast projection for 20 years, assuming that the company will operate for the next twenty years, the cash flows projected for the remaining years must be valued. In this situation, the cash flows will be discounted to obtain their net present value, which is added to the project’s market valuation or the company. Capital budgeting projects give a clear understanding of the amount for which you can sell off the asset after the firm has finished using it or when the asset-generated cash flows cannot be accurately forecasted.

Residual value, salvage value, and scrap value are similar terms used to refer to the expected value of an asset at the end of its useful life, and this amount is often assumed to be zero. It must be kept in mind that the Residual value of an asset should be calculated at the end of every year specifically. If there is a change in this value estimation while checking, these changes should be kept in the record to keep track of changes in residual value in accounting estimates.

Residual Value Explained in Video

How To Calculate?

There are several ways to understand what an owner will get from an asset s of a future date. These ways are as follows:

#1 – No Value

The first and foremost option for the assets with the lower value is to undergo a no residual value calculation. Here an assumption is made that these assets have no value at the end of their use date. Many accountants prefer it as this helps in simplifying the calculation of depreciation. It is a very efficient method for those assets whose amount of any value comes much below the predetermined threshold level. But the final amount of depreciation that comes by following this method is higher than when a residual value is taken into account.

#2 – Comparables

The second approach is comparables. When the residual value is calculated, it is compared to the value of comparable assets, which are traded in a well-organized market. It is the most defensible approach which is used. For example, if there is a considerably big market in used cars, this can be used to calculate the residual value for a similar type of car.

#3 – Policy

The third one is Policy. There can be a company policy that the residual value of all assets under a particular class is always taken to be the same. This approach cannot be termed defensible since the policy-derived value can be higher than the market value. Using this method will reduce the depreciation expense for a business. So this approach is not followed until and unless the policy based values are kept at a very conservative.

Examples

Let us consider the following instances to understand the residual value meaning and also see how it is calculated:

Example 1

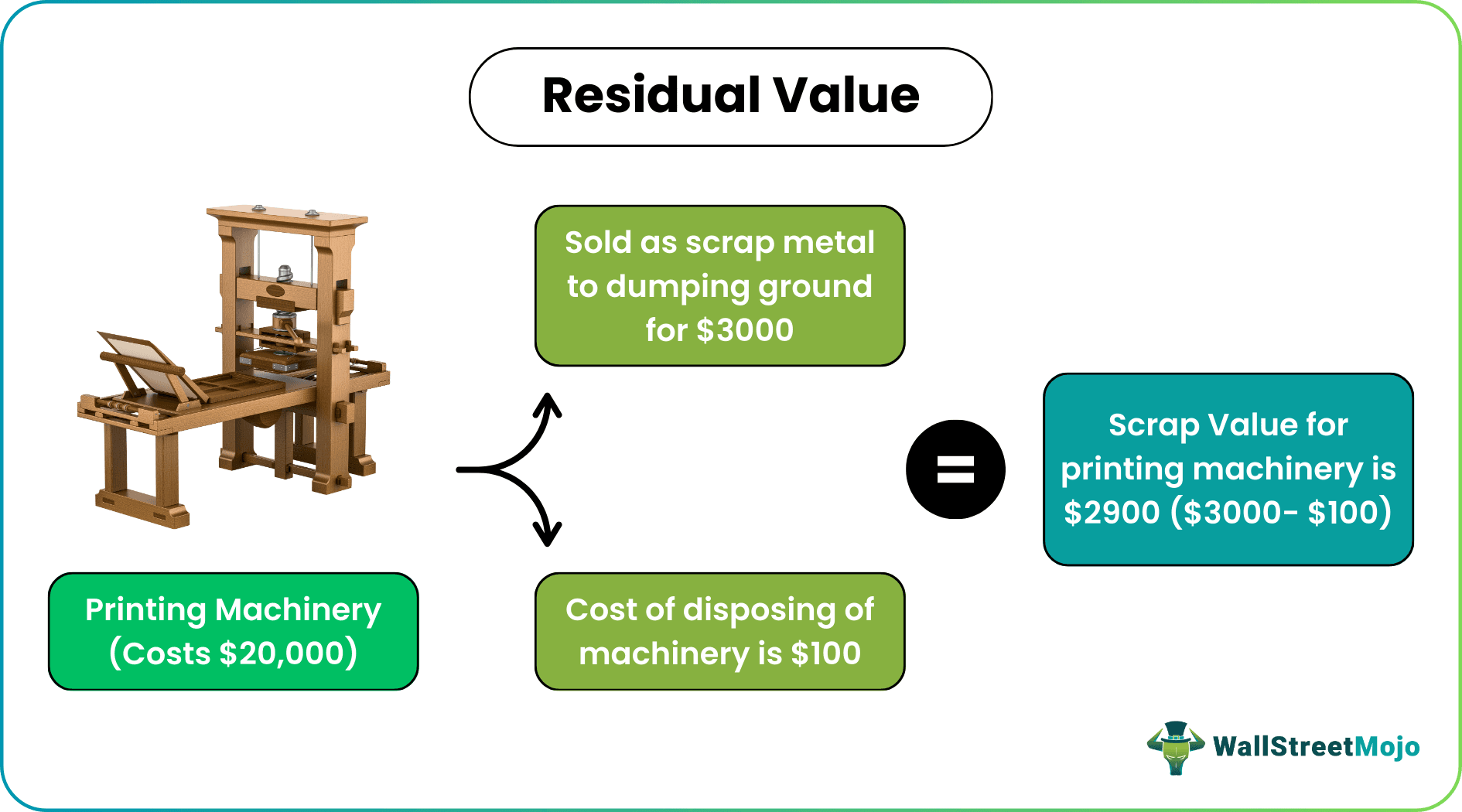

Let us consider a Residual value example of printing machinery. The printing machinery costs $20,000, and we can safely assume that the estimated service life of the machinery is ten years. It can be estimated that at the end of its service life, it can be sold as scrap metal to the dumping ground for $3000. And the cost of disposing of the machinery is $100, which the owner requires to pay for transporting the machine to the dump. Then the calculation of scrap value for the printing machinery is $2,900 ($3000-$100).

Example 2

In October 2023, Toyota revealed how the residual value of the battery electric vehicle (BEV) is poorer than the advanced combustion engine vehicles. The automobile ace, adding to this, said that it would be trying to produce better batteries as the longer batteries will mean better useful life, leading to improved residual values in the future. According to this report, the fleet organizations seem unwilling to buy the BEVs as they think it won’t be worthy investing in it.

Residual Value vs Book Value

Both these terms play an important role in assessing the value of an asset in question. However, they are calculated for two different purposes and in different ways. Let us have a look at the differences between the two below:

- Book value refers to the value of the asset as reflected in the financial statements. On the other hand, residual figures as obtained show the value of the asset that remains after it has been completely used and its useful life or lease period gets over.

- To calculate book value, accumulated depreciation is subtracted from the original cost of the asset. On the contrary, residual value does not have any specific formula. It is rather calculated based on the age of the asset, market trends, its condition, etc.

- The former is used to determine the value of the asset to be recorded in the financial statements or balance sheet, while the residual figure is calculated to help owners know the worth of the asset after its useful life is over. The latter when calculated lets owners know how much they would receive in case they sell the asset to buyers.

- The book value of the asset keeps changing with time as it undergoes depreciation, while the residual value of the asset remains the same throughout its useful life.

Recommended Articles

This article has been a guide to what is Residual Value. Here, we explain the concept along with how to calculate it, its examples and comparison with book value. You may learn more about accounting from the following articles –