Part of our Fixed Assets and Depreciation guide

Economic Life Meaning

The economic life of an asset refers to the length of time during which it is expected to remain useful and generate economic benefits for its owner. It is determined by factors such as wear and tear, technological obsolescence, and changes in market demand. The aim of analyzing economic life is to understand and measure the financial performance and health of a business or economy.

Several methods are used to calculate it in accounts and finance, including the straight-line depreciation method, double declining method, and unit of production method. The choice of method will depend on the specific circumstances and characteristics of the asset being analyzed. It is important to choose an appropriate method and use accurate assumptions and data when estimating it to ensure that the resulting estimates are reliable and useful in decision-making.

- Economic life refers to the period over which an asset is expected to generate economic benefits for its owner and is an important consideration in accounting, finance, and capital investments.

- Its calculation depends on various factors, including technological advancements, market demand, wear and tear, and the asset’s initial cost and estimated useful life.

- Different methods, such as straight-line depreciation and discounted cash flow analysis, can be used to estimate it. However, appropriate assumptions and data must be used to ensure the resulting estimates are accurate and reliable.

Economic Life Explained

Economic life is a concept used to determine the period over which a tangible or intangible asset is expected to generate economic benefits. It is a crucial factor in calculating depreciation or amortization expense that needs to be recorded in financial statements and influences the timing of asset replacement or upgrades. Its estimates are based on various factors, including the asset’s expected useful life, expected residual value, technological advances, market demand, and other relevant economic factors.

Proper assessment of an asset’s economic life is critical for accurate financial reporting and effective decision-making related to capital investments. For example, a longer-than-appropriate commercially useful life estimate for an asset can lead to overstated profits and book values. In contrast, a shorter-than-appropriate economic life estimate can lead to understated profits and book values, resulting in negative consequences for the company. Therefore, companies must carefully assess an asset’s economic life and revise it periodically to reflect any significant changes in the factors determining its useful life.

Example

One example from accounts and finance is estimating the economic life of a machine used in a manufacturing plant.

Let’s say a company has a machine expected to last for 15 years based on its physical life. However, the machine may become obsolete after ten years due to rapid technological advancements, making its economic life only ten years. In this case, the company would need to estimate the depreciation expense over ten years instead of fifteen years to accurately reflect the machine’s actual economic value in its financial statements.

Another example in accounts and finance is the estimation of the economic life of a patent. A patent is a legal monopoly granted to an inventor to prevent others from producing, selling, or using an invention without the inventor’s permission. A patent’s commercial viability is when the patent owner can generate economic benefits from the invention. The commercial viability of a patent is typically shorter than its legal life, usually 20 years. It is because a patent may become obsolete or less valuable due to technological advancements, changes in market demand, or the expiration of its legal life. Thus, the company that owns the patent must carefully assess its commercial viability to determine the appropriate amount of amortization expense to be recorded in its financial statements.

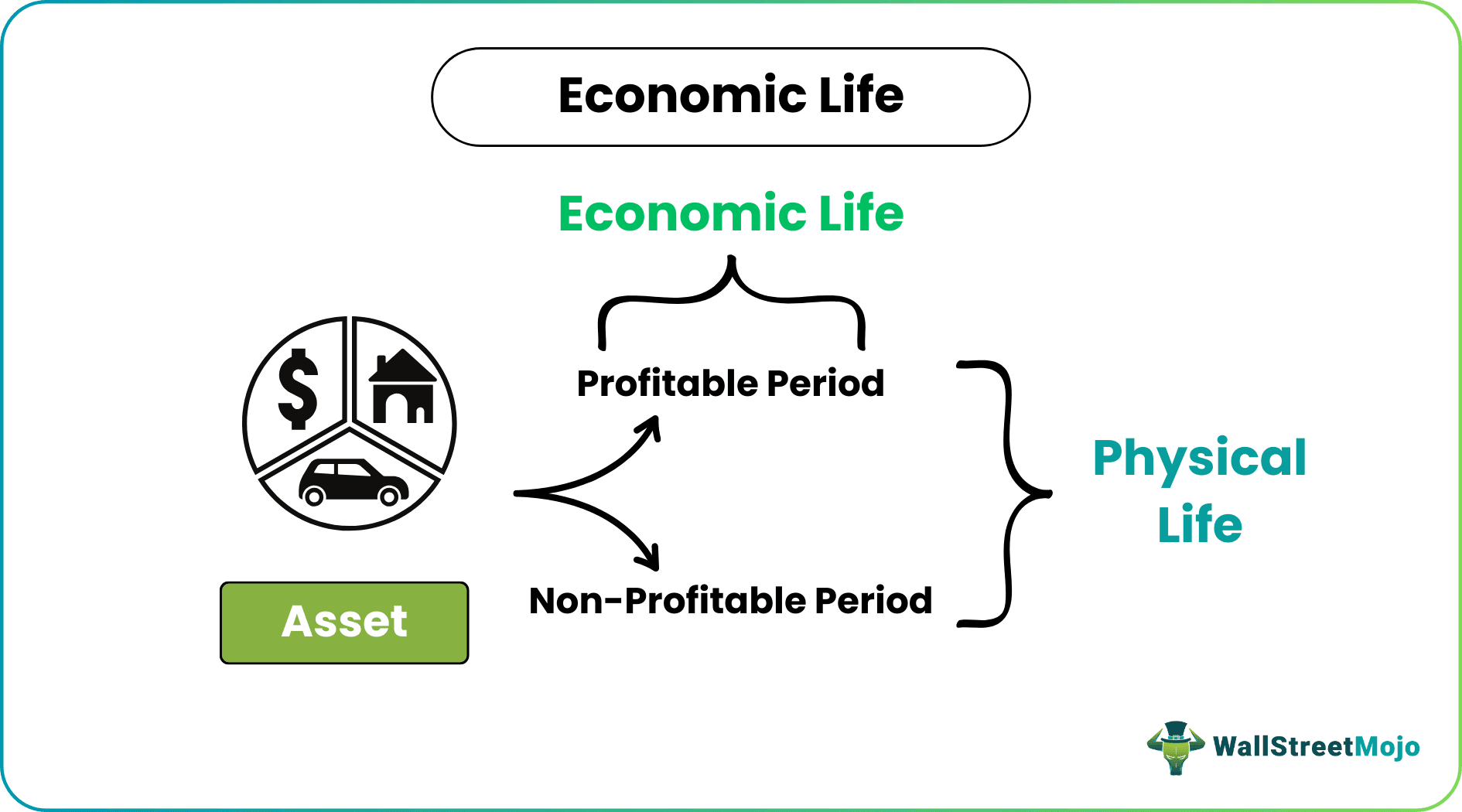

Economic Life vs Physical Life

The economic life of an asset is typically shorter than its physical life because it may become obsolete or less valuable due to technological advancements or changes in market demand. For instance, a computer may have a physical life of 10 years, but its economic life may be significantly shorter due to rapid technological advancements. Thus, it is important to distinguish between an asset’s physical and economic life when making financial decisions related to capital investments.

| Economic Life | Physical Life |

|---|---|

| The period over which an asset generates economic benefits. | The length of time an asset remains in usable condition. |

| Factors such as technological advancements, changes in market demand, and wear and tear are considered. | Only physical wear and tear is considered. |

| Used to calculate depreciation or amortization expense and determine optimal timing for asset replacement or upgrades. | Used to determine maintenance and repair schedules or warranty periods. |

| Typically shorter than physical life. | Generally longer than the economic life. |

| An important consideration in financial reporting and decision-making related to capital investments. | Important for asset management and planning of maintenance and repair. |

Frequently Asked Questions (FAQs)

How to calculate economic life?

The calculation estimates the period an asset is expected to generate economic benefits based on technological advancements, market demand, and wear and tear. Two common methods for estimating are the straight-line depreciation method and the discounted cash flow analysis, which require assumptions about factors such as the asset’s condition, maintenance history, and future cash flows.

What is the difference between economic life and useful life?

The terms “economic life” and “useful life” are often used interchangeably about the expected lifespan of an asset and the length of time over which it is expected to remain useful and generate economic benefits. However, slight differences may exist in how these terms are used depending on the context or industry. For example, “Economic life” may emphasize the asset’s value to the owner. “Useful life,” on the other hand, may focus more on the asset’s functional life and ability to serve its intended purpose, such as through maintenance and repair schedules.

What is meant by the economic life of a building?

It refers to the period during which the building is expected to generate economic benefits for its owner, such as rental income or operational cost savings, and is considered economically viable. Therefore, its estimation is crucial in real estate and finance for determining asset value, financing terms, and return on investment.

Recommended Articles

This article has been a guide to Economic Life and its meaning. We compare the topic with physical life and explain the concept in detail using an example. You may also find some useful articles here: