Part of our Solvency Ratios guide

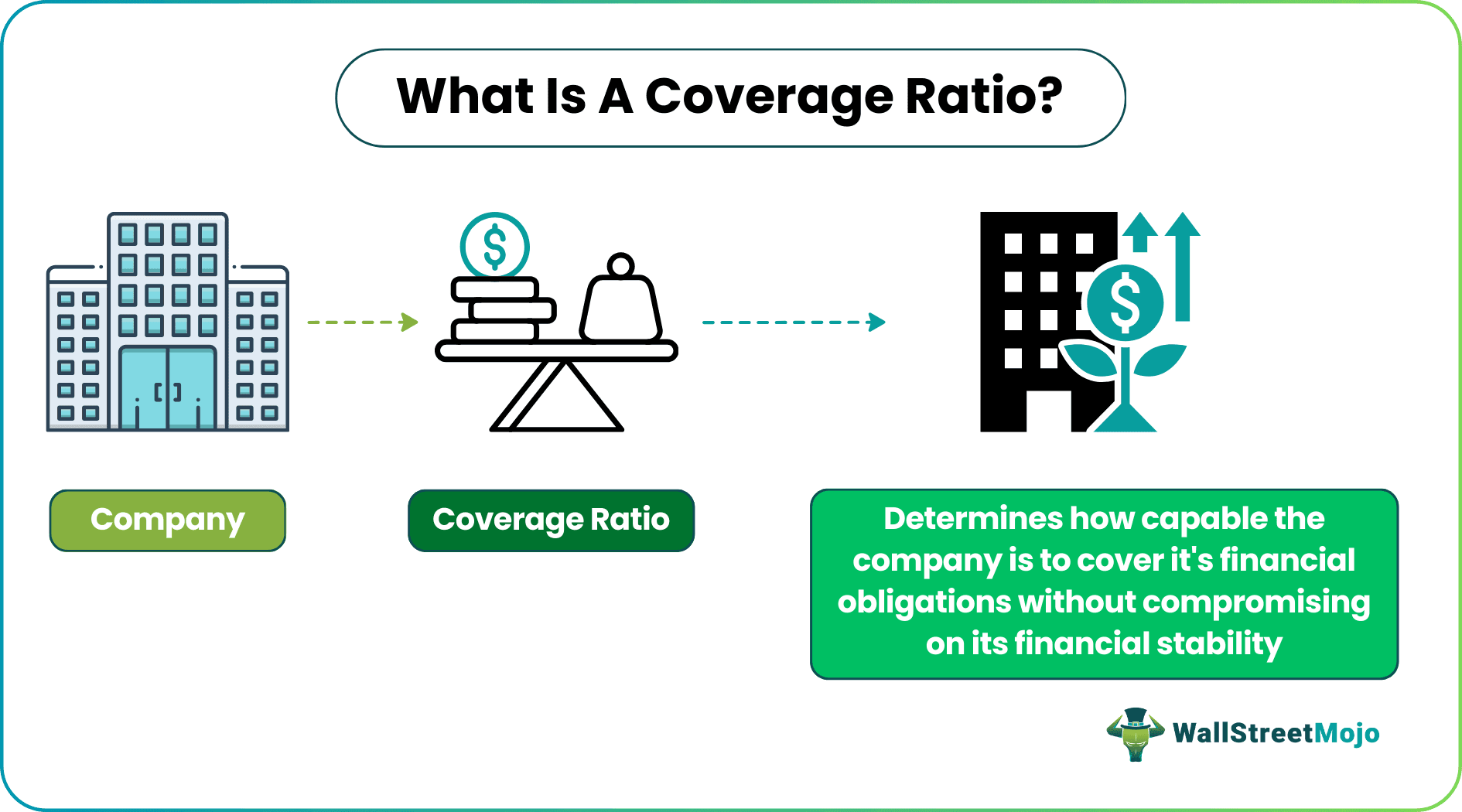

What is Coverage Ratio?

A coverage ratio indicates the company’s ability to meet all of its obligations, including debt, leasing payments, and dividends, over any specified time period. A higher ratio indicates that the business is in a stronger position to repay its debt. Some of the popular ratios include debt coverage, interest coverage, asset coverage and cash coverage.

The coverage ratio helps in tracking the debt situations of a company to help investors make wise investment decisions. If the same has been declining over the years, the investors know of the deteriorating financial state of the company.

- The coverage ratio is a company’s capacity to pay off and cover its liabilities, obligations, debt, leasing payments, and dividends in a stipulated time.

- It implies how well a company’s earnings are sufficient to cover the liabilities and obligations. The higher the ratio, the higher earnings are available with the company to cover the liabilities and obligations.

- These are of various types, such as interest coverage, debt service coverage, asset coverage, and cash coverage.

- It can create a sense of financial responsiveness in the company and create frontiers for the business.

Coverage Ratio Explained

A coverage ratio depicts how capable a firm is of covering all its financial obligations without hampering the flow of the business. The stakeholders, external and internal, use these ratios to understand how strong a firm is financially and whether they can trust it with investments.

It can be used to conduct trend analysis for a company over a period. This calculation shows how its debt-repaying ability is moving over the periods. If it is going down, the firm can have a look at the issue and it can try to rectify that.

These ratios can be used by lenders/creditors before giving a loan. Whether the firm is worthy of loans and at what interest rate loan should be provided. Analysts use these ratios to determine the credit rating of the firm. If the ratings are good, then firms get a loan at lower interest rates.

Types

These ratios can further be derived in multiple terms, which categorize them into different types. Some of the types of coverage ratios are:

#1 – Interest Coverage Ratio

It determines how well a company can pay off its interest in debt using its earnings. It is also known as times interest earned ratio.

#2 – Debt Service Coverage Ratio

This ratio determines the company’s position to pay off its entire debt from its earnings. This ratio measures the company’s ability to repay the entire principal plus interest obligation of debt in the near term. If this ratio is more than 1, the company is in a comfortable position to repay the loan.

#3 – Asset Coverage Ratio

This ratio is similar to the Debt Service ratio, but instead of Operating Income, it will see whether debt can be paid off from its assets. If the firm is not able to generate enough income to repay debt, then the assets of the company such as land, machinery, inventory, etc. can be sold off to give back the loan amount. Usually, this ratio should be more than 2.

#4 – Cash Coverage Ratio

Cash Coverage determines whether a firm can pay off its interest expense from available cash. It is similar to Interest Coverage, but instead of Income, this ratio will analyze how much cash is available to the firm. Ideally, this ratio should be greater than 1.

Formula

Based on the types of these ratios, the formula differs. In fact, analysts use the below-mentioned ratios to determine the firm’s position for its debt obligations in different ways:

Interest Coverage

Interest Coverage = EBIT / Internet Expense

Here, EBIT is the earnings before interest and tax.

Debt Service Coverage

Debt Service Coverage= Operating Income / Total Debt

Asset Coverage

Asset Coverage = (Tangible Asset – Short Term Liabilities)/Total Debt

Cash Coverage

Cash Coverage = (EBIT + Non Cash Expense)/Interest Expense

Calculation Examples

Example #1

Let’s say a firm’s total Operating Income (EBIT) for the given period is $1,000,000, and its total outstanding principal debt is $700,000. The firm is paying 6% interest on the debt.

So, its total interest expense for the given period =debt * interest rate

=700,000*6% = $42,000

- Interest Coverage

- Debt Service Coverage

total debt payable (Principal plus interest)

- Asset Coverage

Let’s say the firm is having $900,000 of tangible assets and its short-term liabilities are $100,000

- Cash Coverage

And non-cash expenses are $100,000

In this case, the ratio analysis depicts that the firm is in a comfortable position at the moment to pay off its debt using its earnings or asset.

Example #2

Let’s take a practical example of an Indian company which is having quite a high amount of debt on its balance sheet. Bharti Airtel is a highly debt-ridden Indian telecom company because of the high CapEx requirements in this industry.

Below are some of the basic data for Bharti Airtel:

Source: Annual Reports and www.moneycontrol.com

The graph below clearly represents the trend of coverage ratios for Bharti Airtel:

As observed, these ratios are going down. It is because its debt has increased over the years, and EBIT has gone down. It happened because of the margin pressure and the entry of Reliance Jio into the market. If this continues in the future, Bharti Airtel could be in a bad position. As a result of this, it has to sell off its assets to repay the loan.

Limitations

- At times, a firm takes more debt, but its effect comes to notice only over the next periods. Also, seasonality can be a factor that hides or distort these ratios.

- Some companies have higher CapEx requirements, so their debt size is more than other companies. This is the case when companies change their accounting policies, and because of that, these ratios can be affected.

- Users should not use these ratios as stand-alone. While checking firm health, other ratios, such as liquidity or profitability ratios, also need to be analyzed alongside to make the decision.

Frequently Asked Questions (FAQs)

What are the various coverage ratios?

There are various coverage ratios. Firstly, the interest ratio is calculated by dividing EBIT by interest payment. Secondly, the debt service ratio is calculated by dividing operating income by total debt. Thirdly, the asset ratio is calculated by (tangible asset – short-term liabilities)/total debt, and cash coverage is calculated by (EBIT + noncash expense)/interest expense.

How can coverage ratios be interpreted?

These establish the capacity of a company to pay off its liabilities and obligations, such as debt, interest, cash requirements, etc. A higher ratio means the company earns a good portion of its revenue and can efficiently pay off its liabilities and obligations.

What is a good cash flow coverage ratio?

Most organizations should aim for a cash flow ratio of at least 1.5x. This means that for every $1 in interest payments, there must be at least $1.50 in operating cash flows.

Recommended Articles

This article has been a guide to what is Coverage Ratio. We explain the formula & calculation examples for its types, including interest, debt service, asset & cash. You can learn more about from the following articles –