What Is Contribution Margin?

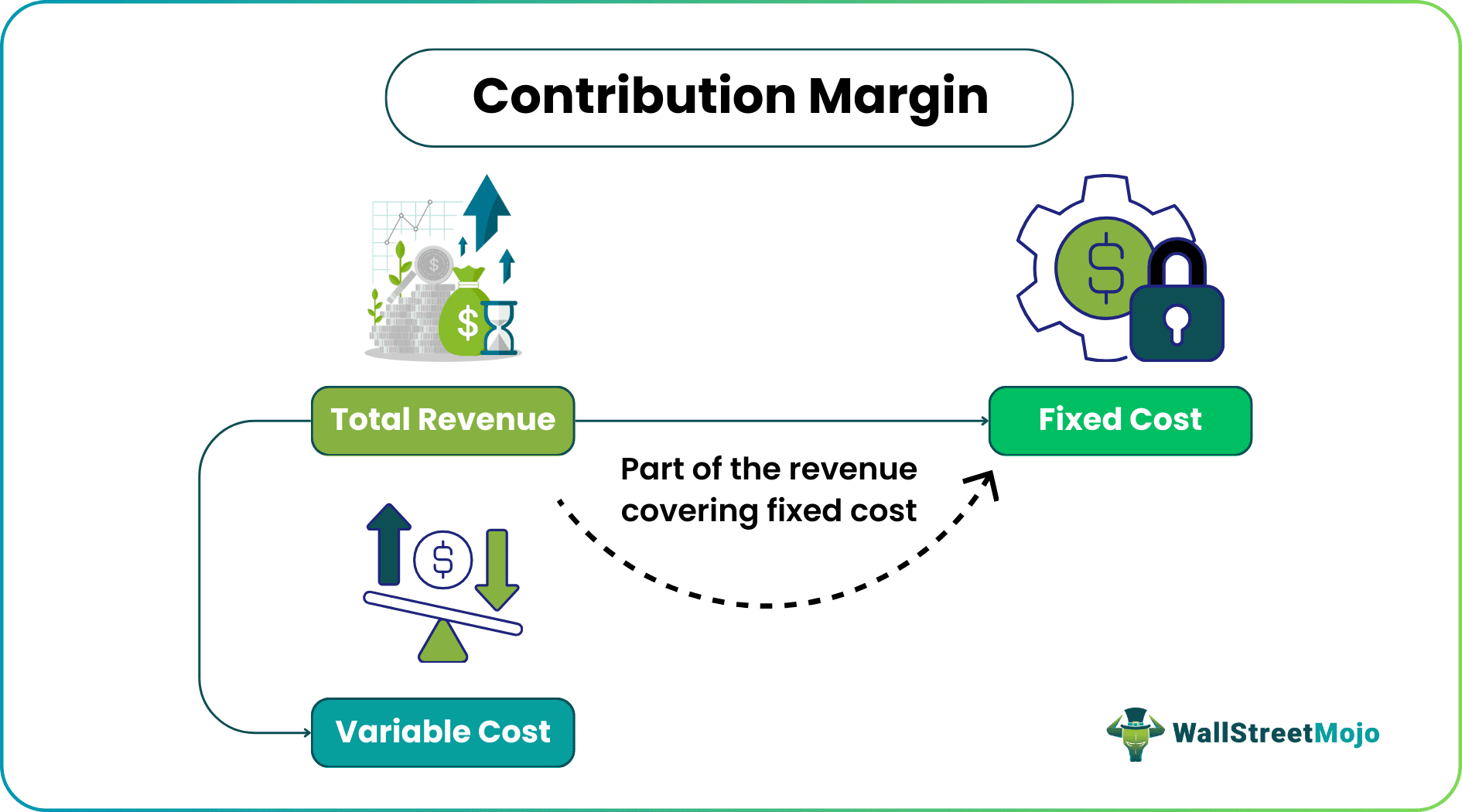

The contribution margin is a measurement through which we understand how much a company’s net sales will contribute to the fixed expenses and the net profit after covering the variable expenses. So, we deduct the total variable expenses from the net sales while calculating the contribution.

Contribution Margin Excel Template

Download Excel Template

It helps investors assess the potential of the company to earn profit and the part of the revenue earned that can help in covering the fixed cost of production. It contributes to the breakeven analysis calculation. The business can interpret how the sales figures are affecting the overall profits.

- The contribution margin is a tool to know how much a company’s net sales may contribute to the fixed expenses and the net profit after making up the variable expenses. Therefore, the total variable fees from the net sales are deducted while calculating the contribution.

- When there’s no way to know the net sales, one may use the formula to determine the contribution: Contribution Margin = Fixed Expenses – Net Income.

- The contribution margin ratio per unit formula is = Selling price per unit – Variable cost per unit.

Contribution Margin Explained

Contribution margin analysis is the gain or profit that the company generates from the sale of one unit of goods or services after deducting the variable cost of production from it. The calculation assesses how the growth in sales and profits are linked to each other in a business.

Using this metric, the company can interpret how one specific product or service affects the profit margin. Thus, it shows the sales amount after offsetting the fixed cost. The fixed cost like rent of the premises, salary, wages of laborers, etc will remain the same irrespective of changes in production. But variable costs change with change in production units. So it is necessary to understand the breakup of fixed and variable cost of any production process.

Explanation of Contribution Margin in Video

Formula

Let us check in detail how to calculate contribution margin. To calculate this ratio, we need to look at the net sales and the total variable expenses. Here’s the formula –

Contribution Margin = Net Sales – Total Variable Expenses

It can be expressed in another way as well.

Contribution Margin = Fixed Expenses – Net Income

When there’s no way we can know the net sales, we can use the above formula to determine how to calculate the contribution margin.

Example

Let us try to understand the concept with a contribution margin example.

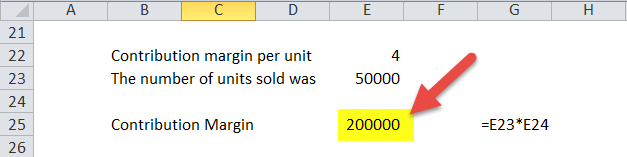

Good Company has net sales of $300,000. It has sold 50,000 units of its products. The variable cost of each unit is $2 per unit. Is it possible to find out the contribution, contribution margin per unit, and contribution ratio?

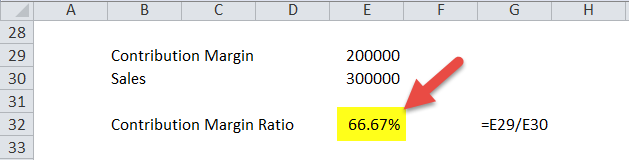

- The company has net sales of $300,000.

- The number of units sold was 50,000 units.

- Selling price per unit would be = ($300,000 / 50,000) = $6 per unit.

- The variable cost per unit is $2 per unit.

- Contribution margin per unit formula would be = (Selling price per unit – Variable cost per unit) = ($6 – $2) = $4 per unit.

- Contribution would be = ($4 * 50,000) = $200,000.

- Contribution ratio would be = Contribution / Sales = $200,000 / $300,000 = 2/3 = 66.67%.

In this example, if we had been given the fixed expenses, we could also find out the firm’s net profit. Thus, here we use the contribution margin equation to find the value.

Uses

We may ask why we need contributions. We need a contribution to find out the break-even point.

We will look at how contribution margin equation becomes useful in finding the break-even point.

Let’s take another contribution margin example and say that a firm’s fixed expenses are $100,000. The variable cost of the firm is $30,000. We need to find out the break-even point.

We will find out the break-even point by using the concept of contribution.

Contribution Margin = Net Sales – Variable Cost = Fixed Cost + Net Profit

Here, we can write –

Net Sales – Variable Cost = Fixed Cost + Net Profit

At the break-even point, the key assumption is that there will be no profit or no loss.

Then,

- Net Sales – Variable Cost = Fixed Cost + 0

- Or. Net Sales – $30,000 = $100,000

- Or, Net Sales = $100,000 + $30,000 = $130,000.

That means $130,000 of net sales, and the firm would be able to reach the break-even point.

Calculator

We can use the following Calculator

Calculate Contribution Margin in Excel (with excel template)

We can easily calculate the ratio in the template provided.

The contribution margin ratio per unit formula would be = (Selling price per unit – Variable cost per unit)

The contribution would be = (Margin per Unit * Number of Units Sold)

The contribution ratio would be = margin / Sales

We can download this template here – Contribution Margin Ratio Excel Template

Analysis

This metric is used by analysts in the financial field to understand how profitable the sale of a particular product or service is or how much should the selling price of the product be so that the company can earn the maximum profit out of it. Decisions can be taken regarding new product launch or to discontinue the production and sale of goods that are no longer profitable or has lost its importance in the market.

However, an ideal contribution margin analysis will cover both fixed and variable cost and help the business calculate the breakeven. A high margin means the profit portion remaining in the business is more. It may turn out to be negative if the variable cost is more that the revenue can cover.

Contribution Margin Vs Gross Margin

Let us look at the differences between the two topics given above.

- The former calculates the revenue remaining after deducting the fixed cost whereas the latter calculates the revenue after deducting the cost of goods sold.

- Gross margin is shown in income statement whereas the contribution margin is not done so.

- The former is helps in calculating the breakeven point and the latter calculates the gross profit of the business.

Contribution Margin Video

Frequently Asked Questions (FAQs)

Why is contribution margin necessary?

A company’s contribution margin is significant because it displays the availability of the revenue after deducting variable costs such as raw materials and transportation expenses. To make a product profitable, the remaining income after variable costs must be more than the company’s fixed costs, such as insurance and salaries.

Are contribution margin and gross margin the same?

No, contribution margin and gross margin are not the same. Gross margin is the difference between revenue and the cost of goods sold (COGS). On the other hand, contribution margin refers to the difference between revenue and variable costs. At the same time, both measures help analyze a company’s financial performance.

What causes a low contribution margin?

Several factors, including high variable costs, low selling prices, and inefficient operations, can cause a low contribution margin, overhead costs, and low sales volume.

Recommended Articles

This has been a guide to what is Contribution Margin. We explain its formula, differences with gross margin, calculator, along with example and analysis. You may also look at the following articles to enhance your financial skills.